The lending business is highly cyclical due to its sensitivity to interest rates, economic cycles, and capital availability to fund loans. According to the Mortgage Bankers Association, these factors are currently driving down mortgage originations, which have fallen 60% y/y in the U.S. in Q4 2022.

The decline in originations pressuring the margins of this high-cost activity is the leading change in the industry. Delinquencies, while currently low, are expected to grow rapidly over the next year as the economy slides into an anticipated recession. Banks need to increase their agility to deal with these volume shifts cost-effectively. There are two key levers to address the shift in processing volumes:

- Automation, which enables an absolute reduction in OPEX based on upfront investment

- Outsourcing, with committed volume flexibility, enables the matching of revenues and costs.

Of the two, the more compelling savings can be made from automation, as long as transaction volumes across the entire business cycle can justify the initial investment. Mortgage origination is a clear first choice for automation because:

- The cost of mortgage origination in the U.S. is typically 10x the cost of servicing ($5k to $10k per loan in the U.S. depending on product complexity and lender platform maturity)

- Origination remains mostly a manual process. Most Loan Origination Solution (LOS) platforms in the market are providing only partial STP processing, relying mostly on manual sub-processes

- Originations are highly cyclical.

Lenders and services vendors are trying to address the mortgage origination challenge, and while no single model has won the market, the as-a-service model looks most promising.

WNS has developed a mortgage-as-a-service (MaaS) offering, working with mortgage lenders for years, and has identified many typical breaks in legacy processes where processing is manually delivered. Critical to the success of a MaaS offering is bringing the most effective resources to bear at each step of the process. The choices include:

- Intelligent Automation of manual processes, where possible

- Optimal shoring of processes, where manual processing remains necessary

- Flexibility for clients to opt for unit-based pricing model

The key steps in the origination process where MaaS transforms processing are:

- Pre-processing and sending initial loan estimate: after receiving the application, the MaaS delivers an initial loan estimate within three days. All offshore delivery

- Third-party orders: auto-triggered order checks including flood, credit, verification of employment, verification of deposit, title, mortgage insurance, appraisal, fraud, etc. All offshore delivery

- Document validation: documents have data extracted and are converted to a digital loan file. Exceptions are handled manually. All offshore delivery

- Conditions management: decision engine and underwriting, automatically raising conditions for consideration by loan officers. Combined onshore/offshore delivery

- Document reviews: review and analysis of income, collateral, asset, title, Agreement of Sale, and fraud. Combined onshore/offshore delivery

- Approval: onshore lender works with the offshore team to approve the loan package. Combined onshore/offshore delivery

- Loan closing: LE and CD prep of documents; schedule closing with the title company. Combined onshore/offshore delivery

- Transfer to servicing: digital loan file transfer to servicing platform. All offshore delivery.

The backbone of the MaaS offering is a combination of

- Smart Workflow platform with integrated APIs to collect third-party information along with inbuilt models for underwriting

- Intelligent automation powered by RPA and Artificial Intelligence.

The MaaS service integrates with the client LOS platform and digital front end to deliver services to bank customers. Because the offering is modular, clients can buy point solutions to automate individual components of the origination process.

Technology is necessary, but not sufficient for successful transformation of the loan operations process. The human element is a critical component of the success of the MaaS offering. The MaaS offering incorporates the development and utilization of talent with a comprehensive understanding of the mortgage process, associated challenges, and parameters of compliance and non-compliance. Initial and ongoing training and examinations in end-to-end loan review including compliance measures are required to continually improve the quality of performance and service levels that complement the areas of automation.

WNS’ MaaS offering has been delivering lenders benefits including:

- Productivity gains of 3x from automation and global delivery

- Customer inquiries and complaints: 50% reduction

- Reduction in loan origination costs: 40%

- QA/QC processes eligible for automation: 70%

- Loan final closure in 15 to 20 days.

These benefits are especially compelling as origination volumes decline and a MaaS service connects costs to revenues, allowing for costs to decline as volumes plummet. We expect to see the industry produce more MaaS offerings as the economy continues to shift. Early vendors, such as WNS, will have more mature offerings as lenders shift to outsourced as-a-service operations models.

]]>

In NelsonHall’s recently published market assessment, Transforming Mortgage and Loan Services, we found that lenders are changing their approach to mortgage and loan operations from a focus on BPS and integration services to a focus on cloud migration and data management services.

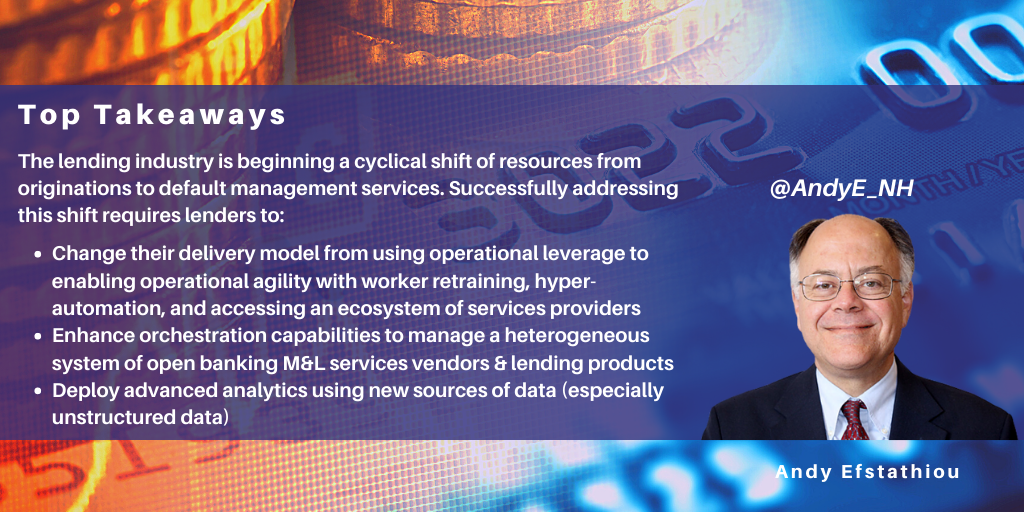

The goal for lending institutions today is to be able to support open ecosystem models, new product introductions, and process automation delivered for a wider range of lender types based on cloud-delivered operations. The pace of industry change is increasing, while the industry begins its cyclical shift from a focus on originations to default management services. The shift to cloud and digital-first delivery has expanded the scope of transformation projects as more processes are opened to third-party partners.

The state of digital operations in the lending industry

For the past year, lending institutions have been:

- Implementing intelligent automation to reduce manual processing and increase accuracy

- Migrating to a hybrid cloud to increase flexibility for new functionality and product time to market

- Building data lakes to coordinate data across silos without replacing their entire data structure

- Providing customers with self-service tools to reduce the cost of delivery and increase CSAT with faster resolutions.

Today, financial institutions anticipate an aggressive decline in originations and increase in lender defaults. This will necessitate downsizing originations and growing default management capabilities. To meet this market shift, over the next year, financial institutions will focus on:

- Increased use of consulting and combined ITS/BPS to identify a road map and convert CAPEX to OPEX

- Reskilling of origination workers to default processes to scale up default work

- Rearchitecting the lending platform to a microservices-based cloud-native application with an architecture that could integrate into their other platforms

- Testing and running open banking environments to start building an ecosystem of participants and a library of business models.

