I was privileged to be invited recently to a customer and analyst event in Budapest, Hungary hosted by Cielo. Great, I thought – I’ve never been there, maybe I’ll see the Danube and a few historic buildings. And from that perspective, Budapest did not disappoint; it was understandable why there were so many tourists visiting, enjoying the hot September weather. But the event itself was a real eye-opener to the potential of this city and country, why it is a very cosmopolitan place to live and work, and why so many international organizations have set up offices/call centers here.

So what attracted an organization like Cielo to set up a delivery center (DC) here? On the second anniversary of the opening of its Budapest DC, Cielo’s Matt Jones explained why. At the time, when Cielo was hiring 10,000 professionals annually across 20 countries, many being in central Europe, it needed a DC location that would best serve its mix of clients. Cielo looked at a number of cities: Kiev, Ukraine; Prague, Czech Republic; Warsaw, Poland; and Budapest, Hungary. Of these, Budapest proved most suitable for Cielo’s DACH clients (those in Germany, Austria and Switzerland).

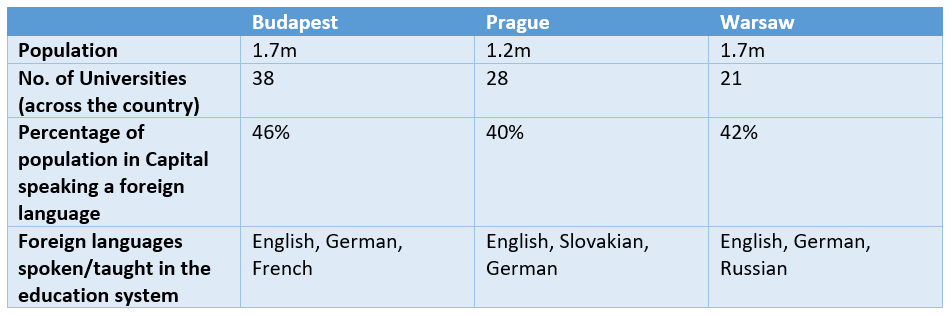

A number of criteria were taken into consideration. To ensure Cielo could live by its “we become you” high touch mantra for all of its European clients, it needed to hire qualified talent with strong bi- or multi-lingual capability. The table below shows the comparison between Budapest, Prague and Warsaw.

Whilst the three cities were strong regarding qualified and bi- or multi-lingual talent, Budapest better matched the languages used by its clients and had the greatest number of universities from which to source talent for itself and on behalf of its clients. In 2015, Cielo’s Budapest DC opened with three employees. Now it has 63 employees, speaking 18 languages (many employees speaking three or more), supports 17 clients hiring in 41 countries. The availability of local talent has enabled Cielo’s DC to scale quickly based on client demand.

The availability of such talent has been a key factor in other shared service centers (SSCs)/DCs being located in Hungary, as it is now the third largest SSC market (with over 100 SSCs) after Poland and the Czech Republic, as business process outsourcing has taken off in the region, with ongoing investments coming from Western Europe or the U.S.

Another advantage for Budapest is its location in the center of Hungary, at the crossroads of three main pan-European transportation corridors. According to HIPA (2017), Hungary has more than 1,800km of built motorways (with 690km planned), the third highest road density in Europe, and the fifth most dense rail network (7,712km). With 5 airports too, Budapest is a two-hour flight from most places in Europe. Budapest’s geographic accessibility was another key reason for Cielo to locate its European DC there.

Hungary also has the highest rate of broadband penetration among the V4 countries (a cultural and political alliance between the Czech Republic, Hungary, Poland and Slovakia) at 133% of the EU average, and the world’s third fastest 4G network speed (this maybe something to do with the fact that five of the major global network/telecommunications companies are located there), giving potential investors something to consider.

Cielo’s clients supported from its Budapest center come from the following sectors: engineering, technology, manufacturing, FMCG, pharma, medical devices, diagnostics, healthcare and insurance. Hungary itself has a strong presence in automotive engineering (with a $26.5 billion production value) with the likes of Audi, Mercedes Benz, Suzuki and Opel (and a further 39 of the top 100 automotive suppliers) operating from there, mainly based in western Hungary. The technology sector is strong, with 15 of the largest global technology companies (including IBM, Oracle and SAP) having a presence in Hungary, all having been there for over 10 years. The food industry is also a strong sector, with nine large companies investing in Hungary in 2016-17 (including Nestlé). This offers Cielo the opportunity to grow its client base in Hungary further, in industries with which it has a strong track record.

With the Hungarian government offering state aid (cash grants or tax allowances) mostly in either western or eastern Hungary in the areas of investment, training, R&D, and employment tax allowances, Hungary is likely to continue to attract international organizations to set up a presence there, giving Cielo further opportunity to grow.

So, at first glance, it seems that there are plenty of appetizers on Hungary’s menu to attract investors into the country. However, closer inspection reveals that some things are not so appetizing about the country’s labor market. Hungary is proving to be a highly competitive location in the war for talent, and over 70% of organizations are already struggling to attract the right candidates (source: Profession.hu, 2017). Motivators cited by candidates are a good salary, fair management/leadership, a stable workplace, fair working hours, and an interesting job. Candidate pain points are lack of useful information in job descriptions to make informed decisions about the role, and no communication from the hiring organization at the end of the hiring process. Profession.hu suggests that organizations need to embrace the concept of candidate experience, develop persona-based employer branding, leverage technology to speed up the recruitment process, provide the right information to candidates, and offer interesting roles.

Cielo, being one of very few talent acquisition vendors located in Hungary, is uniquely positioned to leverage its expertise with Hungarian-based organizations. So, Cielo – what are you waiting for?

]]>

NelsonHall recently visited CSS Corp’s contact center in Chennai, India to learn more about its operations and its current focus on developing its premium technical support services. The center opened in July 2010, supports 28 clients (primarily in the high tech and telecoms sectors), and has ~2,200 employees providing customer care, technical support, premium technical support, and analytics offerings.

Agent recruitment & advancement

In terms of agent recruitment, CSS Corp hires from colleges, and has a summer training program that sees approx. 65% of program participants go on to become CSS Corp employees. The hiring profile includes engineers and non-high tech customer care agents.

CSS Corp is working to address customer channel shifts from voice to chat, and this is reflected in its recruitment priorities. In recruiting customer care agents for chat work, CSS Corp is initially more focused on typing accuracy than speed, and requires candidates with typing speeds of just 20 words per minute minimum. Ideally, agents progress to 35 wpm, but speed is not a deal breaker.

Hired agents typically spend 12 months with the company before advancing to premium technical support, and currently there are ~380 CMS agents at this level. CMS agents can move up to engineering, enterprise, and applications positions, and these advancement opportunities are used as an incentive at recruitment time. CSS Corp has ~400 engineers trained in IoT and ‘smart home’.

