Since my last ESG Market Assessment published in 2024, the public’s perception of ESG has declined due to public revelations that the carbon emission metrics used by many certifying firms are inconsistent, incomplete, and sometimes misleading. During the past year, ESG practitioners have shifted their emphasis from covering all three pillars of ESG to focusing efforts on sustainability. Correcting environmental data sourcing, analysis, and reporting will consume significant resources and provide a set of best practices for acting, tracking, and reporting once completed.

I recently spoke with Capgemini’s Sustainability practice for financial services to find out how their services have evolved and what their clients are doing to meet their sustainability objectives.

Sustainability Initiatives

Recent conversations I have had with financial institutions show they are continuing to pursue sustainability initiatives by working on:

- Data sourcing, remediation, and reporting. While the banks are implementing AI to source and analyze unstructured data, they are focusing less on AI initiatives and more on data lifecycle management and developing analytic frameworks to apply to the data

- Compliance reporting, which varies by region and requires constant change to keep up with compliance requirements

- Understanding and implementing supply chain tracking and monitoring of carbon footprints to manage overall institutional risk and understand the global impact of proposed remediation activities.

This has led institutions to adopt a more focused approach to their sustainability initiatives, emphasizing improved data management and prioritizing projects that address regulatory priorities. Currently, those priorities are:

- Extending sustainability tracking beyond the institutional borders to suppliers, buyers, and investments

- Reducing risk with improved tracking and reporting.

The application of these priorities varies by market, with the highest levels of activity in rank order coming from: Europe (the largest market for ESG services by far), Singapore, Australia, and the U.S. Because local market regulations and business conditions drive investment projects in sustainability, institutions have changed their strategy development and execution from a centrally-planned, enterprise-wide framework to a locally-planned and executed strategy with the flexibility to adopt best practices across the enterprise.

Capgemini’s Financial Services Sustainability Practice

Capgemini has found that institutions with mature sustainability programs are no longer focusing solely on compliance. They want to achieve additional objectives: mitigating climate-related financial risks and creating new sources of business value. To achieve these goals, they need to build a strong data foundation that will enable better risk modeling and product innovation. The goal of Capgemini’s sustainability offerings is to help banks move beyond a regulatory response to embed sustainability into operations, governance, and customer offerings. This enables the banks to turn environmental challenges into opportunities for growth and differentiation.

To meet this demand, Capgemini has developed a sustainability framework that helps clients embed sustainability across strategy, execution, and reporting. It employs a four-pillar approach, with offerings under each pillar:

Sustainable Enterprise, transforming operating models to reduce carbon footprint and costs. Key offerings include:

- Energy Command Center: an IoT- and AI-enabled solution that enables real-time monitoring, predictive maintenance, and optimization of energy and asset performance to reduce costs, carbon footprint, and operational risks

- Carbon Management as a Service: which delivers auditable, and near real-time carbon data across Scope 1, 2, and 3, enabling compliance, reporting, and abatement to accelerate net-zero timelines.

Reporting & Compliance. Key offerings include:

- ESG Lens: an AI-enabled platform that detects ESG data anomalies, benchmarks performance, and provides regulatory insights and scalable ESG compliance

- ESG Reporting: a lifecycle approach to sustainability reporting from roadmap design and data integration to processing and visualization.

Climate Risk & Transition, integrating climate in LOB’s growth and risk strategy. The key offering is business for planet modeling, simulating and computing climate scenarios, stress testing portfolios, and informing transition strategies to reduce financial risk and realize financial opportunity.

Growth & Customer Experience, increasing sustainability revenue and value delivered to end clients. Key offerings include:

- Business and financial impact of sustainability: advanced modeling and advisory services that link sustainability initiatives to EBITDA through integrated financial projections and scenario analysis

- Sustainable finance: a framework and services for deal-level integration, client and relationship manager support, ESG data insights, and tracking mechanisms.

Below are two client case studies showing how Capgemini is working with banks to achieve their sustainability goals.

Leading International Bank

The bank was an early provider of sustainable finance and has a large green bonds business. However, its retail bank provides limited sustainability offerings to customers. Further, due to a lack of active promotion by the bank to the retail customer base, only proactive customers buy those offerings. The bank wanted to proactively establish a brand presence for sustainable finance in the retail market and distribute its sustainable products from its retail branch network.

Using a mobile app with a gameboard of sustainable offerings, Capgemini positioned the bank as a Sustainable Trusted Companion. This proprietary app proposes sustainable choices and offerings with delivery partners at each stage of the consumer/enterprise journey. The bank can meet its sustainability goals with its retail customers relying on the app’s open banking network of delivery partners.

Global Banking Institution

The client wanted an automated platform for mapping EU sustainability reporting (CSRD) requirements across its supply chain. The goal was to simplify and consolidate reporting by evaluating multiple requirements and optimizing the final output.

Capgemini employed GenAI tools to create a map connecting 1.2k CSRD attributes and the bank’s sourcing partners. It then provided a remediation log to resolve unmatched attributes and an audit trail for all actions taken. Finally, it built and deployed a KPI scenario modeler to generate insights to optimize regulatory data.

The use of GenAI tools enabled highly accurate regulatory attribute mapping, provided a scalable solution across multiple sourcing providers and regulatory frameworks, and created a single source of reference.

Summary

Capgemini’s sustainability services help banks to move beyond compliance to use sustainability as a lever for risk mitigation and business growth. Employing its four-pillar framework of Sustainable Enterprise, Reporting & Compliance, Climate Risk & Transition, and Growth & Customer Experience, Capgemini combines technology and domain knowledge to deliver measurable improvements in sustainability. This approach builds the data foundation necessary for sustainability, regulatory alignment, climate risk mitigation, and business revenue growth; and it enables sustainability to increase enterprise resilience and competitive advantage.

By employing GenAI and relevant frameworks, Capgemini is enabling banks to analyze ecosystems, suppliers, and customers to improve business performance and reduce business risk. Importantly, the tools report to multiple stakeholders, allowing them to change behavior.

]]>

I recently completed a global market assessment of how GenAI and process automation are transforming banking operations. Here are some high-level findings.

GenAI adoption trends in banking

The adoption of GenAI and automation is still very immature, with large institutions being the only adopters of this technology on a large scale. However, the pace of maturation is accelerating, as demonstrated by:

- In 2024, the largest tier one banks worked on ~100 POCs each, and only 5% or fewer POCs moved through to operational deployment. However, in 2025, 25% of POCs are moving forward to operational deployment

- Tier two banks were doing only a handful of GenAI POCs each, with almost none moving forward to operational deployment in 2024. However, in 2025, tier two banks are looking for prepackaged GenAI POCs to deploy to operations. If those are successful, they expect to grow the scale of their GenAI activities in 2026

- Tier three banks are engaging in GenAI activities in two ways: enabling employees to test co-pilot agents to enhance personal productivity, but not interact with customers; and joining consortia that will develop GenAI offerings for their market niche

- Specialty financial institutions are running GenAI POCs to deliver low-volume, high-value processes. Examples include commercial banking, trade finance, investment banking, credit/investment analysis, and employee training.

The use cases being operationalized are software engineering, customer agent support, customer onboarding, credit/investment analysis, and personalized training. The majority of GenAI activity in financial services is in software engineering.

The challenge of becoming an AI-first business

Legacy financial businesses cannot become AI-first businesses without becoming fully digital, accessing relevant data as needed, and transforming legacy platforms. To accomplish those goals, banks are:

- Automating manual processes. For years, banks had automated high-volume, low-value processes to reduce costs. Now they are automating low-volume, high-cost processes, with the aim of automating all processing over the next decade. Generally, low-volume processes are for enterprise and high-net-worth customers. By automating these processes, the banks can generate clean data that can be analyzed by GenAI and agentic AI solutions

- Moving legacy systems to the cloud. Legacy transformation has been an expensive, risky, and long-term project. By moving legacy systems to the cloud, banks can break the process into smaller, less risky steps using microservices, APIs, and app marketplaces

- Adopting SLMs. Clean data is challenging to generate on a large scale. Early GenAI POCs have led banks to pursue SLMs, which are much easier and less costly to scrub and vet for high-quality data, thereby reducing the risk of GenAI hallucination.