However, the external environment has put up barriers to transformation. The key barriers impeding the efforts of financial institutions include:

- Useful adoption of analytics: new sources of data (especially unstructured data) provide greater opportunities for the use of AI. However, only tier one lenders have access to large internal data pools. Smaller lenders must draw from industry-wide data pools. Smaller markets and product runs present similar issues: developing quality data for analysis remains difficult

- Access to emerging technology: all service vendors are building ecosystems for emerging technologies and acquiring staff skilled in relevant technologies. Finding the best new technologies and embedding them in effective platforms remains difficult

- New products and markets: lenders are rolling out new loan products rapidly, requiring a response from other lenders in order to remain relevant. The new products require high automation, omnichannel access, and high compliance capabilities

- Access to qualified staff: changing technologies change the required mix of staff skills, and distributed work environments (primarily WFH) limits knowledge transfer. Currently, cloud migration, AI, and default management skills are the least available capabilities.

Rising to the challenge

To address these challenges successfully, lending institutions need to focus on two activities: strategy and process execution.

Key factors in strategy include:

- Creating a roadmap to move operations to the cloud and match costs to revenues, as origination volumes decline and collections volumes grow

- Changing the operational model: M&L managers need to shift from operational leverage to leveraging agility (the ability to cost-effectively switch out workloads). This requires increased process discovery to identify processes for automation. The business model needs to support an open banking environment

- Building an ecosystem of operations vendors with domain knowledge and experience with clients’ operations environments, vendors with complementary digital skills to deliver services, and the ability to work within client operational practices and transfer knowledge.

Key factors in process execution include:

- In the short term, staff training to renovate skills for cyclical issues (i.e., default management) and technology (FinTech, cloud, and IA)

- Preferred services vendors should have the widest pool of Fintech solution providers supporting them

- Data management and orchestration drive accuracy, efficiency, and compliance. Lenders need to build COEs and libraries of successful RPA and data management use cases

- Transforming application development to a DevOps and low/no code model to speed the innovation cycle and migrate to cloud delivery

- Orchestration: selection and implementation of orchestration tools to manage a heterogeneous system of (open banking) M&L services vendors and lending products.

In summary, lending institutions are changing their goals from improving process efficiency for originations to increasing operational agility across sub-processes and ramping up collections capabilities. Margin pressure is too strong for lenders to achieve their business goals with just operational efficiency enhancements. Lenders need to change their business models (from closed platform/static product offerings to open platform/evolving product lines) to enable them to access best practice, best-cost services on-demand, to drive their operational performance.

]]>

NelsonHall recently completed a market assessment and forecast report on Transforming Mortgage and Loan Services. We found that the lending industry is undergoing profound operational change as it adapts to slowing loan growth and emerging customer populations that are younger and more technology savvy. For the past two years, lenders have been:

- Variablizing and reducing the cost of operational delivery using automation, AI, and third-party operations delivery

- Moving to hybrid cloud delivery. This trend is still in the early stages and has been accelerating with the advent of the COVID-19 pandemic

- Standardizing, consolidating, and automating operations across multiple products and markets. Most lenders have been built via M&A and they have tried to differentiate themselves with new loan product features. Standardizing their heterogeneous platforms to reduce cost of delivery and unify customer experience is a high priority

- Focusing on cost reduction for high-cost processes. Origination, due to its high cost ($3k to $7k per closed retail mortgage in the U.S.) has been the highest priority target for cost reduction.

COVID-19 & other challenges

The COVID-19 pandemic has accelerated these trends and initiated an aggressive move to remote work. Remote work has increased the need for strong cybersecurity and for robust national infrastructure in some emerging markets to support remote delivery.

The external environment has put up barriers to transformation. The key barriers impeding their efforts include:

- COVID-19: lenders have been focusing on maintaining operations, while shifting to a work-from-home (WFH) environment. The impact has been to put transformational projects on hold for the short term

- Competitive landscape: the introduction of all-digital lenders, with unproven business models, has led many incumbent lenders to take a wait-and-see approach to business model change

- Changing technologies making long-term investments risky.

For lenders operating in multiple markets, local requirements make transformation difficult. Market-specific requirements that make a standard global delivery methodology impossible to achieve are:

- Local markets require different licenses and procedures, and feature different customer expectations and competitive landscapes

- Evolving loan product types are based on new data fields and product attributes, making existing taxonomies obsolete.

Lenders adapt transformation strategies

Transformation strategies have had to take these barriers into account. While they have postponed many initiatives, lenders have not abandoned those projects. Currently, lenders intend to restart projects when the impact of the pandemic is clearer, and prior to full resolution of the pandemic. At this point, it looks like these projects will restart by late 2020.

Digital transformation goals for lenders are changing from cost-focused to agility-focused goals. Key changes in goals for transformation projects include:

- Strategic goals are moving from reducing costs to changing business models:

- Moving from enable remote customers to enable remote employees (due to COVID-19)

- Transforming to an open banking environment with large ecosystems of partners

- Financial goals are moving from optimizing at fixed volumes to optimizing at constantly changing volumes:

- Increasing flexibility by reducing breakeven volumes and ability to react to change

- Improving STP by tying front-end to back-end for faster TAT

- Increasing sales by taking on new customer types facilitated by better analytics

- Engagement goals are moving from “same mess for less” to “transform”:

- Standardizing and consolidating platforms and methods across silos

- Automating to reduce the labor component and manual errors

- Changing DevOps to facilitate faster, modularized platform renewal

Summary

In summary, vendors are changing their goals from cost efficiency for fundamentally static businesses to agility for continuously changing businesses. The operational changes being made will enable and drive further change in the business. These operational changes will drive accelerating change in lenders’ product offerings, customer base, and market presence. The mortgage industry is at the start of a decade-long transformation of its business model.

Find out more about NelsonHall’s Transforming Mortgage and Loan Services market assessment and forecast report here.

]]>

NelsonHall recently hosted a webinar in which U.K.’s National Savings and Investments (NS&I) discussed how it has transformed its customer experience and operations delivery, and in so doing increased the value of assets managed by 245% and annual contact volumes by 660% while reducing delivery staff by 76% and cost of operations, calculated on a per assets under management basis, by 24 bps.

NS&I’s Mark Keene, who manages the operation’s outsourcing relationship with Atos, described four key initiatives which have enabled it to transform its delivery into a very low-cost digital business with rapidly growing revenues.

NS&I’s business model is a self-funding process of reinvention where operational savings generated from digitizing its operations allows NS&I to generate additional revenue streams from new channels, offerings, or customer demographics. The strategy was implemented using four key initiatives:

- Business reinvention: modernize the platform and business model to shift distribution to digital channels

- Customer experience: improve CX by implementing channel interfaces, which were created using design thinking to improve delivery of CRM services

- Operational Excellence: change supporting operations infrastructure from physical to digital to takeout ~70% of delivery costs

- Trust and compliance: mitigate cybercrime and data loss risks inherent in the new digital infrastructure.

Each of these initiatives required close coordination with Atos. Key components of each initiative are covered below.

Business reinvention

Business reinvention consisted of two components:

- Platform modernization

- Ability to pursue B2B business with other government agencies.

Platform modernization delivered functionality including:

- Transfer to a new operating platform of ~1Bn Premium Bond records

- Consolidation and virtualization of the IT infrastructure

- Retiring of legacy infrastructure and applications

- Implementation of a training and competence framework

- Implementation of a new evaluation tool to drive improved call center operator performance and gather real time feedback from NS&I customers

- Automation of ‘Evidence of Identity’ checking regime for initial sales

- Technology to support the shift to online and telephone channels for customers to manage their NS&I products.

The new banking platform made it faster to develop and bring new offerings to market, and remove offerings when sales targets are reached.

B2B business with other government agencies has been pursued with three agencies delivering payments services. In 2014, NS&I and Atos created NS&I GPS (Government Payment Services) to deliver payment services. The offering reduces NS&I’s overhead costs, and at the same time it reduces the cost of payments for the other agencies. Currently there are contracts with the Ministry of Justice, the Home Office, HMRC, and the Department for Education.