Technical support initiatives

CSS Corp’s technical support initiatives include:

- Increased focus on automation, omnichannel, and analytics

- Increased focus on inbound sales, especially for a high tech electronics client

- Using social media (Facebook) to update customers of high tech clients in an effort to reduce calls to contact centers

- Encouraging collaboration with other providers to deliver strong premium level customer care – e.g. when other service providers are closely involved in providing support services to the customer, CSS Corp premium support agents will call the other provider(s) and conduct a joint call until the customer’s issue is resolved

- Focus on revenue generation for clients – e.g. in providing white labeled premium technical support for a global networking company, CSS Corp is working with the client to move from FTE-based pricing to outcome based-pricing.

CSS Corp’s premium support offerings are built on its Active Delivery Framework, which is supported by a suite of proprietary tools including:

- Active Edge – a social CRM and knowledge management tool providing agents with a full omnichannel CRM view of interactions in voice, email, webchat, and social media formats. This offering is not licensed as a stand-alone, but this could change in future based on customer demand

- Active-I – a support augmenting tool with proactive fault detection and resolution, asset intelligence, and call scheduler support

- Active Insights – a platform solution providing analytics and business intelligence support. It provides a unified view of the customer, and an analytical engine for insights and recommended actions, in an effort to drive cost reduction and revenue growth.

NelsonHall recently visited Convergys’ contact center in Bangalore to learn more about its operations, and here I reflect briefly on three areas:

- The center’s ongoing channel shift to webchat

- An interesting development in the center’s analytics work

- An initiative to hire more women in an effort to have a more balanced workforce.

Background

Convergys Bangalore is a 167,430 sq. ft. facility with ~1. 5k seats and ~2. 5k agents. It also has ten training rooms with 220 seats. Around 70 people are hired each week at the center, which operates 24/7 and supports telecommunications, cable, financial services, and high tech clients. It was established in 2003 and was the second Convergys site in India. The support provided from this site includes customer support, sales, and technical support. Convergys sees more room to grow in Bangalore, and is looking for a possible second site in another area of the city.

Shift to Webchat

Convergys would like to make its locations in India webchat CoEs. The webchat agent turnover rate is lower than voice, as webchat agents do not have to handle concerns from N. American customers of their clients regarding their accents. The move to more webchat agents also positions Convergys Bangalore strongly for the channel growth expected in chat.

Strong training in typing skills, multitasking, and prioritizing are needed for webchat agents. Common webchats can have standardized answers that should be personalized by each agent, not simply copied and pasted from a knowledge base. To improve service, Convergys maintains a library of the successful chats of top agents to see how they resolved issues. Convergys is currently providing webchat support for high tech and telecommunications clients from the Bangalore contact center. From a pricing perspective, support through webchat is typically priced on a per minute or a per webchat model.

Agents in the Bangalore center support Convergys’ clients’ customers in N. America, Europe, and Australia, and it hopes to support the India domestic market in the future. From a language perspective, it primarily supports English, but it also has 30-40 agents at this location speaking French, Spanish, German, French Canadian, and Italian.

Convergys Bangalore is using the Kenexa HR tool for all online applications and typing tests. As typing is not taught in Indian schools, ramping up typing speeds is often slow, typically taking agents three months to increase from 30 to 60 words per minute. During the first two weeks of training, agents focus one hour a day on typing skills. Typing skills are critical for not only call notes but for supporting the webchat channel. Convergys has a telecommunications client supported from this site that only wants agents focused on a single webchat at a time, but other clients are comfortable with agents conducting two and three webchats at a time.

Voice/webchat agents have about 8-9 weeks of training, including accent and culture training, which takes about two weeks. Agents also engage in experiential learning; for example, playing video games that help them to better understand the N. American financial services industry. Agents are also playing video games to get hands on knowledge of gaming companies it is supporting. In addition, webchat training on prioritization techniques is provided to teach agents to handle up to three webchats simultaneously.

Analytics with a Twist

Convergys is conducting some interesting analytics work from its Bangalore center, not only handling analytics for its own client’s customers, but also handling analytics for the clients of many of its competitors (where the end client has decided that Convergys is their preferred choice for analytics). After analyzing the calls, Convergys provides feedback on recommended improvements. This feedback is broader than many other analytics programs, as it encompasses interactions from multiple vendors.

Aiming for a More Balanced Workforce

Many contact center employees in India work evenings/nights to serve U.S.-based clients and customers. Contact centers are a vital industry in India, and the Indian government even mandates contact center organizations to provide transportation for female employees during the night. As part of the company’s ongoing efforts to have a diverse and balanced workforce, Convergys Bangalore is continually working to make it an easy choice for potential candidates. For example, Convergys has developed an app which female employees use to report back to the company when they have made it home safely; and female employees also have access to the Convergys Global Women’s Network.

Furthermore, CEO Andrea Ayers is highlighted in training videos as inspiration, telling her story of starting out as a trainer in a contact center and years later becoming CEO.

]]>EGS is a portfolio company managed by One Equity Partners (OEP), a middle-market private equity firm. Post EGS acquisition, Alorica will employ over 91k people in 154 locations across 16 countries in five continents. Lee will be CEO and Chairman of the new organization, based in Irvine, California. He will also be the majority shareholder. The companies expect to complete the transaction by early Q3 2016. The purchase price is not being shared at this time but Alorica plans to release this information over the next few months.

Lee founded Alorica 16 years ago with $10k and a vision. Fast forward to 2015, and Alorica had beome a $1.2bn company with the West Corp. Agent Services acquisition. And with EGS, Alorica will be generating ~$2.3bn in global revenue, behind only Teleperformance and Convergys as a pure play CMS BPO provider. In CMS BPO, scale is critical; clients want fewer partners, for one. By acquiring EGS, Alorica also avoids becoming a consolidation target.

Beyond the increased scale:

- EGS will expand Alorica’s healthcare sector business, reducing its dependence on the communications sector (currently its largest sector, accounting for ~28% of global revenues), healthcare, media/entertainment, financial services, and retail. It is also looking to grow its business in the technology, energy/utilities, travel and hospitality sectors. Alorica supports payers, providers, PBMs, pharmacies, and (to a small extent) medical device companies, providing primarily customer care and technical support services. EGS brings a number of healthcare industry accounts and pharmacy business. Alorica’s healthcare business currently represents ~9% of its total company revenue; it anticipates that this will increase to ~14% post-acquisition

- Alorica will benefit from the EGS collections business which will be branded under Alorica Financial Care. The focus will be first-party collections in the 30 to 90 day time period

- EGS also brings in some customer analytics capabilities offerings.

Just over a year ago, Alorica doubled in size with the acquisition of West Corporation’s Agent Services. The integration has been smooth, and Alorica claims that it has not lost any of the clients it obtained from West. One of the lessons learned from that acquisition was the importance of not over burdening its operations, HR, technology, and communications teams with integration work. With the EGS acquisition, it will have personnel dedicated to the integration, supported by McKinsey consultants.