Once processes have been digitalized and data scrubbed for a business process, such as credit analysis, the institution needs to develop a plan to change the business model, enabling the business to employ an AI-driven operational environment. As of today, only a few of the most sophisticated large enterprises are integrating business model change into their AI transformation initiatives. To achieve these transformation goals, banks are increasingly demanding change management services from vendors.

Summary

Successful GenAI and automation projects require rigorous control of business and data scope. By limiting the scope of a business process to a well-defined set of operational processes, the bank can source and analyze data effectively. A key example of this is credit analysis, which pulls in large amounts of data but performs analysis that is standardized for an individual institution. Similarly, software development consists of a series of processes that are standardized for an individual institution to create customized functionality. This is driving banks to increasingly work on developing SLMs rather than LLMs for their GenAI engagements.

The use of GenAI is rapidly evolving, and banks are insisting that their GenAI initiatives provide them with the ongoing flexibility to swap in new technologies as new leaders emerge. This creates large ecosystems and marketplaces for Fintech vendors. Service vendors and banks are developing orchestration and management systems, often under the rubric of ethical AI, to manage AI systems and report on their effectiveness.

I will publish a market assessment on GenAI and Process Automation in Banking in December that will delve deeper into this market. It will identify how the market is evolving, what services banks are buying to support their transformation efforts, and the benefits being realized.

]]>

In this blog, I look at the rise of private credit and Cognizant’s operational services that are tailored to meet the needs of the private credit industry.

The Rise of Private Credit

The creation and availability of alternative assets such as crypto, private equity, tokenized assets, and tangible assets, is expanding much faster than the overall investment market. Indeed, changes in regulations are accelerating the adoption of crypto, notably in the U.S. Managing these assets presents different challenges to custodians and asset managers than traditional asset classes.

The largest, fastest-growing alternative asset class is private credit. It has grown in real terms from $49 billion in 2000 to $1 trillion in 2023, according to the Boston Federal Reserve Bank. Market growth has been accelerating since 2019, and Prequin has forecast that the market will reach $2.6 trillion by 2028, with a growth rate of over 20% per year. This level of explosive growth has prompted regulators to take notice and initiate discussions about prudential risk management to ensure market stability.

Private credit presents different risk and management challenges than the traditional consumer credit products provided by conventional lenders. Private credit is provided by non-bank lenders primarily to commercial borrowers. This presents the following operational challenges:

- Borrowers are more complex credit risks requiring rigorous analysis and monitoring

- Lenders have less experience with the borrowers and a smaller operational footprint to deliver all processes

- Private credit often utilizes new deal structures to address borrower operational needs. These deal structures are typically not used by conventional lenders

- The lender (owner of the loan) is often different from the agent (originator and servicer), which necessitates clear and disciplined communication.

The difficulty in addressing these operational challenges is expected to increase when the economy deteriorates, interest rates rise, and individual industries enter cyclical downturns. Hence, private credit lenders are addressing their operational delivery needs by collaborating with technology and BPS providers to enhance the flexibility, scalability, and rigor of their lending activities. Cognizant’s capital markets division offers operational services tailored to meet the needs of the private credit industry.

Cognizant’s Private Credit Operational Services

Cognizant provides three groups of services depending on how the client approaches its operations delivery. They are:

- Operations and research services for clients who externally source BPS services, such as investment operations, credit/investment research, accounting services, and performance management

- Digital and transformation services for clients who externally source project management and point solution implementation, such as change management, project management office, process excellence, and custom solution implementation

- Technology services for clients who internally deploy technology but externally source maintenance services, such as platform upgrades and application/technology infrastructure maintenance.

Processes supported include:

- Data management and pricing (e.g., dealer quotes, asset rating updates, linking/syncing/subscribing)

- Investment operations and treasury (e.g., PIK processing, WSO settlements, sweep commission accruals)

- Accounting (e.g., BDC accounting, accretion income, carried interest, waterfall calculation)

- Reconciliations (e.g., borrower, cash, intercompany)

- Performance (e.g., VAR, scenario and factor analysis, stress testing)

- Reporting (e.g., borrowings/paydowns/rate fixing/rollovers, tax reporting)

- Investor services (e.g., review investor documentation and compliance checks).

Services typically start with fund accounting, cash/trade management, and/or reconciliation. The client will eventually expand its engagement to include investment operations and treasury management. Lenders have been slow to adopt credit research services; however, advances in GenAI are increasing the demand for these services.

Third-party provisioning of operational services for private credit works because the industry's volumes are rapidly growing at over 20% per year, while individual lenders have much larger fluctuations in processing volume due to the buying or selling of portfolios. At the individual loan level, executing these processes is very complex due to the idiosyncratic nature of commercial lending. Calculating cash waterfalls, extracting data from custom documents, attributing performance, reconciling, capital calls, and conducting daily settlements require a combination of domain knowledge and AI to deliver cost-effective, accurate results within deadlines.

Client Case Study: Credit Investment Group

Cognizant has been able to save clients thousands of man-hours of processing time across hundreds of private credit portfolios, while increasing accuracy and enabling clients to scale up/down operations as portfolios are purchased and sold. One such client is a credit investment group, for whom Cognizant provides governance and oversight of fund administration for 152 portfolios with $56 Bn in AUM. Processes supported by Cognizant include corporate actions reconciliation, daily cash reconciliation, and portfolio performance summary.

Benefits achieved for the client include:

- Automated data extraction from trustee reports: annual savings of 1,000 work hours

- Intelligent automation of daily P&L tracking updates across 52 funds: annual savings of 450 work hours

- Low-code automation of daily cash break analysis: annual savings of 300 work hours

- Automated reconciliation of PCO cash balance preparation using trustee data: annual savings of 250 work hours.

Cognizant uses Fintech tools to deliver faster processing in investment operations, such as:

- Canoe for document management: to automate document collection with APIs and RPA. It employs AI/ML to analyze data and generate valuations

- Vidrio for managed data services: to track risk exposure across asset allocations

- Chronograph and I-level for portfolio management: to create a unified view of cash flows

- Alleryx for automations: to automate cash reconciliation and prepare capital calls

- Workflows for control and audit: to implement fund administration processing on the Pega platform.

These tools enable better orchestration and analysis across complex alternative asset portfolios and processes.

Summary

Cognizant’s operational solutions for the private credit industry enable lenders and asset managers to address their two most significant challenges: providing flexibility to scale operations quickly, matching large swings in processing volumes and providing reach to orchestrate policies and procedures across large numbers of heterogeneous assets and portfolios. Cognizant employs advanced technology to pull, analyze, and report on relevant data from custom documents. This is ahead of the market, which is mostly experimenting with the best way to address these challenges. Cognizant will be able to apply best practices and use cases from private credit to other alternative asset classes to accelerate intelligent automation of the industry’s operations.

]]>

I recently completed a global market assessment of mortgage and loan operations services. I found that the mortgage and loan industry is restructuring at a faster pace than at any time since the Savings and Loan Crisis of the early 1990s, as mergers and divestitures have increased in size and frequency.

For example, over the past twelve months in the U.S., Rocket Mortgage has acquired Mr. Cooper for $9.4 Bn. This merger combines the largest mortgage servicer with the largest originator in the U.S. The combined company will service 10m mortgages, 17% of all U.S. mortgages, and Rocket Mortgage forecasts it can save $500m in operating costs post-merger. Elsewhere, other medium-sized market participants have divested their mortgage operations to focus on their core businesses.