Customer experience

Prior to the customer experience initiative, NS&I was a paper-based institution. NS&I increased channel access and captured CX to improve overall customer satisfaction. To implement these changes, NS&I set up a CX directorate, which coordinates teams including:

- Customer Insight Team: to generate an understanding of customer requirements and current performance, and move from a product-centric view to a customer-centric view

- Digital Engagement Team: to build a CX lab based in Glasgow for clients and NS&I to shape, prototype and test business concepts

- Customer Communications Team: to change contact management culture at NS&I to improve CX and ensure deployment of a mobile optimized website and apps, web chat and co-browsing that will support customers.

NS&I now sells 100% of its offerings direct to customer via digital channels. It offers customers an online experience that has been designed and tested with its customer base, with 3.7m customers registered to use online services.

Operational Excellence

Operational excellence consists of two components:

- Workforce management: reduction of operational headcount from 4.2k to 1.2k in a heavily unionized environment, without the need for any compulsory redundancies

- Real estate consolidation: replaced the entire operational estate portfolio with economically modern real estate, including highly efficient buildings with low carbon footprint and inbuilt sustainability. Reduced the legacy footprint of 1.2m sq. ft. by ~85%. Released £13m of real estate capital receipts. Reduced real estate running costs by 50%.

Funds released have been reinvested into the three other NS&I initiatives discussed here.

Trust and compliance

The move to virtual operations delivery and digital channel sales only means that NS&I is more vulnerable to cyberattack. Atos upgraded the core banking platform to mitigate existing and emerging vulnerabilities as security threats become more sophisticated. To align incentives between vendor and client, NS&I contracted with Atos for them to ensure compliance with all current and future FCA regulations. Atos carries the risk for all losses associated with fraud, error or data loss.

Conclusions

Growing a business is tough. Growing a business while reducing costs and increasing profits is even tougher. NS&I has succeeded in accomplishing this goal by realistically assessing its capabilities and strengths, then partnering to access capabilities and disciplines which it did not have internally. Disciplined partnering has led to a long-term journey which has built strong competitive differentiation of offerings, customer experience, and cost structure.

The build-up of differentiated capabilities and brand promise over a long period of time creates proprietary IP and customer goodwill which is very hard for a competitor to challenge over the long term and impossible to challenge in the short run. To date, NS&I has relied on government sponsored investment products to create its own differentiation. By changing its delivery to reduce cost and increase channel offerings, NS&I is creating a new set of differentiators. Established competitors will find it difficult to challenge the new cost structure, and Fintech start-ups will find it difficult to challenge the brand promise in any reasonable timeframe. While any such competitor tries to make such a challenge, NS&I will continue work on its operations roadmap development with Atos to build additional capabilities. Over the next three years, NS&I will be creating:

- Offerings for mass market customers, which require even lower cost operational delivery

- B2B digital engagement offerings for its government clients, which can eventually be productized for sale to private sector B2B clients.

Critical to NS&I’s ability to adapt to the changing marketplace is the ability to consider and experiment with new technologies. NS&I and Atos are currently exploring the possibilities of blockchain and encryption technologies, artificial intelligence, platforms, prescriptive analytics, and accessing wider innovation through open API connectivity. We will update you on the results of these initiatives as they are known.

NelsonHall runs regular webinars for buy-side sourcing practitioners. To find out more, contact Vicki Jenkins.

]]>

As discussed in my blog of April 12, 2017, the mortgage processing industry in the U.S. is challenged to remain profitable because, from 2012 to 2016, loans outstanding grew 1.8% per year, while processing costs grew at 7.3% per year. This is leading to industry consolidation and operational restructuring. A recent example of a BPS vendor consolidating in order to drive greater efficiency into operational delivery is HCL Technologies with its acquisition of Urban Fulfillment Services Llc. (UFS).

Analyzing the transaction

HCL has agreed to acquire UFS for $30m, to be paid in tranches as certain goals are met. The transaction is expected to be completed by June 2017 subject to transfer of licenses (in 48 states) and regulatory approval. Founded in 2002, UFS has:

- ~350 employees

- 3 delivery centers:

- Troy, MI

- Denver, CO

- West Lake, CA (Los Angeles)

- 4 clients across 3 key demographics:

- 1 tier one bank

- 2 credit unions, of which one is the 3rd largest federal credit union

- 1 non-bank lender

- Services that are predominantly origination portfolio purchases, and fulfillment. HCL did not purchase the appraisals, evaluations, mailroom, or print services

- Bank products supported for conforming mortgages, non-conforming mortgages, HELOCs, and refinances

- ~200 mortgages processed per day on average.

UFS provides a client base that overlaps with HCL’s clients, but from the capital markets side. HCL has a capital markets client base that is increasingly looking to buy loan portfolios, allowing HCL to upsell UFS services to them. Indeed, the price paid is reasonable to gain access to a substantial U.S.-based M&L BPS business.

UFS brings onshore delivery capabilities, with capacity for internal growth. Its staff have on average 10 years of M&L BPS experience.

The acquisition allows HCL to grow strategic parts of its business:

- SaaS cloud delivery: HCL will enable As-A-Service delivery of software and BPS. This will reduce cost of delivery for clients, which is important in the current cost pressure environment. HCL will use FinTech enablement to deliver much of the efficiency improvement in operations, and intends to build a loan origination solution delivered from the cloud as a new offering for clients

- Retail banking (not just capital markets): HCL wants to pursue consumer loan BPS across all its processes.

HCL is also looking to make additional acquisitions over the next year to gain specialized loan expertise such as auto or student loans.

Conclusions

HCL is a vendor with strong technology services capabilities, which will be needed for adapting the strong loan BPS assets acquired in this transaction. HCL will be challenged to integrate UFS (which sells BPS services to consumer lenders) into its capital markets and ITS portfolio of offerings. Maintaining cultural independence and cross-cultural coordination within the resultant organization will require clear role-based definition and execution. HCL has been a successful serial acquirer of businesses, which indicates it should be able to successfully integrate these two firms.

Profitability will be dependent on increasing the level of automation. While UFS is currently profitable, the market is experiencing a large cost squeeze, driven in part by compliance costs, but also by stagnating volumes. When the origination market makes a cyclical downturn, volumes will fall aggressively. HCL will need to have implemented its FinTech enhancements to drive down break-even capacity utilization ratios, to be a winner in that environment. HCL is on the right path to succeed, but speed to digital enablement will determine if it can execute successfully.

NelsonHall will publish a major market analysis report and NEAT vendor evaluation for next generation mortgage and loan BPS services in late Q2 2017, addressing M&L BPS market issues in greater detail.

]]>

NelsonHall attended the WNS analyst conference in New York last week for a business update and to hear about their current initiatives. Here I take a quick look at WNS’ banking industry business specifically, and at how it is focused on applying FinTech to BPS delivery to support large productivity gains for its U.S. regional banking clients.

Market conditions are driving clients, especially in banking, to rethink their business models, operations, and partnerships, and WNS believes it will need to cannibalize existing business to migrate its clients to more efficient digital operations. The willingness to cannibalize revenues has shown itself recently, with double-digit banking revenue losses by quarter Y/Y for the nine months ending December 31, 2016. However, banking processing volumes have increased in North America (primarily the U.S.) and U.K., while decreasing in its RoW markets (which represent half of banking revenues). The North American market is WNS’ primary target market for banking BPS, and increasing volumes in the region indicate that a strategy requiring legacy BPS delivery to be cannibalized by digital-enabled BPS is on track.

WNS’ strategy for the banking BPS market is to focus on regional banks in the U.S. market, primarily banks with $20 Bn to $150 Bn in assets. It has developed a set of tools (TRAC) which sit on top of legacy systems, draw data from silos, and deliver FinTech functionality to relevant processes and channels. WNS has decided to focus on its existing client base to deliver FinTech BPS across a much larger footprint within the client. This has resulted in an elongated sales cycle, which has also depressed short-term growth.