Alorica and EGS have a limited delivery overlap. The network IP will be Alorica branded. It took one year to integrate West Corporation’s Agent Services business and the same amount of time is anticipated for the EGS integration.

Client overlap is 10-12 clients, from the communications, retail, and technology sectors. Post-acquisition, Alorica will serve ~600 clients, supporting ~30 languages. It will employ 52k people in North America (including 6k work at home agents), 26.3k in the Philippines, and 11.8k in Latin America.

EGS is Alorica’s second key acquisition in two years. In integrating West, it has learned to manage business integration smoothly, handle significant growth, and retain clients. Far from being a consolidation target, Alorica is becoming a consolidator.

One year on from my chat with Andy Lee, it’s good to see a leader articulate a clear goal and successfully lead a team on the road to making it a reality.

Postcript: This deal was completed on June 30, 2016.

]]>The report also reveals how voice interactions are increasingly being deflected to non-voice channels, primarily webchat, by high tech organizations. Complex interactions tend to remain in the voice channel, though some high tech organizations have moved entirely to a digital, non-voice, customer care and technical support framework. High tech organizations are experiencing reductions in product returns as a result of utilizing video chat and online videos for product installation.

The report identifies the following shifts in channel usage for outsourced CMS in the high tech sector between now and 2020:

- Voice/IVR usage decreasing from 87% to 65%

- Email decreasing from 23% to 15%

- Webchat increasing from 17% to 33%

- Social media increasing from 5% to 15%

- Video chat increasing from 1% to 10%.

The scope of outsourced CMS activity in the high tech sector has moved beyond customer care and retention, technical support, and collections/credit management, with increased emphasis now on revenue generation through paid-for technical support, analyzing end-to-end processes to reduce product returns and truck rolls, and enhanced installation support.

The report shares a variety of case examples quantifying how CMS vendors have delivered the benefits sought by high tech organizations from outsourcing. It also includes details of the current and future shape of CMS in the high tech sector, outsourcing drivers, vendor delivery capabilities, channel usage, market size and growth, and critical success factors.

‘Targeting CMS in High Tech’ is now available, along with a NEAT vendor assessment tool which enables sourcing managers to assess and compare the performance of vendors offering CMS services to high tech organizations. For more information, please contact Guy Saunders at [email protected]. You can also view a brief video with highlights from the report here.

]]>Alison Hilton, Deputy Director, Personal Tax Operations, HMRC, spoke about how her organization handles ~60m customer transactions a year, and decided to go digital to provide stronger customer care, and reduce customer effort. However, customer education was an important part of the transition: Hilton discussed how HMRC had to remind customers not to share sensitive personal information on social media, for example.

Katie Downs, Omni Channels Growth Partner at Barclays explained how they have embraced video chat to personalize banking. Barclays initially focused on ensuring a secure connection before offering video chat to its customers. It also provided specialized training to video chat agents, including what clothes to wear, how to fix their hair, and how to maintain focus on the customer on screen. James Gough, Social Media Operations Manager, Tesco, described the European retailer’s Twitter activity, having recently shared its one millionth tweet. Gough’s team responds to ~40k inbound social media interactions a week, ranging from store related questions and complaints, to customers just looking to find out information from the retailer. Tesco has been meeting its commitment to have its 180 social media agents respond to customers via social media within 24 hours.

I had the pleasure of sharing a session with Melanie Howard, Chair, Future Foundation, and we used our looking glass to see what customer care will look like in 2020. Melanie addressed the themes of responding to clients in a more personalized manner, and contact centers powered by robots with minimal human interactions. I primarily focused on where we see digital channel usage changing over the next five years and how business process outsourcers in the customer management services (CMS) market can assist companies in utilizing digital channels. The high tech and telecoms sectors are trailblazers when it comes to digital channel usage, and in my most recent report on CMS in the high tech sector, I identified the following shifts in channel usage between now and 2020:

- Voice/IVR usage decreasing from 87% to 65%

- Email decreasing from 23% to 15%

- Webchat increasing from 17% to 33%

- Social media increasing from 5% to 15%

- Video chat increasing from 1% to 10%.

Voice interactions are increasingly being deflected to non-voice channels, primarily webchat, with complex interactions tending to remain in the voice channel (though a small number of high tech organizations are utilizing only non-voice channels). Video chat still has obstacles in terms of the quality of customer/agent interaction, though it has proven to be of benefit in reducing truck rolls and providing installation support which can reduce product returns and cost.

The presentations at the CCA Convention showed how the adoption of digital channels is increasing and creating additional ways to enhance the customer experience. You can see a brief highlights video from the convention here.

]]>Groupe Acticall insisted that the Sitel management team remain intact as part of the acquisition agreement, as the majority of the team had been working together since 2009. And, according to Sitel CEO, Bert Quintana, “Sitel is here to stay with the support of a strong industrial investor.” Sitel will continue to operate as an independent entity.

Most of Groupe Acticall’s presence is in France, with some in Brazil, Ivory Coast, and Morocco, primarily in the contact center business, though it also has a professional services, digital services, learning CRM and IT offering.

Sitel has had organic growth of 8% y/y (Q2 2014 to Q2 2015), though it is behind in EBITDA: its competitive set has ~12% EBITDA compared to Sitel’s 8%. One major change with this acquisition is that Sitel will be less focused on quarter by quarter earnings, and rather more on annual earnings, due to the focus of its new investor. Groupe Acticall is interested in five to ten year plans, though Sitel will still have annual plans. Over the next couple of years, Sitel plans to double its rate of growth and increase its investments in research and innovation. And in the first year, Sitel plans for its 2016 overall capital spending to increase by 40% over its historical spending levels.

From a delivery perspective, France, Brazil and Morocco are the only delivery locations with operational overlap between Sitel and Groupe Acticall. Scale is important to Sitel’s clients, with 70% of its revenue coming from clients served in two or more countries; with this in mind it has opened several new contact centers this past year: Coventry (U.K.), a second center in Varna (Bulgaria), Porto (Portugal), and several in the U.S. (Knoxville, TN; Spartanburg, SC; and Pompano Beach, FL). It also recently opened a new contact center in the Tarlac, Philippines. As it continues to grow its delivery footprint, it is considering nearshore U.S. locations in Latin America.

Sitel is focused on growing its work at home agent (WAHA) support. It expects to see in excess of 20% growth in the next three to five years for its WAHA business as it is less capital intensive than its brick and mortar contact center business. Sitel’s WAHA delivery started in the U.S. and it is also providing WAHA delivery in Germany to fulfill a client need. It plans to expand WAHA delivery to the U.K. over the next year.