The challenge of operational transformation

The lending industry remains a highly manual operational environment. The high cost of loan origination, increasing competition, and evolving technology is driving industry participants to automate processes and embed AI into their operations. The changing market environment, including shifting customer demographics (such as younger and unbanked individuals) and increasingly stringent enforcement of regulations (especially KYC/AML), is driving the acceleration of automation to accommodate significantly higher processing volumes.

Successful operations transformation requires change on a large scale. To make a big impact on operational effectiveness, lenders need to address three issues:

- Data: None of the emerging AI technology works without clean data from multiple sources. Data sourcing, extraction, scrubbing, and indexing from new channels and new ecosystems are required to enable an intelligent organization

- Agility: Lending is a cyclical business. Delivering cost-effective operations requires operations with a non-linear cost structure. Lenders need to move to hybrid multi-cloud delivery with high levels of process automation to increase operational flexibility

- Modernization of the operations estate: Lenders cannot simply rip and replace systems without undue risk and cost. Lenders need to develop a structured replacement strategy utilizing microservices, APIs, and app marketplaces to employ best-of-breed solutions for each sub-process.

Lenders have been applying these strategies to modernize origination and default management services, while loan servicing has seen less transformation activity. Where lenders have modernized their servicing activities, their efforts have focused on process automation and the modernization of collateral management.

Across all processes, the shift from manual to digital processing has delivered the highest ROI. GenAI promises to deliver additional cost and time savings on judgment-based processes, such as credit assessment, product offers presented to borrowers, and risk/security management.

Regional and local lenders are using managed services and BPS to mitigate their staffing disadvantage. Their focus is on buying standardized offerings to enable them to compete with tier-one and digital lenders.

Summary

The biggest challenge to transforming lending operations is the risk of implementation. Many of the most successful implementations have been done after an initial failed attempt with a previous vendor. Failed implementations often occur due to a vendor's lack of familiarity with a specific new technology and inadequate change management practices. Lenders generally avoid full platform replacement strategies in favor of phased modernization or decoupling of functionality. These strategies are easier to pursue using cloud delivery, which reduces risks by moving technology change management to the cloud provider, leaving business change management as an internal task.

Third-party vendors can provide valuable insights, best practices, and product selection services for emerging technologies, leveraging their experience with AI, automation, and cloud technologies, which is especially helpful to regional and local banks. These best practices are developing rapidly as FinTech and cloud technology continue to evolve.

I will publish a market assessment on transforming mortgage and loan services in July to delve deeper into this market. It will identify how the market is evolving, what services banks are buying to support their transformation efforts, and the benefits being realized.

]]>

In this blog, I look at the growing requirement for operational flexibility in banking, and at a specific KYC initiative from Capgemini aimed at addressing this.

Industry trends

Financial institutions and regulators are increasing their financial crime and compliance (FCC) activities for three reasons:

- The failure of Silicon Valley Bank (SVB), which highlighted the risk of balance sheets with asset/liability mismatches and liquidity risk

- The growing industry-wide expectation of a recession and/or market decline

- An ongoing increase in cyberattacks and fraud perpetrated by increasingly sophisticated actors

- A growing body of compliance regulations from many governmental entities across the world.

Industry trends toward cloud delivery, open banking, and financial product innovation (e.g., crypto) are driving the industry toward greater exposure to financial crime risks. Regulators in each country take a custom view on regulations. Collectively, regulators are raising the bar to demand a proactive response to real-time changes in customer risk assessment. Crypto enforcement in the U.S. is becoming more business-friendly, while the European Union has moved forward with comprehensive regulations aiming for tighter oversight.

As a result of these industry trends, financial institutions will need to transition from the current, heavily manual processes conducted primarily during customer onboarding to highly automated processing conducted continuously and based on a much broader range of data inputs.

Capgemini launches pKYC Sandbox

Capgemini acquired Exiger in October 2023, which accelerated the development of Capgemini’s Financial Crime Compliance offerings. Exiger was founded to oversee the monitoring of HSBC’s AML regulatory action. Capgemini has been appointed on the FCA skilled person panel as a result of the novation of a slot previously held by Exiger FCC to Capgemini. Its capabilities and direct regulatory participation led Capgemini to develop an offering that enhances Know Your Customer (KYC) automation, supporting clients with additional managed services. This enables them to customize their KYC activities while increasing operational flexibility.

Capgemini has developed an offering to address these challenges. Launched in April, pKYC Sandbox enables financial institutions to improve their KYC operations in four areas:

- Data sourcing and management: expanding the range of data sources, both public and private; applying the client’s taxonomy to the data; tracking and analyzing the data over time

- Event and materiality detection: identifying data changes at frequent intervals; applying a KYC/AML risk management policy to data changes; creating and using materiality triggers to the data

- AI and GenAI capabilities: employing AI, ML, and GenAI to create automated alerts, build KYC profiles, and validate documentation

- Enhanced workforce management: scaling KYC/AML alert generation and profile creation using AI and GenAI rather than labor; providing right-shoring services to scale manual labor cost-effectively.

The pKYC Sandbox enables each financial institution to transition from static KYC to trigger-based KYC in a manner tailored to meet its specific business requirements. The sandbox enables the bank to evaluate new technologies and procedures in a standalone environment, mitigating the risk of compliance failures or customer data breaches.

Capgemini has partnered with RegTechs and hyperscalers, including Encompass, Quantexa, WokFusion, Pega, and Google, to develop this offering. Capgemini has partnered with Microsoft to create the industry's first use case for AI-led Know Your Customer (KYC) transformation. Microsoft technology provides:

- Ability to efficiently source data from internal and external providers

- Multi-agent workflows with Azure AI Foundry to digitalize worker tasks

- Structured and unstructured document analysis and data capture using models from Azure AI Model Catalog and Power Platform AI Builder

- Copilot agents integrated into the processing stream

- Data-based risk assessment and reviews, eliminating multi-level QC processes.

Capgemini says the benefits of this offering include:

- First-year cost savings of 10-15%, increasing to 50% per year by year three

- Ability to customize by geography and LOB

- Ability to scale operations non-linearly due to increased process automation

- Creation of a golden source of KYC records

- Consistent execution with transparency to regulators

- Flexibility to adapt to new regulatory requirements.

Summary

Over the past five years, there has been a rapid increase in KYC/AML regulatory requirements worldwide. Financial institutions are struggling to keep pace with the rising costs of compliance. Capgemini has developed a customizable offering that leverages Microsoft AI and GenAI to deliver automated KYC assessments while maintaining visibility into the procedures used to create those assessments. As part of the service, BPS services are provided from right shore centers to deliver the retained manual processes cost-effectively. This enables banks to adapt their KYC operations to meet new regulations and changing business volumes.

]]>

GenAI is being tested by enterprises to identify the value it can bring to their operations. In 2024, the BFSI industry undertook more GenAI testing and POCs than any other industry. However, many POCs were unsuccessful because of limitations in data sets, processing power, and digital processes.

In 2025, large banks are narrowing the range of their GenAI use cases and launching full-scale operational deployment for them. The use cases banks are operationalizing are:

- Software development and modernization

- Agent support

- Process automation

- Document data extraction and categorization

- Employee training.

Software development, modernization, and maintenance are GenAI's highest adoption use case in the financial services industry, with GenAI reducing the delivery cost by 30% to 70%. The financial services industry is in cyclical high demand for software development and modernization as it adopts new technology architectures, responds to rapidly evolving regulatory requirements, and automates previously manual processes (a “digital first” strategy). So, what are vendors doing to help institutions operationalize GenAI software development to speed business transformation at scale?