The strategy has begun to pay off, as demonstrated by a contract with a long-term banking client who for many years purchased only one process, credit spreading. This client has acquired 5+ banks in the past two years and has realized it needs to consolidate operations and aggressively improve operational delivery. WNS won the client’s BPS business (another vendor has the ITS remit) and WNS will now expand its operational footprint to cover deposit operations, mortgage originations, and retain credit spreading. Further expansion of the contract is expected.

Part of WNS’ commitment to cost reduction is underpinned by a pricing model, Total Relationship Discount Model, which guarantees cost savings under a non-FTE based business model. Under this pricing model, WNS commits to a set level of cost saving (e.g. 10%). WNS can decide where it will find the savings to optimize its processing, or the client/vendor can select additional areas to pursue wider dollar savings on additional processes. If WNS does not deliver the guaranteed level of savings, it will remit the difference to the client.

In summary, WNS is pursuing the right approach in targeting a very narrow segment of the banking market to pursue FinTech-enabled BPS. This will cannibalize revenues and slow the pipeline in the short run, as WNS and other vendors such as IBM have demonstrated in the past few years. However, in the long run, successful execution of this strategy will produce rapidly growing revenues as clients consolidate vendors to ones with domain expertise in emerging technologies and its application to sub-industry specific challenges. The alternative will be long-term business decline, as the current decline in legacy BPS accelerates.

]]>

The mortgage and loan servicing industry is beginning a period of rapid change in the way business process services are delivered. Over the past few years, mortgage portfolios have not grown rapidly. For example, in the U.S., the largest residential mortgage market in the world, loans have grown only 7.3% from year-end 2012 to year-end 2016, a CAAGR of 1.8%. Some lines of loans have grown quickly, such as auto and education loans in the U.S. However, those loan pools are smaller than the mortgage pools and loan servicing requirements are less complex, both of which drive much lower revenues for processing services.

During the same time, regulations governing loan servicing have increased the cost of servicing by 14% CAAGR, according to the Mortgage Bankers Association. The increasing compliance costs of processing loans has led to banks and servicers exiting the business, notably CitiMortgage’s sale of 780k mortgages to New Residential Investment, due to close in Q2 2017. A separate contract with Cenlar to process the remaining Citibank mortgage portfolios will result in Citibank processing all its mortgages with third party vendors by 2018. In fact, according to the U.S. Government Accounting Office, from 2012 to 2015 non-bank mortgage servicers increased their market share from 6.8% to 24.2% of the market. The gains in market share by non-banks is attributed to the lower level of supervision of non-banks by regulators. Despite this, the economics of servicing are so bad that, in a review of the three largest non-bank mortgage servicers in the U.S., Moody’s found that only one of the three were profitable.

The bottom line is that the economics of this business are terrible, and eventually either lending will shrink or servicing operations must become much more efficient. We are seeing signs of vendors moving towards much more efficient methods of business process delivery for loans. These methods can deliver 40% cost reductions from the current standard of practice. The methods employed to deliver efficiency gains rely on the use of FinTech solutions, but include a broad range of techniques, including:

- Greater focus on employee training, which enables greater effectiveness in process execution, particularly when using digital tools to support external stakeholders (primarily customers, but including regulators, service providers, and management). Increased training increases the employment value of a worker and serves to enhance efforts in recruiting, retaining, and adapting the workforce over time

- Increased investment in proprietary IP, including templates, frameworks, APIs, and methodologies. These serve to facilitate process reengineering and change management when business conditions change and the lender changes its portfolio of offerings

- FinTech solutions which increase the level of automation and STP to reduce the overall cost of delivery. The key to modern digital solutions is the adaptability of solutions across environments. In the past, scripts were applicable to one task. Modern digital solutions can deliver automated execution across hardware, software, databases, and processes. Reuse of a single license across tasks reduces cost of ownership and increases flexibility of operations.

Banks have been focused on compliance challenges and sales efforts for the last five years. In the past year, banks have been turning to BPS vendors to deliver improved process efficiency for them. Delivering increased efficiency requires a deep dive into industry sub-processes, with an equivalent level of domain knowledge around technology, and yet finding individuals skilled in both areas is difficult. BPS vendors committed to process transformation as part of their services delivery are working to attract and develop those rare employees with dual skill sets. The result can be cost savings over 40%, versus traditional outsourcing cost savings of ~20%.

NelsonHall will publish a major market analysis report and NEAT vendor evaluation for next generation mortgage and loan BPS services in late Q2 2017 to address these issues in greater detail.

]]>

Based on NelsonHall research conducted during late 2016, I have identified three key predictions for business process services (BPS) and IT services (ITS) in the Banking sector in 2017.

1. Compliance initiatives move from industry headwind to tailwind

The first prediction is that compliance operations change initiatives will decline, and the resources released from this change will fund new revenue generation activities.

Changing bank operations procedures and execution has been the primary driver of operations projects (and the major expense) for the past three years. In 2017, this trend will reverse. With implementation of existing compliance requirements largely in place, spend in this segment would most likely have reduced in 2017 anyway, but the U.S. election has further signaled a respite for banks from new regulations.

Existing initiatives are now set to pay off for the banks. Banks have undertaken:

- Automation initiatives: primarily robotic and analytics initiatives focused on KYC, AML, and FATCA. Complete digitization of these processes now means any future changes will require AMD services, not operations services

- Third party delivery of compliance: Compliance-as-a-service shares implementation overhead and increases industry standard adoption of regulations. Third party delivery has eliminated compliance as a competitive differentiator. Future change adoption is now in third party hands

- Global standardization: Banks have shifted compliance delivery from unique systems for each market to global systems with a standard taxonomy, but configurable for each market’s unique regulatory requirements. This makes new market entry and compliance changes a matter of changing configuration, not developing a new system.

Compliance to date has been a cost sink, which has delivered no differentiation or revenue. However, because most compliance initiatives have focused on customer acquisition requirements, banks are now able to turn those compliance capabilities into customer acquisition drivers. With reference to the three areas above, customer acquisition can now be driven with:

- Automation, used to drive down TAT and enhance customer experience

- Third party delivery, used to segment clients and markets, where high priority clients/markets are delivered by retained organizations and lower scale/priority ones delivered by third party vendors

- Global standardization, increasing brand integrity for existing customers and providing the same experience for new customers.

In essence, banks will be able to create a ‘one brand’ experience for a much larger audience.

2. Revenue generation becomes the top industry priority

The second prediction is that banking BPS vendors will develop multi-service capabilities to support clients in new revenue generation.

Banks can only reduce costs so much on a shrinking base of revenues. In 2016, banks have started to focus their attention on increasing revenues, while reducing marginal variable cost per unit of marginal variable revenue. The great game of 2017 is shaping up to be one of how to find opportunities for good marginal cost/revenue gains, and then execute against those opportunities. Key initiatives that BPS vendors are working on include:

- Automation and FinTech initiatives: Due to the low cost enabled by increased automation and enablement of much lower cost delivery methods (i.e. digital channels versus brick & mortar channels), banks are able to address previously uneconomic market segments, including lower revenue customers (e.g. mass affluent customers in private banking) and lower revenue markets (e.g. small country entry and/or lower potential revenue product offerings). The remaining challenge, now that banks can technically address these opportunities, will be for banks and vendors to understand the peculiarities and demands of these new customer, market, and product segments

- Improved customer experience: Lowering the cost of customer acquisition and delivery reduces the barriers to entry for competitors to lure customers away. Rebuilding barriers to entry requires delivery of a unique and agreeable customer experience. This has changed the way banks and vendors address the set-up of customer experiences. The focus has been to build customer interaction operations with a ‘design thinking’ approach, which utilizes a human psychology approach to building delivery to satisfy human expectations and needs. Much has been written about this, and while it’s all the rage in the industry at the moment, it is only likely to yield results if based on quality market research and platform build.