It is positive to see Sitel continue to focus on a range of industry sectors. Sitel’s win/loss survey data indicates that it is selected by clients due to its ability to show sector expertise. It is executing a sector strategy it began in 2014 in which it is working to grow its largest sectors. Its top five clients account for ~23% of its total revenue, while its top revenue generating client accounts for 6% of revenue. Sitel does not have a large dependence on a single client, as do many of its competitors (e.g. some depending on large telecoms providers, including Convergys, Sykes, and STARTEK).

Communications is Sitel’s largest sector, making up 39% of revenues. It sees further growth opportunities in the sector due to the amount of contact centers currently in-house, and is focused on showing clients and prospects how it can provide stronger revenue generation and CSAT increases than in-house contact centers.

Financial services is Sitel’s second largest sector, where they are expecting to see growth within its insurance client base. The third largest sector is retail, which is also the fastest growing. Sitel is supporting both traditional and e-commerce retailers, and also providing e-commerce support for its traditional retail clients. The retail business has the highest WAHA adoption rate of all the sectors Sitel supports, and it is in the process of hiring an executive with deep retail expertise to lead the sector.

Sitel is also focused on technology. It is investing in a cloud-based ERP (SAP) system for its financial and HR functions, expected to go live by the end of 2015. Sitel believes its legacy systems are why its SG&A is high compared to the market, and is looking for this technology investment to provide real-time data for decision making in an effort to lower its SG&A. In addition, it has hired talent management experts with SG&A constraints in mind.

It is good to see the Sitel management team remain intact, something that is helping them guide clients and employees through the transition. And, as the team evaluates strategic capital investments, they have clear growth ambitions. We wait to see how Sitel will fare under the new regime, but at this stage the indicators are positive.

]]>CSS Corp’s roots are in supporting the high tech sector, and while its focus remains on high tech, it is positive to see it branching out to closely aligned areas such as consumer electronics, retail, and telecommunications.

CSS Corp has two business units for its technical support services: enterprise and consumer, both primarily providing level 1 technical support, with some level 2 and 3 support. The consumer technical support business also includes an element of up-sell and cross-sell, and the company also has a small number of agents providing level 4 technical support.

When NelsonHall attended this conference in 2014, CSS Corp was developing a mobile and desktop application Active i to allow for easier consumer use of premium technical support. It had launched its Active Insights suite which includes real time feedback of findings to a client facing dashboard, support of voice to text analytics and machine learning, predictive analytics and performance management, and voice and video analysis. Currently, it has two clients using the full Active i suite.

CSS Corp continues to focus on analytics, launching its new analytics offering, Analance, during the conference this year. This offering uses structured and unstructured data to drive real-time feedback and simplify the customer experience. It recently signed a multi-year contract worth several million dollars for the use of cloud and analytics insights, which Ramesh believes will position CSS Corp as a key player in the market.

CSS Corp continues to aggressively market multi-device, white-label paid-for premium technical support (PTS). It is piloting an ‘Internet of Things’ (IoT) PTS contract with a networking client, and this technical support add-on service is an important part of its growth strategy. Its PTS platform integrates proactive support.

CCS Corp is looking to grow its PTS offering in the following ways:

- By partnering with OEMs to grow its technical support and premium technical support services. In Europe and North America it plans to partner with point of sale manufacturers (retailers) and carriers, to get paid technical support bundled with the device when sold

- By providing support for all devices sold by OEMs

- Through platform manufacturers, to integrate devices (develop products on platforms/use common protocols)

- Through partnerships with retailers and carriers, to provide premium technical support for all devices purchased from a store/carrier, as one ecosystem, in an effort to support the entire smart home.

While many vendors are focused on supporting the entire smart home, CSS Corp is slightly ahead of many of its competitors for its focus on platform manufacturers as well as how it plans to partner with point of sale manufacturers to get paid technical support bundled with the devices when they are purchased.

CSS Corp is putting a lot of emphasis on its analytics offering to enhance customer experiences for its clients’ customers, including piloting video submissions of trouble tickets with a high tech client (with customers submitting a video recording online in an effort to better explain issues to agents). It is also looking to use video support to assist with installation needs, which it plans to offer in future once a pilot has been secured. Instead of providing a generic video, agents will be able to provide support by having access to the same device as the customer in an effort to show how to install the product through a personalized video for the customer, and answer questions in real-time. The use of video communication puts CSS Corp ahead of the curve among many of its peers as it works to simplify the customer experience – though many of them are considering it to support high tech clients, they have yet to take action.

Company background

CSS Corp is a private company headquartered in Chennai, India. Currently, it provides technical support for enterprise and consumer products, manages IT infrastructure, provides remote infrastructure support including mobility solutions and cloud enablement, and provides carrier network support. It has ~5.5k employees across four continents, has 13 delivery locations, and supports 25 languages. NelsonHall estimates CSS Corp’s CY 14 revenues to be ~$220m, of which ~90% is from U.S. based clients. Last year, it began focusing on growing its business in EMEA.

]]>Minacs has ~4K employees supporting the automotive sector, with ~3.5K providing customer care and ~500 supporting marketing programs. Support is provided from delivery centers in the U.S, Canada, Mexico, and Europe, where agents with special technical skills support mechanics in the dealerships, and can see the customer relationship management (CRM) history of the customer. Minacs also has ~1.5k agents supporting an emergency assistance program for one of its automotive clients; many of the agents supporting this program are emergency response trained and have 911 dispatch certifications.

From a channel perspective, Minacs is using the traditional channels such as voice, e-mail, and web chat, but is also using video chat with its dealers for proactive and reactive communication (e.g. to allow agents to see a vehicle part being discussed). Minacs is also using digital and social marketing through advertisements on Facebook, Google, and Twitter for the OEMs.

Minacs provides marketing services for its automotive clients. This includes managing service reminders for vehicle owners, and using analytics to provide targeted offers to customers (e.g. targeting special offers to customers identified as not using dealerships for vehicle servicing). Minacs also cleanses customer data for marketing accuracy.

Minacs uses telematics to transmit data in real-time back to the contact center. Its connected consumer strategy leverages ALT CRM, a business operations model that utilizes big data analytics, algorithmic logic, and technology. Minacs developed ALT CRM as an alternative CRM model to support clients by predicting purchasing behavior, applying algorithmic logic to deliver timely and personalized messages, while utilizing multiple channels and devices for interactions. It also shares with clients insights gained from customers and vehicles through its support of emergency driver assistance, traffic and navigation, infotainment, usage based insurance, smart device integration, fleet management, and energy management.

OEM support includes mediation services, trade assistance buyback, service, parts, digital marketing, social customer service, marketing enablement technology services, affiliates rewards/owner loyalty and retention programs, rebates and incentives, outbound cross-sell/up-sell, customer acquisition analytics, and digital test drive campaigns.

Dealer support includes product and parts services, electronic parts catalog assistance, support of parts information center, warranty claims and recall inquiries, dealer inquiries and compliments, help desk and escalation technical support to dealer technicians, field assistance, outbound cross-sell/up-sell, customer acquisition analytics, and digital test drive campaigns.