TCS is helping institutions accelerate software development and modernization by embedding GenAI in its TCS MasterCraft offering, one of the software brands it offers to the market. TCS MasterCraft is a 2012-launched software and data modernization platform that delivers multi-modal software development and ongoing modernization of legacy applications. TCS MasterCraft uses AI to analyze data records and legacy code. In May 2025, it launched a GenAI-enhanced version to enable software engineers to:

- Interview software users more effectively identify processes with high automation potential by employing agentic GenAI

- Create legacy code summaries

- Extract processing rules and SOPs from code summaries

- Identify dependencies

- Customize new code design by industry and institution

- Write and test new code

- Extract processing rules and SOPs from new code summaries.

GenAI functionality will enable clients to:

- Identify processes to automate. Previously, people identified manual processes suitable for automation. Often, individuals had skills in either technology or business, but not both. By combining GenAI and people to conduct process identification, TCS MasterCraft is now able to improve process selection and enable more efficient resource utilization

- Build greater operational customization by industry, market, process, and institution, facilitating differentiation

- Enable reduced time to market for new products to harvest more of each new product’s lifetime value.

TCS will not standardize on one LLM set. This enables clients to work with the most relevant LLMs and switch between them in the future. Clients will be able to develop higher accuracy from their AI models from data-sourcing flexibility.

The BFSI industry has been the largest adopter and user of GenAI for software development to date, and already, 2025 is showing strong growth in the number of GenAI-enabled software development programs. Principal adopters are global custodians, global universal banks, and commercial lenders.

The hype around GenAI has been around building moonshot projects to deliver novel functionality. TCS MasterCraft's latest version is designed to deliver up to 70% greater efficiency, addressing the vast legacy application infrastructure constraints that banks face. Many of the legacy apps are written in COBOL, which increasingly lacks trained coders able to update and transform them. Success in automating code remediation will release billions in bank capital to address higher-value industry challenges.

]]>

In recent years, cryptocurrency (crypto), a digital currency that relies on a distributed ledger system to maintain ownership and transaction records, has emerged as a new asset class. Crypto has experienced the ups and downs typical of emerging technologies. In 2022, the demand for crypto hit a low, with the value of bitcoin dropping by over 74% from $64.4k on November 13, 2021, to $16.5k on December 31, 2022. Since then, Bitcoin has risen to $87.4k, a 430% increase.

The new Trump administration has accelerated the adoption of crypto, and President Trump has pledged to make the U.S. the crypto capital of the world. This is the first in a series of blogs on crypto that will focus on how financial institutions and technology services vendors are addressing the market opportunity and what best practices look like today. First, I will take a look at WNS’ initiatives.

The crypto challenge

There are four main types of crypto: payment (e.g., Ethereum, Bitcoin), Tokens (e.g., Ethereum), Stablecoins (e.g., Tether), and central bank digital currencies (e.g., digital yuan or e-CNY).

Each type of crypto has a different set of stakeholders, regulations, and technology architecture. Successful operations in each major crypto type require discovery, policy deployment, technology infrastructure, and business model build-out to enable successful, secure operations.

Regulations on crypto are beginning to emerge and vary widely by country. The organization with the most mature regulatory approach to crypto is the Financial Action Task Force (FATF), an intergovernmental organization set up by the G7. The EU has adopted the FATF’s approach to regulation in their MiCA regulation. Adoption of crypto by people and businesses remains low due to a perceived lack of security, which has been amplified by many examples of bad actors stealing or laundering crypto. However, the strength of crypto, which has no centralized manager or single source of failure, is also its primary challenge. The decentralized nature of crypto enables bad actors to game the system and commit various financial crimes.

So, what are the best practices for participating in a crypto environment?

The WNS approach

WNS provides a set of compliance services for financial institutions looking to operate in the crypto world. There are four service offerings:

- KYC: performing new customer onboarding and continuous monitoring (periodic reviews, perpetual KYC) of customers in establishing customer identity, understanding their background and activity, and identifying any potential risks, all to ensure compliance with regulations

- AML: performing AML investigations for crypto transactions by verifying trigger alerts, searching the customer for payments related to crypto, performing a KYC profile, and analyzing the on-chain flow of funds for red flags, if any, to report to regulators

- Fraud investigations: supporting client fraud investigation with triggers to protect customer funds/assets

- Customer query handling: replying to customer inquiries on crypto, verifying onboarding documents, requesting additional documents, and requesting clarification.

To enable the delivery of these services, WNS provides its employees with training specific to crypto-based security issues. Recently, it launched a Compliance-in-a-box service to support KYC, AML, Fraud, and SAR form preparation for suspicious customers. The Compliance-in-a-box solution targets Fintech firms that do not have the resources to deliver these services internally for the foreseeable future.

WNS is also building new services for crypto clients, including:

- Advanced Financial Crime Compliance (FCC) services: currently, all FCC vendors can analyze data from public sources (e.g., internet, media, and data vendors). Few crypto participants can analyze on-chain data for a Financial Crime assessment. The few institutions able to analyze on-chain data are global institutions that use the data for proprietary purposes. WNS will explore developing on-chain analytics solutions and integrate them with public blockchain data to provide FCC services customized for crypto assets

- Intelligent Customer Service driven by GenAI capabilities: providing high customer experience to end customers with faster onboarding and self-service capabilities through AI/ML-driven transformation/analytics solutions.

In summary, WNS and other vendors are developing offerings that will enable traditional asset analysis and management capabilities by adapting those tools to the crypto ecosystem. Key adaptations will be the data analysis of on-chain transactions and entities. Effective value analysis of crypto will require the analysis of data sets that do not impact the value of traditional assets.

]]>

Avanade laid out its strategy and roadmap for growing its business over the next three years at a recent analyst day. Avanade is an Accenture/Microsoft joint venture providing enterprises with IT services. In the 25 years since its founding, Avanade has delivered 37k projects to 5k clients. Its staff holds over 60k Microsoft certifications, including 68 employees with the Microsoft MVP designation. Currently, Avanade sources the majority of its business leads from its owners.

New Horizon targets mid-market

The company is launching a new strategy, New Horizon, to grow its business faster and become operationally more independent of its parents. It plans to focus its direct business development efforts on middle-market enterprises. Currently, Avanade’s client base includes middle-market clients, most of whom are direct-source clients. It defines middle-market enterprises as having revenues between $500m and $5bn. The market of mid-tier firms has thousands of enterprises and should offer Avanade faster growth opportunities than tier-one enterprises outside Microsoft and Accenture’s target markets. If the strategy is successful, it will grow to four times its current size in the next three years.

To accomplish these goals, Avanade is hiring salespeople to identify mid-market prospects and bring on 1k new clients annually. Engagements will start with 4-to-6-week projects, Halo Offers, which will identify Microsoft opportunities within an enterprise. These engagements will be expanded into Solution Plays, implementing templated solutions, or as-a-service engagements. By employing standardized delivery and rapidly scaling best practices across markets, Avanade will be able to deliver quality engagements while growing its sales faster than it scales its workforce. It will also need to shift its mix of full-time/contractor employees towards more contractors to be able to scale delivery to clients with higher sensitivity to seasonal and cyclical economic conditions.

Scaling sales and delivery will only be possible if Avanade’s offerings meet client requirements. Avanade’s mid-market clients prioritize:

- Onshore/nearshore delivery to enable mid-level managers to communicate requirements that enable their differentiated value proposition to the market and maximize client/vendor trust

- Defined solution frameworks to enable rapid deployment and scalability

- SaaS, cloud, and managed service delivery to allow them to reduce their commitment to internal resources.

Avanade is investing in building services for emerging technologies, with a focus on AI, including:

- Engineering services across emerging Microsoft technologies:

- Co-pilots and agents

- AI design and engineering

- Innovating customer experiences:

- Hybrid experiences

- Search (collective intelligence)

- Emerging disruptive technologies:

- Data fabric and core

- AI infrastructure and Edge

- Security and identity.

At this stage, Avanade’s offerings for the Biz Apps suite are its most industrialized offerings.