These initiatives provide a good base for banks to build out their revenue generation capabilities in 2017, after years of languishing revenues. Banks have reduced their stable of third party vendors to reduce cost and regulatory certification of vendors. Successful vendors, therefore, will be the ones who can deliver a broad footprint of services across technologies, geographies, and customer segments.

Understanding the buying requirements of previously unbanked customers and markets is not going to be easy to do well. Most vendors will need to expand their market research capabilities to develop the insights necessary to support effective execution of this strategy. And to do that, vendors will have to pursue M&A activities.

3. M&A initiatives will accelerate to enable the shift to a pervasive FinTech structure

The third prediction is that significant mergers, acquisitions, and partnerships will emerge as the Tier 1 service providers continue to develop their digital delivery infrastructure.

To be successful in 2017, vendors will need to build out their offerings to support an emerging environment where new technologies, FinTech, are being adopted to deliver new functionality; technology which is directly related to human senses, emotions, and experience. Building such technologies sequentially would require very long lead times. The answer to that challenge is to build these technologies in parallel. Since no one organization can design, build, and run such a large infrastructure development program, many technology firms will have to focus and specialize on discrete project areas. Then, the successful ones will either merge into larger organizations or acquire other organizations. In the short run, the next two years, vendors will need to partner or acquire capabilities.

Over the next two years, M&A will focus on technologies mature enough to deliver operationally tested functionality where banks are ready to undertake widespread adoption. These technologies include:

- Machine learning: these technologies have been deployed over the last three years, and users have identified high-value use cases (primarily in customer interactions)

- Cloud delivery: IT services vendors have trialed use cases (especially where security is less of a concern), cybersecurity solutions, and delivery (primarily partnering with large vendors such as Amazon Cloudfront)

- CRM for mobility: Scaling the mobile channel cannot be done with a labor-only solution. Automation of customer mobile support has been trialed, and effective first generation solutions have been developed which will now be rolled out and developed into second generation solutions.

The next twelve months will see deployment of these technologies across borders and products. To scale the delivery of these deployments, ITS vendors will need to add labor skilled in these technologies by acquiring small specialist consulting and ITS firms. They will also need to acquire IP to fill in the gaps in IT that ISVs are missing. Examples include:

- APIs connecting legacy platforms with new technologies

- ITS automation tools focused on these domains

- Solutions that can enhance functionality, such as CRM modules providing functionality not provided in existing mobile CRM tools.

Summary

In 2017, the banking BPS and ITS industry will consolidate many of the small-scale FinTech initiatives that have been developing over the past three years. FinTech solutions remain very small-scale to date, but have been very successful in identifying use cases and developing solutions that have been successfully deployed at small scale. Over the next year, the FinTech solutions and services industry is poised to deploy at scale and to develop initial capabilities into robust capabilities. This will require aggressive scaling of resources, staff and infrastructure, and will require deepening of IP to deliver much more robust functionality that can be successful in a broader range of operating environments than has been required of these technologies to date. It is shaping up to be a fun year!

]]>

At HCL’s recent adviser and analyst event, #HCLBigLeap, I spoke with their banking industry executives about HCL’s strategy and activities designed to drive application maintenance and modernization services, and specifically about the key ISV partnerships that are enabling this.

Background

HCL was founded in 1976, and had a strong focus on manufacturing during its first two decades. HCL Technologies was spun off as the enterprise’s software services and information technology company in 1991, and was listed in 1999. Application services, which includes AMD services, has been HCL’s largest service offering by revenues until Q2 FY 2017 (ended September 30, 2016). However, application services has faced slowing growth due to declining demand for ERP deployment. HCL is mitigating that revenue loss with expanded application modernization services, which is of particular interest in the financial services industry.

Key partnerships underpinning application modernization drive

HCL has pursued a strategy over the past 35 years of creating joint ventures and alliances with key partners such as Hewlett Packard, Cisco, Perot Systems, Deutsche Bank, and NEC Corporation, amongst others, to drive strategic growth.

Recently, HCL has set up JVs and partnerships with banking industry software vendors to drive application maintenance and modernization services targeting the widely adopted legacy platforms used by global financial institutions. By helping global banks modernize their legacy platforms, HCL hopes to expand its banking client base and develop domain expertise on the custom legacy platforms within these banks.

Current partnerships include CSC and Infor:

CSC

In July 2015, HCL and CSC formed a joint venture, CeleritiFinTech, in which HCL contributes engineering capabilities to provide modernization services for Hogan platform, CAMS II, PTS, and EarlyResolution. Specifically, HCL has developed source code documentation capabilities that can document complex COBOL mainframe source code. This documentation is useful for deconstructing the code so as to be able to isolate components relevant to a specific function, and thereafter apply incremental modernization techniques such as API, exposing business logic, data, etc. From this, it is possible to identify any customizations that have been made to the code, and identify how to change code or insert new modules and subroutines as banks modernize their applications. Alternatively, this capability can be used to diagnose bugs in new code. APIs so developed can be reused in deploying standard FinTech functionality.

As part of the JV, HCL has recently finished mapping the original source code, and in Q4 2016 will be rolling out app modernization services to the ~100 CSC banking clients using CSC banking solutions

Infor

In June 2015, Infor & HCL announced a strategic partnership. This collaboration will help to expand implementation, development and support resources for Infor customers across all geographies through HCL’s local operations in ~30 countries. As part of the alliance, HCL will build a practice specifically to support key Infor products, including Infor M3 and Infor Lawson Enterprise Financial Management, dedicating ~500 employees to work exclusively with the Infor ecosystem. The company’s resources and expertise combined with Infor’s applications will promote faster and more effective responses to market opportunities, which is expected to serve as a catalyst for growth for both organizations.

Summary

Banks are challenged to modernize legacy systems, primarily those based on the COBOL language, where source code documentation and skilled programmers are in limited supply. At the same time, banks are under pressure to modernize from:

- Regulators, who are demanding compliance for new regulatory frameworks

- Competitors, many startups, who are delivering digital banking services that did not exist in the past.

HCL’s ISV partnerships are enabling it to reduce time to market and cost to deploy new functionality or remedy existing software. These initiatives provide HCL with a large installed base of established banks with which they can pursue AMD services. This has required large investments (tens of millions of dollars in each case) to map the code, but it should pay commensurate dividends over the next ten years, as banks cannot re-platform in the current business environment, if ever. HCL intends to expand this initiative as opportunities present themselves.

]]>

NelsonHall attended the IBM Forum for Financial Services event in New York this past week, which focused on how bank customers are using IBM’s cognitive offerings. IBM has been investing heavily in services and technologies to enable deeper insight into financial institutions’ customers, starting 18 months ago with the development of Watson-based analytic assets.

IBM’s thesis is that it can segment financial services customers in a better fashion than traditional institutions have done in the past. Its approach is to segment customers by their individual preferences rather than by the institution’s preferences, i.e. asking the question ‘what does the person want or need?’ rather than ‘is this a high net worth customer or low net worth customer?’. To enable this, IBM is utilizing its repository of analytic learnings and clients’ customer databases, using its dynamic segmentation tools to identify changes in customer needs based on transaction history, which then enables banks to offer relevant products to meet emerging consumer needs.