Customer support includes welcome and education calls, customer lifecycle marketing programs, complaint management, vehicle location inquiries, customer care escalation, payment incentives, and warranty claims support.

Minacs anticipates growth in its digital marketing support service in the near future, as it is seeing growth in mobile and social support. It is seeing dealers moving television and radio marketing funds to digital marketing. Minacs has invested in its North American team and plans to focus on business growth in Asia as well. As it supports and sells services for offerings such as Sirius satellite radio subscriptions for OEMs, it is looking to package credit card processing and subscription marketing. On the financial side of the automotive business it also supports Ford and Honda credit/lease retention and looks to increase this business support as well.

In summary, while customer management services (CMS) in the automotive sector is not as mature as in, say, telecoms or high tech, Minacs understands that this is a growth area, as the needs of the digitally connected consumer continue to increase and vehicles join the digitally connected world.

]]>In March 2015, privately held Alorica acquired West’s Agent Services business for $275m in cash. In 2014, the Agent Services business generated ~$580m in revenue. Alorica anticipates $1.2bn in combined revenue for 2015, making it a top 10 CMS player globally.

West will continue its focus on the healthcare sector, and on analytics and technology, retaining its specialist agent services businesses, Health Advocate (a health plan advocacy services provider which utilizes agents, purchased in June 2014 for ~$265m), and its business-to-business, and cost containment services.

Alorica’s acquisition of West’s Agent Services business will:

- Expand its services offering, adding receivables management and direct response, outbound business, and consumer sales services

- Enable it to enter new sectors including healthcare, utilities, and government, and enhance its presence in the communications, retail, travel, financial services, and consumer products sectors

- Increase its delivery capabilities: Alorica will gain ~25.3k employees from West’s Agent Services business, of whom ~1.5k are nearshore (Jamaica and Mexico), ~5.4k offshore (in the Philippines) and ~18.4k in the U.S., of whom 5k are work at home agents (WAHA).

Over the past 5 years, Alorica has completed two other transformational acquisitions. They were:

- In 2010, Georgia-based Ryla, Inc., a provider of outsourced customer care. Alorica gained a significant number of employees from the acquisition

- In 2010, Florida-based PRC, LLC, a provider of outsourced customer care. Alorica increased its global footprint and gained ~10K employees from the acquisition.

Five months into the West acquisition, Alorica CEO Andy Lee described how he founded Alorica 16 years ago with $10k and a vision, back when it was ‘all about surviving’. Fast forward to 2015, and Alorica has gone from a ~$600m to a $1.2bn company with the West acquisition, and is launching a new brand campaign to create a new corporate identity.

Looking ahead, Alorica is aiming for 5% revenue growth in the next year. Lee’s goal is for Alorica to become number one CMS vendor (by revenue) serving North America.

Alorica highlighted its four core competencies as revenue generation, customer care, technical support, and receivables management, the latter being integrated from West into some of Alorica’s legacy clients. Alorica anticipates receivables management to be its highest area of growth over the next year. In future Alorica may also consider offering full revenue cycle management to its clients.

Entry to New Industry Sectors & Increased Delivery Footprint

The acquisition of West Agent Services allowed Alorica to enter two new industry sectors: healthcare and utilities. In healthcare it obtained contracts with two of the three largest healthcare insurance payers in the U.S. Coincidentally, both vendors were shortlisted for one of those healthcare deals, West having come out on top. The utilities business it acquired from West includes small contracts only, but Alorica plans to grow its utilities business.

The acquisition included a small amount of client overlap, mostly in the telecommunications/cable/satellite industry sectors. However, Alorica has been able to provide benefits to the overlap clients such as new site options and additional WAHA delivery.

Alorica’s WAHA delivery footprint was enhanced significantly through the West acquisition, growing from ~800 to ~5.8k home agents. All of the agents are currently based in the U.S., but based on client demand, Alorica may consider WAHA delivery from Mexico as well. Alorica will leverage the West at Home platform, Spectrum, to manage and grow its WAHA agent delivery capability, allowing agents to create their own schedules.

There are few overlaps in terms of delivery. In most cases, the acquisition has created an opportunity to fill open capacity. Jamaica and Mexico were new delivery locations added through the acquisition, and Alorica now has 48K employees working from 72 locations.

Summary

This is a pivotal growth move for Alorica, and the company was able to point to several examples of clients benefiting from the move, including:

- A legacy U.S. retail client is now adding WAHA services from West to solve e-commerce staffing peaks, and is also taking advantage of West’s more sophisticated collections offering

- A legacy U.S. telecommunications client is now using the WAHA delivery to cover peak times, starting with a small pilot

- Another large U.S. telecommunications client, finding itself out of capacity with West Agent Services, was able to add brick and mortar capacity through Alorica.

This acquisition has more than doubled Alorica’s revenue, increased its headcount especially for WAHA delivery, added new service offerings such as direct response and receivables management, increased its delivery footprint, and expertise, and allowed for entry into the healthcare and utilities sectors.

]]>Clearly, this was a fire sale, presumably of an unprofitable business. We were intrigued as to why HGS was buying further Indian contact center business - and indeed there is a story behind the announcement. The main reason for the acquisition is to more broadly expand the domestic Indian business as well as add banking and financial services clients. This domestic Indian expansion will help HGS handle domestic India business for international accounts (it recently won some business in India for a global CPG client).

HGS is picking up two telecoms clients, which together account for ~88% of the acquired business, plus four insurance and banking sector clients.

This acquisition may have been opportunistic, but it has some other benefits:

- It will significantly expand HGS’ footprint for servicing the India domestic market (India CMS BPO accounts for ~6% of HGS global business, its India payroll business another 2%). As well as adding to HGS’ existing nine cities with contact centers (with ~7800people) for domestic business in India, the Mphasis centers will bring in delivery capability in the northern Hindi-speaking states in India

- HGS will also acquire some premium level support capabilities for the Indian telecoms sector – for services which are often slightly less price sensitive

- And it will provide HGS with some referenceability in the key CMS BPO banking and insurance sectors. Expect HGS to look to win more BFSI BPO business in the region.

In short, what is a fire sale for Mphasis looks like as if it as the potential to become a great asset for HGS.

]]>It comes as no surprise that Onex is selling its stake in Sitel. What is perhaps a surprise is the size of the company making the acquisition - and the price.

Groupe Acticall, a national player in the French CMS market CY 2014 revenues of $196m, has grown through largely inorganic means since its inception in 1994. t is owned by Creadev (55%) and founders and exec officers Laurent Uberti, Olivier Camino and Arnaud De Lacoste (45%).