Financial services clients

The financial services industry is Avanade’s largest industry today, its client base consisting primarily of tier-one banks. The New Horizon strategy will look to grow in BFS in the U.S., Europe (UK, France, Iberia, ASG), APAC (Australia, Singapore), and Brazil marketplaces. Avanade can provide industry domain knowledge, which Microsoft does not offer. It can access Accenture’s industry capabilities and has a cost structure that allows it to deliver cost-effectively to mid-tier banks. To date, Avanade’s engagements with mid-tier banks have primarily been AI-based, cloud migration work, and application development modernization.

Key examples provided were AI-assisted customer contact use cases. For example, responses to customer inquiries must be highly accurate according to regulations. The AI contact agent can deliver high accuracy with ChatGPT 4.0-based technology or somewhat lower accuracy with ChatGPT 3.5-based technology. However, the license costs make 4.0 uneconomic for the client's use case. Avanade was able to engineer improved accuracy into the 3.5 technology to meet the high accuracy requirement. The client was able to save on licensing costs and make its use case highly cost-effective.

Conclusion

In summary, Avanade is looking to grow into the mid-market enterprise at a breathtaking pace. For perspective, the New Horizon initiative will grow its direct business revenues faster than Avanade grew its direct business in the first 25 years. Its best opportunities for success will be in regulated industries where competitors do not have the luxury of putting off decisions until it is economically convenient to implement disruptive technologies. Regulations in BFS are tightening with new regulations that shorten settlement times, increase risk management requirements, and require greater customer data protection. The pace of new compliance adoption provides a generational opportunity for a large services vendor like Avanade to enter the mid-tier market and gain market share with a strong value proposition. To succeed, Avanade will need to consistently deliver successful engagements while innovating new offerings and best practices across geographic and sub-industry markets.

]]>

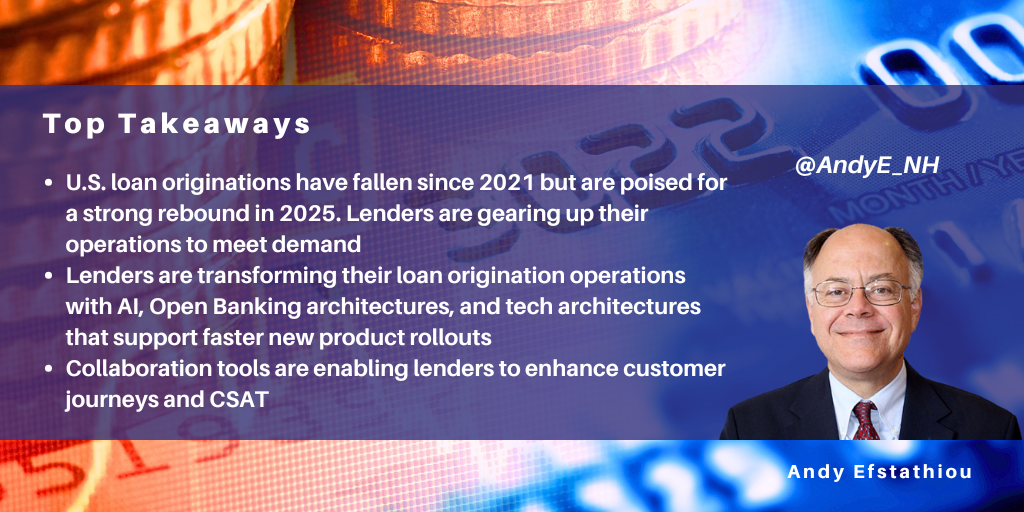

Global loan originations have declined since COVID and the trough of interest rates in April 2020. For example, in the U.S., loan originations fell from $4.51 trillion in 2021 to $1.50 trillion in 2023. Currently, interest rates in the U.S. are declining, and mortgage originations in the first three quarters of 2024 have increased by 9% over the prior year. The U.S. lending industry group, the Mortgage Bankers Association, forecasts a 28% increase in mortgage originations in 2025 to $2.3 trillion due to lower interest rates and increased home building providing consumers with a larger inventory at a lower net cost. Lenders are preparing their operations for a strong rebound in lending. This blog looks at some of the initiatives in play.

NelsonHall completed a survey of 60 financial industry executives in August 2024 about their intentions for operational transformation. Mortgage and core banking operations are the areas with the highest need for fundamental change (55% of respondents indicated extensive change is needed). Mortgage operations had the highest level of respondents (60%) saying they would increase their use of standalone operations transformation.

Lenders are looking to transform operations to drive revenue growth and capture the anticipated surge in origination volumes by:

- Using AI to enable hyper-personalization

- Using intelligent agents to enable customers and originators to shop a broader range of offerings and options efficiently

- Adopting flexible tech infrastructure to enable faster loan product introductions

- Implementing open banking architecture to enable partners to offer customers a broader range of financial products and services.

A recent example of the type of operational changes origination lenders are making is Florius, the largest mortgage specialist in the Netherlands, which wanted to simplify the application process for its customers. To meet this goal, it upgraded its systems to:

- Analyze incoming calls and route them to agents with customer-specific knowledge (typically an agent the customer has worked with previously)

- Integrate systems for customer contact, CRM, databases, and fulfillment

- Retain flexibility for future upgrades with APIs and open architecture.

The company did this by upgrading its Avaya Aura solutions for contact center, workforce automation, and collaboration platform (Breeze), which it integrated with its Microsoft Dynamics CRM system. It worked with NTT DATA in consulting, integration, and ongoing managed services to access expertise and upgrades.

Another example is when the largest mortgage lender in the U.S. wanted to redesign its customized, manual mortgage origination systems into a highly automated system that would deliver faster processing, lower error rates (significantly lower rejection rates), and greater scalability to address industry cyclicality. Working with WNS, the lender deployed Mozaiq.ai, an intelligent mortgage automation platform, and KnowRa+, an intelligent agent solution, to support the originators. The result was that the lender could reduce time-to-close, reduce costs, and improve CSAT and new business growth.

This is just a sample of what lenders are doing to prepare for the anticipated growth in lending. I am starting a global market assessment of operations and technology services in the mortgage and loan industry this month. The Transforming Mortgage and Loan Services project will delve deeper into how these initiatives develop, how lenders address the challenges, and how technology services vendors support their clients. The transformation promises to change the underlying lending business model across many geographies, making home and asset ownership accessible to new consumer demographics under more favorable terms than before.

Technology vendors with relevant offerings can contact me directly to participate in this study.

]]>

In 2025, the financial services industry will continue to build out its AI, GenAI, cloud delivery, and process automation capabilities. NelsonHall’s recent survey of financial services executives identified that:

- Operational transformation is highly important to 92% of retail banking companies and 93% of commercial banking companies

- Current operating models and processes at over half of institutions are not highly adequate to support key business lines, including payments, lending, and wealth management.

Banks will change how they pursue their business objectives in 2025, including in the areas of AI/GenAI, cloud delivery, and process automation.

AI/GenAI: operationalizing Small Language Model projects

In 2024, every bank wanted to investigate GenAI and appear to have an AI strategy. This resulted in many consulting engagements and POCs. Most POCs do not have a high ROI, and very few banks have operationalized any GenAI POCs. Furthermore, banks have discovered that successfully operationalizing GenAI using LLMs requires vast data, processing power, and energy consumption.

In 2025, most banks will decide that GenAI technology needs greater maturity before they invest heavily in operationalizing the technology internally. However, early adopter banks will move from testing the technology to operationalizing it in a narrowly defined set of use cases. The use cases will use Small Language Models (SLMs) to address internal operations processes such as:

- Software development, including more efficient generation of code documentation

- Hyperpersonalized content for marketing campaigns, such as generating thousands of unique marketing documents and emails personalized to each intended recipient

- Employee online training programs customized to each employee

- Email/document extraction and knowledge summarization

- Risk management, where banks train apps on special-purpose data sets, such as specific loan types used by regional/local customers, to identify risk characteristics and initiate early remediation activities.