In Generation 1.0 of IBM’s customer analytics for the financial services industry, it engaged clients in around 26 PoCs to establish new customer segmentation and improve both the customer experience and the clients’ sales. Of these POCs, around18 have moved to full production. The others are not funded at this time due to required capital commitment versus hurdle rates many of these on-hold projects will be revisited now that IBM has developed a cloud-based delivery system with a lower price point than an internally delivered project.

At the forum, IBM announced Customer Insight 2.0, part of its financial services customer analytics offerings. IBM’s new capabilities include:

- Prebuilt solutions based on experience to date

- Cloud-based delivery to lower adoption costs, including private cloud implementation to address client security issues

- APIs to integrate legacy systems into emerging technologies

- Customer prebuilt profiles (nine life event profiles based on research and PoCs to date).

A key question that the PoCs have been seeking to answer is what life events and personality traits are driving customer behavior and how can a bank support the customer in dealing with those issues. Clients buying these services from IBM have been focused on single bank product lines, but are looking to maximize overall customer retention and life cycle value. Ultimately, better cross-selling of existing customers can only succeed if those customers have a high satisfaction level. Thus, immediate sales performance is not as important as customer satisfaction.

IBM has developed a way of looking at customers that is less institution-centric and more consumer-centric. It uses its Watson capabilities and industry experience to enable better usage of a bank’s transaction data to understand its own customers. IBM uses its dynamic segmentation capabilities to identify changes in consumer needs, which can trigger changes in buying behavior that the bank can fulfill. IBM provides the infrastructure to deliver these now productized capabilities so that banks can use them to drive revenue and, more importantly, customer retention, at a lower price point than would otherwise be possible.

While further buildout of this offering will happen, banks using it are now can begin redefining their relationships with their customers for the digital age.

]]>

Here I take a look at how platform-based business process services (BPS) is yielding benefits for retail banks – specifically, delivering manual processes with greater efficiency, increasing automation, and delivering transaction products at scale.

Delivering manual processes with greater efficiency

Retail banking (RB) BPS is a large-scale, mature business with high adoption rates by global banks operating in their home (mature) markets. However, to date, RB BPS has had low adoption by mid/small tier banks and all sizes of banks within emerging markets. Global banks typically start with single tower BPS engagements and slowly expand to multi-geography and multi-product engagements.

Vendors are asked to deliver elemental processes focused on disputes, reconciliation, and data management, from offshore centers. These processes include manual review, remediation, and analysis of assets/liabilities/entities, data, and documents. Efficiency improvements have focused on process optimization, using techniques such as Six Sigma, to improve efficiency and accuracy, and meet deadlines.

Clients and vendors have been challenged to improve BPS efficiencies beyond labor arbitrage and process discipline, due to banks’ product-centric legacy systems (which make platform-based process improvements difficult). In addition, siloed legacy systems make data extraction for deriving analytical insights difficult. Continuing industry consolidation has made legacy systems a growing challenge.

Developing & delivering automated processes

Platform-based RB BPS delivery has been tried over the past five years with the aim of delivering lower cost and higher quality operations. However, previous attempts at platform-based delivery have failed due to the unwillingness of banks to replace legacy platforms en masse. This is now changing, with the RB BPS industry beginning to adopt platform-based BPS delivery to support a wide range of banks, including global banks (their emerging market operations), regional banks, local banks, and start-up banks. The platforms are not core banking platforms, but rather process platforms (e.g. reconciliation, customer management, settlement, etc.). These are not an integrated part of the bank’s core platform, but rather operate by pulling data or transactions from the bank’s core platform, often from multiple siloes.

The processes are mostly transaction-based. Typical processes include: data/transaction support, document management, compliance, omni-channel delivery, and support for entire operations for smaller/start-up banks. Delivery to date has been focused on single tenant environments. However, BPaaS delivery is rapidly moving to the forefront to enable overhead costs to be shared across processes that are not competitive differentiators and where cost has been growing (e.g. in compliance, reconciliation). Finally, where banks do not have domain expertise (i.e. Fintech), banks are looking to vendors to monitor industry developments in order to understand and deliver best practice.

Transaction products delivered at scale with automation

Retail banks will continue to adapt to new business models whereby they will offer a wider array of low-risk, transaction-based products (i.e. deposits, payments, and wealth management), which will be supported by more standardized, consolidated, automated operations across multiple markets, from very high scale delivery centers. And increasingly these will be delivered by third party vendors. Vendors will use their own platforms for delivering services, which will be highly automated. Manual processing will shrink aggressively as a proportion of the overall operations footprint.

Standardized global processing will expand in order to continue to reduce cost per transaction. High volume, standardized processing, enabled by automation, will allow pricing per transaction to become the standard pricing scheme in RB BPS. The shift to transaction pricing will allow banks to become nimbler, shifting their product mix in response to changing market conditions, and reducing the boom/bust cycle that has driven the industry in the past.

]]>- Margin: where profit margins are highest, usually with new processes or products where competition has not yet developed, speed to market is critical and cost is not a challenge

- Scale: cost can be reduced by applying operational techniques (automation, centers of excellence, or sharing of overhead) which leverage economies of scale.

Where margins have been thinnest and scale largest, BPS has flourished. Since banking regulations vary by country, banks have adopted outsourcing in the largest countries first. Recently, aggressive changes in regulations have spurred banks to focus BPS efforts on outsourcing compliance-related activities, which have a negative margin (cost, but no associated revenue).

Today, retail banks, the largest-scale adopters of BPS in financial services, are on the verge of a sustained increase in BPS adoption, as margins have aggressively contracted across product lines and standardization (driven by regulatory requirements which have been coordinated cross-country) has increased, and will continue to increase, significantly.

Each process in banking is unique and the degree of scale and margin varies significantly across processes. The three primary processes in retail banking are:

- Deposits: low margin, limited scale, multiple sub-products

- Lending: high margin, limited scale, standardization of syndicated/securitized products, high customization of retained loans

- Payments: low margin, very high scale, standardization across countries.

Based on the margin/scale characteristics, one would expect the earliest adoption of BPS to be in payments, which it is. Next we would expect sub-processes with the largest scale to be outsourced. Again, customer contact and account opening have been largest scale (with applicability across all processes). These sub-processes have been outsourced for deposits and lending. Loan administration in standardized loans (consumer mortgages underwritten by government programs) were the next processes to be outsourced. In the last three years banks have focused on outsourcing compliance processing, which has the lowest margins (negative), and largest scale (across all products).

The next stage in the journey

Bank offerings at a macro level are well established and will not gain new processing scale. However, reengineering of processes can develop increasing scale, as banks restructure their operations from a vertical (product-oriented) approach to a horizontal (customer-centric) approach. This is allowing banks to focus on standardizing customer interaction processes (which increased regulations encourage), which can then be delivered by third-party vendors.

Key technologies supporting this include:

- Customer analytics, which support bringing the ‘right’ product to a customer at the right time

- Robotic process automation, which supports highly standardized delivery of processes

- Mobile services, which support centralized service delivery, since mobile services are not delivered in person.

This focus on customer delivery will improve C-SAT and allow banks to deliver a much larger array of offerings to their customers, while keeping complexity of multi-product delivery low.

]]>Capital Markets Client with Broadridge

In this example, Broadridge is providing a post-trade utility for a global institution looking to become a primary dealer in the U.S. market, something which requires the creation of large operational delivery scale in fixed income. Provision of operational services is on a multi-tenant platform with support from U.S. fixed income domain experts.

Benefits achieved from this arrangement include:

- 35% lower TCO

- Increased STP

- Adaptability to remain current: new product offerings and reporting required for primary dealers

- Simplified connectivity to 70+ data feeds and global custodians/depositories.

Retail Banking Client with Infosys

In this example, Infosys is supporting platform renovation and providing BPS services to a major Canadian bank. The client’s challenge was three-fold:

- To identify savings from increased automation and BPS

- To transform their platform and train employees on new processes

- To reduce costs and improve process efficiency and accuracy.