The much larger Sitel Worldwide has been majority owned by PE firm Onex Corp. since January 2007 when ClientLogic, which Onex owned, merged with the larger Sitel. Onex has to date invested $320m into Sitel. Onex’s general strategy would be to realize an investment of this nature by 15 years at the latest. In this case Onex has decided to sell its stake in a company that has been struggling with profitability for years.

In mid-2013 Sitel restructured to support a focus on higher margin activities such as its SaaS offerings, transformational CMS contracts (such as the win with TDC in September 2014), WAHA, multi-channel and social media support. By the end of 2014 these measures had not yet had a chance to have much effect, with Sitel’s operating margin reducing from 4.6% in 2013 to 3.4% in 2014. Q1 2015 performance was more favorable, with revenues up 1.2% y/y, up 10% in CC, to $355m, and operating margin up 1.6 pts to 4.4%. The company has been exiting low margin/unprofitable contracts and closing some contact centers, while opening others (e.g. in Nashville, TE, Pompano Beach, FL, Coventry, U.K. and Bulgaria).

At end Q1 2015, Sitel had ~ 59k employees, with approximately 41.4k in the Americas (which includes APAC) and 17.6k in EMEA. The company has 108 contact centers across 21 countries.

Following the acquisition the combined company will have ~68k employees and 128 contact centers globally.

This is a fire sale by Onex, the purchase price of $55m representing just 1.1 x 2014 EBIT and a fraction of its $1.44bn revenues.

Sitel was the fourth largest CMS vendor (in terms of CMS BPS revenue) in CY 2014. This is a reverse takeover with the well-established Sitel name being retained and its current management team remaining in place… though it is not yet clear where the combined entity’s head office will be. Like Teleperformance, the largest CMS vendors globally, Sitel will have French ownership.

We look forward to hearing more about the strategic intentions for the future Sitel & Groupe Acticall.

]]>While the concept of isolated sales-focused call centers is nothing new in the outsourced CMS space, the way in which IC conducts itself, especially now that it is a division of a large CMS pure play, is particularly interesting. IC seems to have maintained its “small company“ agility and go-to-market strategy; for example, the vast majority of the division’s contracts are run on a pure outcomes-based pricing model, a concept that many of the larger CMS vendors would baulk at! This pricing model is also reflected in agents’ compensation, ensuring an incentivized and motivated workforce.

The division has also proved to be an early mover in adopting and developing some of the more interesting and actionable analytics and agent-facing platforms. IC has developed a customer profiling tool, icConsumer, which uses a combination of data sources, including information entered online by the customer prior to an outbound call, multi-channel contact history (including previous purchasing information), lifestyle and interest data gathered from social networks, and data from third party providers. The aggregated data from icConsumer is segmented, then fed into icDial, a managed dialer service which proactively prompts an agent to call a profiled customer at a particular time.

Once an agent is speaking to a customer, another tool, icEngage, displays relevant customer information, including age, gender, marital status, number of children/dependents, interests, a geographic map of the customer’s location, local weather and local news. With this information agents are able to build rapport with the customer before using the customer’s spending history to make the most relevant suggestions for an initial sale. Once the initial sale is completed, agents can then use information such as number of dependents, marital status, interests, etc. to make up-sell and cross-sell suggestions – e.g. family contracts, insurance, or extra data bundles if selling on behalf of a telecom client.

IC currently has clients in the telecoms, BFSI and utilities verticals. For a large U.K. telecom, IC has become a major sales channel, operating 100% of the client’s outbound sales, accounting for a third of the client’s new contracts per annum. For this client, IC-acquired customers generally remain ~20% longer than customers acquired through the client’s other sales channels. Similarly, for another large U.K. telecom, IC acquired the equivalent of ~300 high street stores.

Moving forward, Convergys is planning to target the U.S. market by opening additional IC centers in the U.S. and the Philippines later on this year. Convergys is also looking to sell IC technology, including icConsumer, icEngage, and icDial on a SaaS basis in the future.

Given that the vast majority of its contracts have an outcomes-based pricing model, which is then filtered down throughout the organization, IC has fostered an entrepreneurial and sales-focused mindset across its operations. This high-pressure, results-driven environment, which requires a particular type of agent, can often lead to extremely high attrition levels; however, IC’s attrition of between 5%-7% per month is better than would normally be expected of a large outbound sales call center.

See related article Convergys to Acquire Stream Global Services, Becoming Number Two CMS BPO Vendor Globally

]]>Founded in 1993 and headquartered in Jeffersonville, IN, Accent has 2.3k employees and delivers services from six locations in the U.S. and Jamaica. It has 18 clients in the telecoms, technology, retail, financial services, and consumer products sectors. Current annual revenue run rate is ~$67m, hence the $16m purchase price indicates that it is not a profitable company.

The acquisition is expected to close by the end of May, and STARTEK expects the majority of the integration to be completed by year end 2015. With the addition of Accent, STARTEK will have ~50 clients and ~14k employees operating in five countries.

This is an important acquisition for STARTEK. Not only will it broaden its client base and sector mix, it will reduce its heavy dependence on the telecoms sector, which has accounted for ~80% of total revenues, and where it is exposed to vendor consolidation and reduced contact center volumes in the industry. Just three clients (T-Mobile USA, AT&T and Comcast) account for nearly 60% of global revenues, and in Q1 2015 STARTEK was impacted by a 30% revenue reduction from AT&T. STARTEK has been close to bankruptcy several times in the past four years, and has had to close several of its call centers, most recently in Oklahoma and Costa Rica.

The acquisition will boost global revenues by around 26%, and enhance STARTEK’s omni-channel customer engagement offerings. Accent’s customer engagement agency model will complement and enhance the analytics capabilities gained with the acquisition of Ideal Dialogue in 2013.

STARTEK has clearly been focused on diversifying its client base, having signed $10.5m of new business in Q1 2015 across clients in healthcare, financial services, and consumer products. However, it is the acquisition of Accent that will be the key determinant of STARTEK’s future success as it looks to shake off its dependence on the telecoms sector.

]]>For analytics, a popular claim is the use of big data for predictive modeling within contact centers. But is it really happening? The reality is that, while certain vendors are using data for simple predictive modeling, this is still a distinct differentiator among vendors and there is significant room for improvement. It is simply too early to claim that vendors are systematically using big data for predictive modeling.

An example highlighting this is a contract with a telco in which big data (including multi-channel contact history, lifestyle information from social media channels, information from third-party reference agencies, and customer local data such as weather and news reports), are simultaneously displayed via infographics and text to an agent’s desktop to help the agent better understand the consumer’s needs, build greater rapport and, in revenue generation contracts, retain, up-sell and cross-sell to a greater degree. However, in terms of predictive analytics, the data presented to the agent suggesting offers for the customer is based only on previous spend history and does not combine all of the above-mentioned big data sources.

So, are real-time analytics solutions currently being used in contact centers to either change agent behavior or provide customized offers to consumers?