While banks will operationalize GenAI use cases, AI efforts in 2025 will primarily focus on modernizing the data architecture. To improve the data architecture, banks will seek to:

- Define a data security architecture that is effective under a rapidly changing technology environment

- Decide what applications can be used in each part of a bank’s tech ecosystem (e.g., proprietary apps in the customer-facing environment and third-party apps in the internal facing environment)

- Decide where the data will be hosted and who has access.

Finally, banks will deploy AI embedded in processes to enhance corporate action resolutions, payment dispute resolutions, and prospect and at-risk client identification and prioritization.

Cloud delivery: standardizing faster delivery & embedding domain IP into hyperscaler solutions

Banks have been accelerating their move to the cloud. Over the past two years, most banks have developed target operating models (TOMs) and have adopted a hybrid, multi-cloud strategy. In 2025, banks will focus their cloud activities on:

- Migrating payments and securities trading to the cloud to improve cross-border transaction processing and declining settlement times (on the path to comprehensive real-time settlement)

- Standardizing and coordinating multi-country cloud delivery to provide a single-brand experience to customers

- Building joint solutions with hyperscalers, including:

- Cybersecurity and fraud solutions with industry customization

- Frameworks and solutions to deliver custom synthetic data sets

- Automation of data migration

- Automation of hollow-the-core processes.

Process automation for payments and lending

The adoption of process automation has been accelerating because:

- Cost pressures have accelerated the automation of manual processes

- The conversion of platforms to microservices has delayed the rewriting of solution modules, which will remain legacy for the time being.

In 2025, the focus on process automation will be on automating processes in lending (primarily origination) and payments (settlement, reconciliation, and reporting). This represents a significant shift from focusing on customer contact to transaction execution. By embedding AI in these automated processes, banks can complete transactions much faster, setting the stage for real-time processing, not just near real-time processing.

Summary

Banks are maturing their approach to using RPA, cloud, and AI in operations. In 2025, they will operationalize these technologies in tightly defined and rigorously controlled domain-specific use cases. GenAI will be deployed to address domain-intense challenges such as hyper-personalized marketing campaigns, employee training, software development, and document summarization. Cloud activities will automate migration, standardize TOMs, and migrate transaction processes. And finally, payments and lending sub-processes will be automated with embedded AI to address domain-specific requirements.

]]>

I recently attended the Genpact AI conference, where the Genpact employees I spoke to were energized by the changes AI is bringing and are focused on helping clients operationalize emerging technologies at scale. The company is investing in tools to provide greater ongoing feedback from employees: an HR executive described how they use an employee feedback system combined with a benefit awards system (like an airline's rewards program) to monitor employee satisfaction and identify ways to remedy shortcomings.

In this blog, I look at Genpact’s approach to scaling AI across the enterprise.

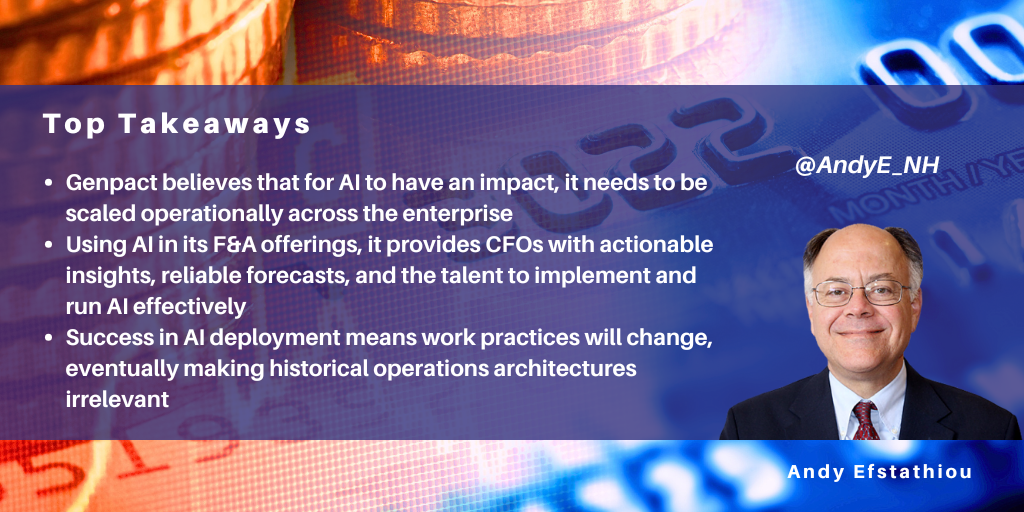

Scaling AI across the enterprise

Genpact’s AI focus is on the “AI of Now”. It believes that for AI to have an impact, it needs to be scaled operationally across the enterprise. Unlike many competitors, Genpact did not demonstrate futuristic AI functionality but instead focused on how it helps drive adoption across enterprises, presenting examples of operational deployment of AI to six clients. To grow its client base, Genpact wants to do more work with Tier Two enterprises, which typically have a more significant portion of their operations delivered with legacy platforms and manual processes.

To drive operational adoption of AI across an enterprise, Genpact believes there are three things required:

- Domain expertise: understanding industry-specific processes and data from working with those processes. Genpact has identified which processes and data it will work with for AI projects

- Technology ecosystem and expertise: building an ecosystem of product vendors is necessary to access emerging AI functionality. Executing successful implementations requires the tools, integrators, and technology knowledge that most clients do not have

- Dynamic talent: building an effective workforce to deliver these services requires training and creating cross-functional data, AI, and domain experts’ teams.

Practical AI applications

To build its AI services, Genpact surveyed what CFOs want from their technology investments, and found their top requirements to be:

- Actionable insights

- Reliable forecasts

- Talent that can implement and run AI effectively.

Based on this research, Genpact has embedded AI into its F&A offerings to enable CFOs to improve capital allocation and produce more reliable sales and profit forecasts with on-demand revenue and cost forecasts, fast decision-making with what-if analyses, and the ability to drive change in the trajectory of their business. Using these tools, enterprise clients can:

- Drive growth through AI-driven insights and data-backed decision-making

- Improve revenue forecasting, working capital optimization and planning

- Improve operational efficiency with AI-driven automation.

Genpact can develop better AI-based insights than any single client because it draws on a large pool of data from clients across multiple industries. Genpact’s business supporting F&A draws on its experience doing 500 quarterly book closes for 35k legal entities annually. The data and domain experience from this sizeable annual transaction pool enable robust predictive analysis and the ability to apply AI using keystroke-level process knowledge, thus enabling it to deliver outcomes to its clients. Similarly, Genpact has applied its considerable operational transaction experience to address supply chain and bank fraud challenges for clients.

New AI tools

At the conference, Genpact announced three proprietary tools for its AI ecosystem:

- Genpact CFO Actions Hub: the four key themes the hub will address are responsible AI, fine-tuning LLMs, the agent-computer interface, and how to retrieve & generate data that enables CFOs to transform data into cohesive narratives and enable forward-looking actions like scenario planning and forecasting. It uses LLMs and Genpact’s domain knowledge on a foundation of responsible AI to drive relevance with CFOs

- Genpact Agentic AP Solutions: the launch of four AI-based AP solutions, already live, with four AI-based AR and four AI-based accounts solutions coming soon

- Genpact Finance AI Academy: a set of training courses for employees and clients to improve their domain/technology expertise for the use of AI in finance.

In addition, Genpact’s GenAI solution, Scout, was on the conference app. It summarized each presentation soon after it had been delivered. This was a significant aid to this conference attendee because of the speed at which the summaries were sent out after each session. Presentation slides were also available on the app soon after each session.