Processes requiring improvement included deposit services, mortgage lending, virtual banking, wealth management, and investment services.

Benefits achieved from this arrangement include:

- Upfront cost reductions of 40% to 80% across most processes, primarily from use of tools and automation

- Significant cross-training during the transition phase

- Enhanced tracking of SLAs to provide the client with visibility into process quality

- Vendor committed to 25% improvement in process efficiency over three years.

Conclusions

In both cases, BPS vendors are supporting capital investment with technology they are using across multiple institutions. The technology is modern with an emphasis on increased automation of manual processes and STP. The multi-tenant environment ensures currency will be maintained because of demand from many tenants, and lowest cost of change due to shared overheads. The domain expertise of the vendors’ employees is enhanced by exposure to multiple clients addressing the same set of industry challenges.

The shape of operational workforces in this platform-driven approach to service delivery shifts from a pyramid shape (with the largest number of workers in the lowest skill jobs) to a diamond shape (with the largest number of workers in mid-level tasks, managing technology and robotic processing tools). Bots can scale transactions at a negligible marginal cost, allowing clients to achieve a lower TCO over an entire cycle (both seasonal and secular cycles). Cost savings are running at between 40% and 80% using this type of approach, as compared to the typical labor arbitrage cost savings of between 20% and 30%.

]]>- HCL and CSC: Two JVs were formed, whereby HCL will operate and expand the existing Core Banking business of CSC. The first JV will focus on account management and delivery governance while the second will focus on service delivery and product development

- FIS and Sungard: FIS acquired Sungard for its wealth and asset management solutions. The combined entity will focus on selling platform-based BPS services to the wealth and asset management industry, and leverage FIS’ existing retail banking clients for upsell (FIS has seven other public solution partnerships in capital markets)

- Broadridge and QED Solutions: Broadridge acquired QED to obtain software-based investment accounting solutions which will now be delivered in a BPaaS mode

- Wipro and Viteos: Wipro acquired Viteos to provide STP and post-trade BPaaS services for alternative investment managers

- Broadridge and Direxxis: Broadridge acquired Direxxis to acquire cloud-based marketing solutions for wealth advisors.

These deals are being driven by several key business factors in Financial Services:

- Capital scarcity for both financial institutions and BPS vendors

- Requirement for IP to support process reengineering which delivers cost reduction that increases with scale (operating leverage)

- Lack of client engagement staff to support business growth and C-SAT improvements

- Willingness of clients to accept standardized services for a much broader array of processes, which will drive BPaaS adoption.

Businesses at all levels (financial institutions, ISVs, and BPSs) have limited resources to pursue revenue gains and therefore have to adopt ‘sharing’ policies to succeed. Currently, qualified labor (i.e. domain expertise and the experience to effectively use that expertise) is scarce and expensive. To solve the twin challenges of cost reduction that increases with growing volumes, and client/customer engagement, all participants need access to large amounts of labor. This can only be accomplished by sharing the scarce resource. We will continue to see partnerships and acquisitions of the types listed above for the next three years. The result of these partnerships will be the restructuring of the BPS industry servicing the Financial Services industry. BPS will become highly automated and delivered in a BPaaS fashion.

Ultimately, industry consolidation (both financial and BPS industries) will be required to realize the gains from these new IP-based BPS services. The net outcome, to be achieved over the next ten years, will be:

- Financial Services will consolidate, with ~40% fewer firms. The survivors will be buying operations on a BPaaS basis, which will deliver 40% to 50% lower cost, but more importantly greater flexibility, allowing financial institutions to enter and leave lines of business much faster than is currently the case

- BPS vendors will consolidate, with 60% to 70% fewer tier one BPS vendors delivering industry-specific processes. Lack of proprietary solutions will make pure manual delivery cost-ineffective (~40% to 50% more expensive)

- ISVs for industry-specific solutions will struggle to survive independent of the BPSs who utilize their software. Most ISVs will either partner with operations vendors in multiple geographies or will merge with one of those vendors.

Criteria for success in payments processing

The payment processing industry is a mature industry characterized by very high transaction volumes, strict processing deadlines, and high levels of regulatory oversight. Hence, success in the payments processing industry requires vendors to have:

- The ability to process high volumes of transactions with short turnaround times

- Leading market share in individual markets, not global (multi-market) size

- Market-leading features/functionality.

In short, maintaining scale while driving additional functionality into its offering is what drives vendor success.

Key features of the transaction

The Equens financial processing business will be merged into a new entity owned 63.6% by Worldline and 36.4% by current Equens shareholders (and ultimately Worldline will acquire 100% of the shares). The new company, Equens Worldline Company (EWC), is expected to have 100m payment cards serviced and ~€700m in revenues. Key markets serviced include France, Belgium, Germany, Italy, and the Netherlands. EWC will have the largest payment processing market share in each of those countries post-merger.

Worldline will acquire 100% of PaySquare (Equens’ commercial acquiring business) for a cash payment of €72m (~$79m). PaySquare provides payment services to 50 financial institutions and acquiring services (in-country and cross border) to 120k merchants primarily in four countries: Netherlands, Belgium, Germany, and Poland. PaySquare is expected to increase Worldline revenues by ~25%.

Other features of the acquisition include:

- The bank/shareholders of Equens (ABN Amro, DZ Bank, ICBPI, ING bank, and Rabobank) will renew contracts for 5 years, creating ~€1 Bn committed pipeline of processing business

- The deal includes an option, starting in 2017, for Worldline to acquire any selling shares from Equens shareholders, and eventually acquire 100% ownership

- The number of staff with electronic payment expertise will rise from 1.7k to 3k employees

- There are targeted cost savings of €40m in infrastructure rationalization by 2018, and €15m per year in client-specific increased efficiencies by 2021. In addition, there will be one-time savings of €40m in synergy implementation costs between 2016 and 2018

- The deal creates an omni-channel business, combining card capabilities (Worldline) with non-card capabilities (Equens)

- An enhanced roadmap will result from consolidating and standardizing processing platforms, and reinvesting savings into enhancing features/functionalities of offerings (including client customization, country customization, cross border transactions, mobile, security, and analytics).

Outlook for the transaction

This transaction will be very important for the central European payments market. The impacts will include:

- Lower cost for EWC by ~4% to ~5% of revenues

- Creation of an unassailable leading payments vendor in five key markets: France, Belgium, Germany, Italy, and the Netherlands

- Creation of a springboard for Worldline to challenge incumbent payments vendors in key adjacent geographies, including Scandinavia, Eastern Europe, and Southern Europe. Success in those markets would create a dominant Pan-European payments vendor

- Greater resources available to develop payment functionalities relevant to the central European marketplace.

Card networks:

- Mastercard: +2.7% (2014: +13.5%)

- Visa: +0.8% (2014: +7.8%)

Payment processors:

- First Data: +2.1% (2014:+3.0%)

- TSYS: +18.0% (2014: +20.2%)

- Euronet: +11.9% (2014: +18.0%)

- Worldine: in euros, +4.0% (2014: +2.8%)

In every case, Q1 2015 revenues grew more slowly than 2014 revenues, with the exception of Worldline, which generates and reports revenues in euros, and has signed contracts in Latin America (e.g. Brazil and Argentina) which has driven very high growth in its mobility and e-transactions services.

In general, vendors had good revenue growth in North America and in emerging payments (e.g. mobile and e-payments). Whereas, vendors had weak or declining revenue growth in non-U.S. markets (especially Europe and Asia) and mature business lines (e.g. card issuing and card acceptance).

So what has changed?