While there are some interesting real-time analytics applications currently being used, this is limited at present. One example is a platform that analyses offshore agents’ rate of speech and displays the ‘sweet spot’ for this via an avatar on the agent’s desktop. This is done in real-time and assists with rapport-building with customers through the NLP technique of matching and mirroring.

Another innovation being piloted is a voice analytics platform that tracks a consumer’s words, phrases, and voice stress levels. These can then be used for compliance and industry-specific regulatory requirements in outbound campaigns, whereby a prompt appears in real-time on an agent’s desktop to recite a compliance statement, or proactively offer to remove a customer from a calling list if the customer is becoming stressed.

The move to using this type of real-time analytics for personalized offers and promotions is underway, but it will be a while before it is widespread.

Another common claim from CMS vendors is their ability to deliver transformation in their client contracts. What is the reality?

There has been a shift in recent years in how CMS transformation is delivered. When CMS was largely about agent numbers, a vendor would look to incentivize agents, improve training, and look to hire more skilled agents, in order to improve service delivery and reduce costs.

Then, about five years ago, there was a big shift: multi-channel, analytics, and social media became the new transformational levers, and are now considered an essential part of CMS delivery, though by no means have these yet reached maturity. Also, now that agents have access to increasingly complex customer data, and customers are now only interacting across live agent channels for high-complexity queries, the quality of the agent delivering this service is vitally important. Therefore, most of the transformation we are now seeing revolves around the HR aspect of service delivery. Training complexity and length is increasing, with many vendors now adopting a continuous agent learning and development scheme within their operations. And with the additional training investments vendors are now making, attrition is becoming even more costly; hiring agents who are more likely to deliver a high quality service, and stay with the company, is now more important than ever.

Hence, behavioral-based hiring methods are now been used in transformational deals over traditional skills-based hiring approaches. These methods are able to identify agents who might not have all of the required skills, but who have the correct mindset with which to learn and improve, and are more resilient. This type of hiring approach is already proving to reduce attrition levels and improve initial KPI adherence.

In summary, there’s no shortage of big claims from CMS vendors about the extent and effectiveness of their offerings in the areas of analytics and transformation. And big changes are happening in both areas, but not always quite as the vendors would have you believe.

]]>In total, 24 languages are supported, and the center is able to draw upon London’s rich cultural mix to recruit students and recent college graduates with broad language capabilities.

In the government sector, HGS runs a multi-channel helpline for the U.K. Visas & Immigration department, supporting people in 222 countries in 21 languages through voice, e-mail, webchat, and self-service. It provides customer care as well as market insight and reporting for this client.

In the automotive sector, HGS agents utilize video chat in addition to traditional channel support such as voice, e-mail, webchat, and social media, to provide sales and road-side assistance to the European and Middle Eastern divisions of a luxury automotive client. HGS has found that customers consider webchat to be impersonal, and is planning to extend the use of video chat beyond the client’s U.K. customers to Europe over the next year.

The Chiswick center supports several bespoke client programs that go beyond traditional customer care. For example, HGS is conducting on-site product testing as part of complaint handling for a global client in the CPG sector. In a recent instance, HGS tested one of the client’s consumer products (bottled bleach) in order to determine whether the product cap was defective as part of a customer complaint; on this occasion it was able to establish that the product was not defective, though tests on other similar products have necessitated changes to product packaging in the past. HGS is at liberty to recommend product changes, replace damaged items for the client’s customers where warranted, and send the customer complimentary products based on inconvenience caused.

HGS is supporting Danone U.K., a provider of early life nutrition, water, and fresh dairy products, with customer care by providing nutrition and health information to new parents. The care is provided through voice, email, and webchat, with plans to provide video chat support within a year. HGS supports this client through a 30-strong agent team which includes five qualified midwives and nutritionists. It also has a group of agents with experience caring for children, handling complaints, and providing out-of-hours support for the early life nutrition line.

In the healthcare sector, HGS is supporting a healthcare provider, Virgin Health, that offers parents the ability to have their babies’ stem cells collected at birth and stored, preserving them for research and potential treatment of serious illnesses. HGS is involved in the entire process, from initial inquiry to stem cell collection to the final checks which take place six months after the birth of the child. HGS coordinates the work of medical professionals, arranges the distribution of the collection kits to hospitals, and organizes the delivery of collected samples to the storage unit. This program has multi-lingual capabilities as it supports customers in the U.K and the Middle East.

The HGS Chiswick center is a good example of a vendor effectively leveraging the language diversity and high education standards of a location to offer strong multi-language, multi-country, and multi-channel support, and to develop bespoke support programs that add value to the customer relationship.

]]>A year ago Convergys acquired fellow contact center vendor Stream, making it the second largest CMS BPS provider by revenue behind Teleperformance. NelsonHall CMS analysts Vicki Jenkins and Mike Cook caught up with key members of Convergys’ leadership team on the anniversary of the acquisition to discuss how the new organization is shaping up.

The importance of cultural alignment

Convergys learned about the importance of cultural alignment through its $335m acquisition of Intervoice in 2008 to strengthen its IVR capabilities. Convergys was a conservative, Cincinnati, OH-based company focused primarily on BPO, while Intervoice was a technology company based in Richardson, Texas and a far less conservative company. Convergys put those cultural lessons into practice with its $820m Stream acquisition in March 2014. Stream was a far better cultural fit for Convergys, being focused on BPO and also based in the Midwest, in Eagan, Minnesota. From a capacity and client perspective, Convergys had little overlap with Stream.

While Convergys has not lost any clients due to the acquisition, there was understandably a degree of hesitancy from some clients due to service continuity concerns. One such client was a high-tech firm that was previously with Stream. The client was initially planning on reducing headcount at the time of the acquisition, but following the implementation of analytic enhancements leveraged from Convergys, the client has since increased capacity and is now set to have Convergys as the sole vendor of a new strategic offering.

Convergys traditionally had a robust analytics offering with ~400 consultants, and these services are now being rolled out to previous Stream clients. Examples of analytic services include VOC and customer journey mapping.

Another factor that calmed the concerns of previous Stream clients following the acquisition was the joint company’s more stable balance sheet, a concern that had stunted expansions with existing clients.

Impact of the acquisition: clients, delivery and growth

The Stream acquisition has created a broader global client and delivery footprint for Convergys, bringing opportunities for clients. An example has been a U.S. telecommunications client which has now begun using nearshore delivery from the Convergys (formerly Stream) location in the Dominican Republic. Convergys sees the opportunity to more than triple the work it is providing for this client.

However, while Convergys is benefitting from a larger nearshore footprint in Central America, it is also facing some problems in the region; for example, the technological infrastructure of Honduras is not to the same standard as Costa Rica and the U.S. Convergys currently has two clients in need of telecommunications infrastructure updates in Honduras, and is in the final steps of solving these issues.