Conclusions

Genpact’s AI strategy is to drive operational adoption of AI within enterprises to deliver business value. Operational adoption requires both client and Genpact employees to become familiar with AI technology and how it works in practice. Success in AI deployment means work practices will change, eventually making historical operations architectures irrelevant. Successful change management will need employee buy-in, and Genpact is building continuous feedback mechanisms to keep employees on board.

]]>

In July, I published a blog outlining the latest evolving practices in core banking platform transformation. In this new blog, I outline Capgemini's approach to addressing core banking transformation challenges with its clients.

The imperative of platform transformation

Demand for core banking platform transformation continues to proliferate to enable banks to:

- Reduce their operational costs

- Meet customer expectations and increase C-SAT

- Migrate operations to the cloud

- Enable FinTech functionality, including AI and GenAI

- Increase operational agility and bring new offerings to market faster

- Integrate operations into the emerging digital ecosystem and comply with open banking requirements

- Achieve faster and more accurate adoption of changing compliance requirements

- Improve risk management capabilities

- Achieve effective international expansion.

However, bankers are reluctant to start transformation projects due to many key challenges, including:

- Difficulty in running an operation environment while undertaking a renovation project

- High risk of project failure leading to career failure

- Complexity, cost, and long timelines to run a project

- Limited access to skilled resources to execute a project.

Capgemini’s approach to core banking transformation

Capgemini has developed a disciplined core banking transformation methodology to address the challenges to achieving a successful transformation based on six critical success factors. It addresses each of these success factors in its engagements as follows:

Effective governance model:

A project governance model must enable project lifecycle continuity. The governance team must include all relevant stakeholders, including the IT group, LOB owners, and third-party service providers. Bringing in the right decision-makers for each microservice is critical to keeping a project on track. Retaining an active governance board will mitigate the risk of project failure over time as people change roles.

Identifying functionalities embedded in the core platform:

Most legacy systems have poor functionality documentation. Banks need to identify functionalities, dependencies, and integrations. BIAN is the standard reference for an industry-standard banking framework. This process needs to be executed with speed and accuracy. Capgemini employs its IPs: CAP360, a legacy code analyzer, and BREAD, a GenAI legacy rules extractor. These tools typically deliver a 40% cost reduction in identifying functionalities versus manual identification.

Sequencing the decomposition of functionalities:

Their dependence on ledger systems must drive the sequencing of pulling out functions into modules. Banks should begin by decoupling systems, such as customer management, where multiple functionalities converge to deliver service. The second set of functions to be decoupled are the ones not dependent on ledger systems (e.g., compliance and payments). Finally, the bank should decouple functions dependent on the ledger systems.

Prioritizing orchestration investments:

A microservices environment needs to be able to link the modules to execute business processes. Rolling out an orchestrator requires prioritizing which functionalities to orchestrate first and what customization to build into the orchestrator.

Reinventing the target operating model:

To reinvent and execute a new operating module, the bank must assign the right team to own and manage individual modules continuously. It needs to coordinate how teams work to enable collaboration across modules and align their development roadmaps.

Linking business value to the transformation journey:

Identifying, implementing, and reporting agreed-upon KPIs and SLAs enables the stakeholders to remain committed to the project and identify remedies if objectives are not met.

Case study

Capgemini recently undertook a core banking transformation project for a tier-one global financial institution offering retail, wealth, corporate, and SME banking services in 50 worldwide markets.

Challenges:

- Long time-to-market for new bank products

- Higher customer servicing costs and inability to meet customer expectations due to a lack of digital banking capabilities

- Increasing inefficiency and high maintenance costs of heterogeneous and end-of-life legacy system operations

- The need to componentize a microservice-based architecture to be able to bring in best-of-breed modules

- Inflexibility of existing system.

Scope of services provided:

To support the bank’s discovery phase and baseline the operations architecture, Capgemini delivered architecture components including:

- Capability model covering all the capabilities aligned to the BIAN model

- Requirements catalog covering 2000 requirements aligned to the capability model

- Baselined scope, defining the markets, products, processes, and integrations to be covered

- Architectural blueprint covering designs for all infrastructure components.

Capgemini set up a Design authority covering:

- Architecture principles, critical design decisions, RAID Log, and non-functional requirements

- Data migration and coexistence strategy, migration options, co-existence scenarios, reconciliation and cut-over approach

- Minimum Viable Product (MVP ) definition approach and sample MVPs

- Roadmap for the next phase of architecture and design

- Functional, nonfunctional, and architectural inputs to the vendor selection RFI for selecting a new core product vendor.

Benefits:

- Defined core and non-core capabilities with ownership agreed with 50 teams across the globe for delivering non-core capabilities

- Employed a BIAN-aligned capability framework and a roadmap to define BIAN-aligned microservices

- Developed a global technology architecture that identified the applications that will deliver non-core functionalities

- Enabled componentized modules, which can be extended to all the bank brands and accommodate local requirements

- Identified existing initiatives the bank will need to change to align with the core banking transformation initiative

- Developed an operational drivers value map to identify the go-to-market proposition for the first MVP

- Identified the core banking product vendors with whom the bank would like to send an RFP

- Delivered a platform and technology perspective for the target state reference architecture

- Delivered a detailed design for the core banking transformation program.

Conclusions

In summary, most banks are pursuing a hollow-the-core strategy for core banking transformation. However, the success of that approach is dependent on bringing all relevant stakeholders to oversee the project and the ongoing evolution of operations. Rigorous prioritization of module sequencing based on business goals and process dependencies will drive value enablement; and orchestrating technology modules and operations units will deliver value to customers.

]]>

At its recent thought leadership forum, Confluence 2024, Infosys set out its roadmap for achieving a leadership position in AI services.

Despite the hype in the marketplace, Infosys finds its clients are taking a thoughtful approach to implementing AI. Clients want to carefully evaluate the realistically achievable ROI if they bring a project to full operational deployment. Once they identify high ROI opportunities, they fix the data infrastructure for a quality analysis. That requires fixing the sourcing, scrubbing, and distribution of data. Next, operationalizing the data analysis requires modernizing workloads, moving the workloads to the cloud, and experimenting with how AI can be applied to those workloads.

Successful application of AI requires leveraging domain expertise. However, to date, most AI vendors lack the domain expertise to enhance the practical application of AI to business workloads. Infosys is applying its industry experience to develop AI-based offerings for real-time payments, digital wealth management, and commercial banking in financial services. These process areas are characterized by higher levels of manual processing and higher customization across banks.

Infosys’ AI investments

Infosys is investing in six areas to build its AI capabilities:

- Data: tools, techniques, and services for sourcing, scrubbing, and analyzing data. Infosys uses its Master Data Management (MDM) solution for these functions

- AI functionality: enhancing its Topaz platform. Infosys is partnering with more Fintech vendors to develop emerging functionality

- Cloud migration: Infosys is enhancing its Cobalt platform and adapting its architectures and cloud delivery to more markets, including expanding its services for the Nordics, Southeast Asia, and the Middle East

- Engineering software services: Infosys has found GenAI very effective in accelerating its software development. It is taking these learnings and enabling client teams, primarily in large enterprises, to accelerate their internal software development. Shorter development times allow faster time to market for new products and quicker responses to cybersecurity threats

- Marketing: Infosys launched its Aster platform of AI-enabled marketing services, solutions, and platforms in June 2024. Currently, the platform has 400 assets and 50 partners

- ESG: Infosys has found that curating data and feeding the model are as important as building the best ESG model. It has accelerated its investment in these foundational aspects of ESG reporting.

Delivering business impact with AI

Infosys has found that a robust set of change management services is necessary to impact operational outcomes with AI. To increase business impact for clients, it is supporting its AI initiatives by:

- Enabling broad-based adoption by growing its AI and GenAI training offerings for its and client employees. These training programs include the application of domain requirements to AI solutions

- Scaling its Fintech partner ecosystem to provide clients with curated access to mid-tier Fintechs who are likely to succeed but do not currently have the scale for most enterprises to investigate. Banks are particularly interested in the vetting of cybersecurity Fintechs

- Providing clients with ready-to-use offerings by building out use cases that can be operationalized and developing productized offerings for tier two and three enterprises

- Building cybersecurity capabilities to secure AI. AI security presents a different set of challenges than securing data and transactions

- Customizing offerings to the unique characteristics of each market (e.g., Nordics, ANZAK, Middle East).