Two key changes in the payments market have occurred:

- FX rates have changed (primarily, the U.S. dollar has strengthened), which has reduced the rate of growth, after currency conversion, in the highest growth markets for vendors

- Pricing of services has declined due to:

- Shift to lower cost transactions. This is especially true in mature markets where transactions continue to shift from high cost channels (e.g. checks, credit cards, wires, and cross border payments outside SEPA) to low cost channels (e.g. debit cards, EFT, prepaid cards, SEPA compliant cross border transactions)

- Aggressive cost reduction (e.g. renegotiation of AMEX/Costco contract to a lower cost contract at MC/Costco; various digital wallets, such as Google Wallet)

- Use of analytics to minimize cost of transactions via bundling, and improved cash management.

What does it all mean?

Established payments processors and banks have done a serviceable job of disrupting existing payments systems to drive increased growth in the payments market, while driving down user cost and maintaining margins. We believe that stage of the payments market is coming to an end and traditional vendors will now experience very aggressive challenges to their existing market positions. Future cost reductions will be so aggressive that margins will fall – by a lot. For example, Google Wallet charges customers nothing for its service (and hopes to recoup costs plus a profit from advertising). Given a cost of zero for transactions, it will be hard for a vendor charging on a per transaction model to compete without completely changing their pricing model. Full stop.

Established vendors are finding success in two key areas:

- Analytics: both corporates and consumers show a willingness to pay for analytics that help them to manage payments and their financial lives better

- Aggressive cost takeout: vendors experienced in emerging markets, where costs are already exponentially lower than in mature markets, are finding it easier to succeed in the payments market today. Mature market vendors who try to hold onto current pricing levels face large losses in market share. For example, the Costco relationship represented ~8% of AMEX’s spending volume. AMEX may wish to harvest profits from its existing base of business, but it will not survive in the long run unless it finds a way to maintain (and grow) its base of business in the face of reduced pricing and ultimately changed pricing models.

The next two years will see the battle of pricing models and analytics support for clients in the payments market.

]]>Looking at the recent financial results of six key incumbent vendors (four payment processors and two card schemes, all global vendors) highlights where the industry is going and what it takes to succeed. Below are results for the quarter ended September 30, 2014 (refer to NelsonHall’s tracking service articles for more detailed analysis).

How Payment Processors are Winning in the Current Environment

Headline results for payment processors are:

- Alliance Data: Q3 FY 2014 revenues of $1,319.1m, up 20.3 % year-on-year (yoy). International revenues grew at 23.5%

- Euronet: Q3 FY 2014 revenues of $453.4m, up 25.7 % yoy. International revenues represent almost all revenues (~90%). EFT services grew 28.6%

- First Data: Q3 FY 2014 revenues of $2,791.1m, up 2.9 % yoy. International revenues grew at 4.1%. Merchant services grew 0.3%

- TSYS: Q3 FY 2014 revenues of $552.9m, up 8.5 % yoy. International revenues grew at 12.2%. Merchant services grew 1.2%.

Vendors growing revenues (and profits) are focused on:

- Non-U.S. and non-mature markets growth

- Emerging services such as mobile payments, EFT payments (especially ATM networks in emerging markets), and P2P payments, including cross border money transfers

Among the payment processors, two vendors with winning strategies are Euronet and Alliance Data.

Euronet

Euronet's growth is the result of:

- Continuing expansion of its payments network (primarily ATM machines in India and Europe)

- Products:

- Electronic payments in Middle East, Germany, and India

- Money transfer, consumer to consumer, and Walmart2Walmart

The key to Euronet's success has been its ability to identify under-penetrated markets and pursue those opportunities. For example, Germany is not typically thought of as emerging, but its use of EFT is accelerating. Similarly, Walmart is a merchant with leading technology, but deployment of money transfer capabilities into retail merchant environments is leading edge in the U.S.

Euronet should continue to grow revenues in double digits just based on its existing footprint, which is not yet fully saturated. As it develops new initiatives, its revenue growth can accelerate further.

Alliance Data (ADS)

ADS’ growth is the result of:

- Growth of its loyalty programs in Canada and Brazil (Loyalty One in Canada, Dotz in Brazil, and BrandLoyalty/LoyaltyOne for grocers in Europe and LATAM)

- Growth of its merchant marketing programs in Europe and LATAM (Epsilon globally)

- Growth of its private card program, primarily the loan balances on the merchant clients’ private label cards)

The key to ADS’ success has been supporting clients in increasing their sales. ADS centers its offerings on marketing and sales support, driven from its proprietary technology and underlying transactions data. Payment processing, a core deliverable of ADS’ services, does not stand center stage in its value proposition.

ADS’ delivers services which are scarce in the marketplace, but not unique. For example, funding and managing card loans is especially important to merchants now that banks are withdrawing from that market. ADS is embracing this profitable business, while other participants are withdrawing.

ADS should grow its revenues in double digits by expanding into new markets in LATAM and Europe. Its Canadian market opportunities are saturated, by logo, but not by service offering. New analytics and payment types (e.g. mobile) should help drive growth in the Canadian market for ADS over the next five years.

Card Schemes Find Their Own Path to Success

Headline results for card schemes are:

- Mastercard: Q3 FY 2014 revenues of $2,503m, up 12.8 % yoy. Cross border volume grew 15% on a constant dollar basis. Total processed transactions grew 18.3% to 11.7 bn

- Visa: Q4 FY 2014 revenues of $3,229m, up 9.9 % yoy. Cross border volume grew 10% on a constant dollar basis. Total processed transactions grew 4.2% to 20.9 bn.

The card schemes face a somewhat different set of challenges because they sell highly standardized services, which are underpinned by massive capital investments, through card issuers (banks). Despite the limitations placed on card schemes by the nature of their underlying services, card schemes are finding the same drivers of success. Critical to growing the business is international markets and new services.

Mastercard has aggressively moved into emerging markets, staking out an aggressive growth strategy in Asia, Africa, and the Middle East. Key examples over the past year alone include:

- National identity card program in Nigeria with payments capabilities

- Electracard acquisition in India to expand processing services for banks in 25 countries

- Opening various delivery centers in Middle East and Asia

- Launch of a development platform in Ireland for ISVs to develop APIs and solutions for Mastercard processing services

These aggressive moves into markets and services have allowed Mastercard to grow revenues faster than Visa over the past year, and in the past quarter alone 28% faster.

Competitors Face Limited Window of Opportunity to Challenge Incumbents

In summary, the winners are moving into new markets and services. Critical new markets are emerging markets with little payments infrastructure and mature markets with legacy payments infrastructure where newer payments technologies (mobile, EFT networks) are starting widespread adoption. Establishing proprietary networks or distribution outlets (such as P2P payments) will create barriers to entry in the future and the opportunity for upsell of additional services, such as analytics.

Over the next two years, the window for competitors to catch up by pursuing these vendors will close. Already, presence in smaller countries, such as ADS in Brazil, makes it challenging for competitors to displace an entrenched vendor. Once payments vendors have created dominant market positions in major country markets, over the next five years, the payments industry will begin a consolidation phase in order to convert local leadership into multi-country leadership.

]]>Apple Pay supports credit and debit cards from the three major payment networks, American Express, MasterCard and Visa, issued by the largest banks, with ~83% of purchase volume in the U.S. Apple Watch will also work at the over 220,000 merchant locations across the U.S. that have contactless payment enabled.

Key benefits identified by Apple for the service are:

- Apple does not collect purchase history so purchases remain private

- Transaction security is improved. Card numbers are not stored on the device nor on Apple servers. A unique Device Account Number is assigned, encrypted and securely stored in the Secure Element on the consumer’s Apple device. Each transaction is authorized with a one-time unique number using the Device Account Number and Apple Pay creates a dynamic security code to securely validate each transaction.