For the banking industry, Infosys is investing more AI resources in developing open banking offerings. Today, open banking is in high demand from European banks. Initially, Infosys is developing embedded finance and trade finance solutions for its open banking portfolio.

Finally, LLMs are in high demand in the financial services industry. However, institutions that have deployed LLMs are beginning to look to the deployment of SLMs (Small Language Models). SLMs are used for specialized tasks with limited data sets. LLMs require specialized hardware and cloud delivery to run. Typically, SLMs can be run on local hardware, often a cell phone, without cloud access. Specialized industries such as financial services will have many applications for SLMs, and Infosys is developing offerings for this emerging trend.

]]>

Banks are undertaking core banking transformation projects at an accelerating pace. Typically, two-thirds of these transformation projects will fail. Most either fail to implement a new solution altogether, leaving the bank with the original legacy system, or (in the case of a successful implementation), fail to deliver the anticipated value. Some projects, such as those at TSB Bank and Cooperative Bank, cause permanent impairment to the business and become the stuff of legend.

Since the risk of failure is high, why are almost all banks undertaking core platform transformation projects today? Driving the change is a rapidly evolving industry facing multiple challenges:

- Regulatory changes that require real-time transaction processing, open banking businesses, and expanded reporting, especially for fraud and risk

- Changing customer bases resulting from generational change and the banking of previously unbanked consumers

- New bank entrants, both established banks entering new markets and digital bank startups

- Technological change, including cloud, FinTech, AI, and distributed ledger

- High-cost structures requiring greater efficiency to enable those banks to remain viable.

To address these challenges, banks are pursuing three goals with their transformation efforts: developing low-cost access to quality resources, eliminating internal barriers to all corporate resources, and increasing operational efficiency.

Low-cost access to resources

Banks are pursuing the goal of providing low-cost access to resources by building ecosystems of vendors and partners with the help of technology service providers. To succeed, their platforms need to be able to plug in products and services from the ecosystem partners, so the banks are enabling optimum internal technology deployments by modularizing functionality within their platforms.

To do this, banks need a tech/business talent ecosystem to staff transformation projects. Finally, they need an ecosystem of third-party business partners, such as independent investment advisors, loan originators, and data vendors, to set up new businesses quickly and meet open banking requirements.

Eliminating internal barriers to corporate resources

Eliminating internal barriers to corporate resources is being achieved by rearchitecting core banking platforms into a microservices architecture, which enables the bank to change the operational structure from product silo-based to customer-centric. A customer-centric architecture allows the bank to deliver hyper-personalization of services to each customer. Critical to successfully removing internal barriers is changing how data is managed by improving data sourcing, scrubbing, and efficiency. Finally, embedding AI into a platform that can access all relevant data enables customers to shop complex offering portfolios more easily.

Increasing operational efficiency

The third goal of improving efficiency is being achieved by digitalizing all processes and documents. Banks are outsourcing more processes to convert CapEx to OpEx to align revenues and costs better. Processes are being automated with either digitalization or RPA. Where manual execution is still required, banks are implementing AI to reduce manual error, increase the span of control, and deploy consistent use of best practices.

Summary

The biggest challenge to achieving these goals is implementation risk, and the biggest challenge to successful implementation is change management. Banks mostly avoid full replacement strategies in favor of phased modernization or functionality decoupling. These strategies are easier to pursue using cloud delivery, which reduces change management risks by moving technology change management to the cloud provider, leaving business change management as an internal task.

Third-party vendors can provide best practices from other engagements in the industry, which is especially helpful to regional and local banks. These best practices are evolving rapidly as FinTech and cloud technology continue to evolve.

I will publish a market assessment on transforming core banking services in September to delve deeper into this market. It will identify how the market is evolving, what services banks are buying to support their transformation efforts, and the benefits being realized.

]]>

Financial institutions are data-driven businesses, and because of decades of investment in technology, banks process data using heterogeneous legacy environments. Modern AI and GenAI solutions promise to enable banks to manage and analyze data more effectively. However, adopting new AI solutions is lagging far behind the market hype. In this blog, I look at how TCS is helping clients address this challenge.

The Challenge

Banks must modernize their data management practices and technology infrastructure to adapt to fast-changing regulations, business models, stakeholders, and technology offerings. The scale and complexity of bank legacy data environments are a primary inhibitor to data modernization.

Most existing AI and GenAI projects are point solutions that deliver some benefits but cannot deliver business transformation. Further, when an AI solution is implemented, the highly siloed nature of large banks makes data analysis ineffective because modern AI, ML, and GenAI require the analysis of very large data sets.

For banks to adopt AI at the pace and scale needed to drive fundamental business transformation requires support from technology services providers. Essential third-party tools needed include:

- Taxonomies, frameworks, and use cases to identify where and how to implement AI solutions

- Ecosystems of vetted FinTech vendors to draw on for emerging functionalities

- Accelerators to drive effective implementation.

TCS’ Approach to AI Enablement

TCS has multiple offerings specific to BFSI customers and their requirements around AI. For example, it has developed Advanced Quantz & Analytics, an offering to enable clients to accelerate their AI journey, delivering services comprising:

- Technology and analytics engineering

- Business contextualization

- AI strategy consulting

- Design

- Innovation.

These five services are delivered as a package to identify combined business/technology requirements and implement transformative change. However, to reduce complexity and time to operational deployment, TCS is developing use cases and templates for AI deployment.

To support the development of use cases, templates, and offering development, the Advanced Quantz & Analytics team has built four COEs:

- Applied data science: delivers AI/ML solutions at the enterprise level

- Language and semantics: delivers GenAI and Deep Learning knowledge graph applications by partnering with graph producers

- Quantz: delivers quantitative solutions for market and risk use cases

- Analytics engineering: delivers process and ecosystem transparency for ML-based operations and orchestration.

These COEs have developed use cases that are segmented by time to deployment and business value:

- Time to deployment:

- 0 to 6 months: quick implementation to achieve rapid payback

- 6 to 12 months: medium-term implementation, which can be scaled across LOBs, silos, and markets

- Over 12 months: transformational engagements requiring major platform retooling

- Business value:

- ROI

- Customer impact

- User adoption rate.

TCS has developed ten categories of ML/AI models it wants to work with in BFSI, including sales, risk, financial forecast, and language models that are already fully operational, and others that are in development.

Advanced Quantz & Analytics has developed 147 use cases across eight asset classes, with credit and equity having the highest number of use cases developed to date. To operationalize use cases, clients have access to TCS’ ecosystem of 1k technology providers and 500 FinTechs in TCS’ COIN ecosystem.

TCS is working with 80 clients in BFSI to deliver AI services with the Advanced Quantz & Analytics offering. Most clients are large banks able to draw on large data sets, but many engagements require TCS to deploy synthetic data sets to enable effective ML and analysis.

Summary

AI and GenAI offer new power to enhance the value of bank data and transform many financial services business models. Identifying relevant use cases and implementing effective solutions remains challenging for the banking industry. TCS has developed an offering to support banks deploying AI and GenAI effectively and quickly. Its Advanced Quantz & Analytics offering has a roadmap for developing new use cases and toolsets to enable the offering to mature as AI technology continues to develop quickly.

]]>

I recently attended the EY Global Analyst Summit 2024, the theme of which was Rethink! The conference sought to answer the question, “How is EY rethinking the value it delivers?” and this blog looks at how EY is rethinking its activities in support of the BFS industry sector.