As a result of the Stream acquisition, Convergys has seen growth in EMEA and LATAM. Prior to the acquisition, Convergys had 1% of its headcount in EMEA, and this has now increased to 10%. Convergys was able to speed up its plans for LATAM expansion, with headcount in the region increasing from 3% to 7% post-acquisition. Convergys had a small presence in the U.K., but shortly after the acquisition it opened a new center in Derry/Londonderry, Northern Ireland and the Stream operations team was instrumental in launching the new site.

The two companies have been able to leverage strengths to retain clients and secure new business. An EMEA-based telecommunications client was concerned about Stream’s financial position as it progressed towards a new deal, but the improved financial stability brought about by Stream being acquired by Convergys helped to secure the deal. In addition, an online financial services and an e-commerce retail client, both legacy Convergys clients, expanded in EMEA with the assistance of Stream. And a new EMEA-based telecommunications client is in the process of launching with Convergys to provide customer care support.

Convergys has grown with 16 of its top 20 clients during this past year. It has specifically grown with two U.S.-based high technology clients, and it plans to leverage this growth to obtain new business.

Still work to do, but the signs are good

So, does Convergys have further work to do? Of course. They have plans for the second year focused on system integration, market positioning and branding, particularly in EMEA. The combined organization had numerous payroll systems prior to the acquisition. During 2014, it has been working to integrate systems and plans to complete this integration in Q4 2015.

Convergys sees EMEA as an opportunity for growth and aims to become the largest CMS vendor in EMEA. While it looks for additional capacity in EMEA, M&A is possible. External marketing and branding is a focus for Convergys in the region, and it is starting to gain some traction. A U.S.-based media client that came from the Stream portfolio has conducted a pilot and launch in the U.K. by utilizing the Convergys analytics offerings.

Convergys aims to grow all of its sectors in EMEA, with a particular focus on financial services. It is also looking to further grow its high technology sector business, even though it has already doubled as a result of the Stream acquisition.

And finally, how has Convergys performed financially in the year since the Stream acquisition?

Revenues for the year were up 40%, although organic growth was negative 1%, indicating that Convergys has seen contractions and/or client losses from its own legacy portfolio. However, from a profitability stand point, the company has performed well, with adjusted EBITDA margin up 30 bps during the period to 12.5%.

All of which points to a successful first year for the combined organization, and though some integration work remains to be done, the signs are good for 2015 and beyond.

]]>Q4 2014

- Revenues were $64.2m, up 1.2% y/y

- LBIT was $1.5m, a negative margin of 2.4%, down 98 bps y/y.

Full year 2014:

- Revenues were $250.1m, up 8.1%

- LBIT was $4.9m, a negative margin of 2%, up 72 bps.

Q4 revenue contribution from largest clients was:

- T-Mobile: 30.6%

- AT&T: 19.6%

- Comcast 15.7%.

During 2014, STARTEK:

- Added 17 new clients and $48.6m of annual contract value

- Signed two new clients with annual contract value of $5.5m

- Invested $17.4m in opening four new contact centers: two in the U.S., one in Honduras and one in the Philippines, with a total of 2.9k seats. It also closed two under-performing sites, in Jonesboro, AK and Heredia, Costa Rica. In total, it added 2k seats on a net basis in 2014

- Incurred revenue headwinds in relation to the closure of its Costa Rica contact center, had delayed ramps due to its IP platform migration, and saw softer than anticipated volume from a few large clients.

It plans in 2015 to invest ~$20m in adding ~2.5k seats for future growth.

---------------------

Revenue growth has slowed right down (2013 saw 15% y/y revenue growth in Q4 and the full year 16.7%). But at least margins are improving. Closing the sites in Jonesboro and Heredia should lead to further margin improvement in 2015.

Nearly 66% of its Q4 revenues came from just three clients, all in the telecoms, cable, and satellite industry. STARTEK is focused on sector diversification:

- The immediate priority is the healthcare sector, following its 2013 acquisition of Registered Nurses on Call (RNOC) and its launch of its healthcare division. In 2014, it invested $400k in building out its STARTEK Health offering. Healthcare is a growing market and an attractive sector to CMS vendors

- STARTEK is also for momentum in 2015 to come from its receivables management and back office services businesses.

]]>

Growth in GDP is, to a large extent, driven by increasing private consumption, which alone will look to outstrip real GDP growth in 2015. Growth in private consumption indicates the need for increased customer facing capability of organizations, hence potentially a rise in the need for outsourced CMS.

There has been over the last 14 months a flurry of acquisitive activity highlighting the potential both vendors and PE firms are seeing in this market. Examples include:

- Xerox’s acquisition of Invoco in December 2013 (1,800 FTEs, 10 centers)

- arvato’s acquisition of Walter Service’s German operations in April 2014 (1,100 FTEs, 5 centers)

- Livia Group’s acquisition of SNT Deutschland

- Capita's focus on the region. The firm has made two contact center acquisitions in Germany over the last eight months:

- In July last year tricontes, a Munich based telemargeting vendor with a retail, telecoms, utilities and insurance focus

- Last month, customer management consultancy Scholand and Beiling

- And this month, avocis for £210m. avocis has ~5,000 seats in Germany, where it is one of the largest CMS vendors, accounts for 53% of total revenue, and Switzerland, which is where its foundations lie, and where it claims to be market leader in . avocis was created as an umbrella brand in 2011 from the amalgamation of six companies. It services clients in the telecoms/IT, utilities, financial services, and healthcare sectors

- In its first acquisition since Andy Parker started as CEO, Capita is paying 1x 2014 revenue for avocis, which is a growing business: 2014 revenues were up 21%, and its EBITDA margin was 14.2%, up from 11.4% in 2013. Capita expects avocis to achieve its target for a post-tax ROC of 15% within two years. Significant in being Capita’s largest acquisition to date, avocis is s one of the largest CMS BPO vendors in Germany, It is a capacity move in the region: avocis' vertical focus aligns with that of tricontes. Together with tricontes, Capita will have a significant presence in the German commercial sector CMS BPO market. That is a phrase that one (German, commercial sector CMS) would not have expected to say of Capita even four years ago! This move into Germany for CMS BPO has been an extremely interesting strategic decision by Capita, who outside its specialist activities in financial services and insurance, is known as a U.K. public sector specialist.

With a large addressable market that is showing increased interest in outsourcing, positive consumer consumption, a stable economic & political environment and the above mentioned buy-ins from vendors and PE firms. The region has historically been services by small to mid-sized vendors. With companies such as Capita now building scale, the vendor landscape is now changing, Expect to see some large CMS BPO deals in the region over the next few years, led by the telecoms, banking and retail sectors.

]]>Honduras, and specifically the city of San Pedro Sula, have battled negative perceptions which stem from statistical data indicating high murder and kidnapping rates as well as a military coup and near civil war in 2009. The Honduran government understands that they still have work to do to reduce crime rates, and believes education and job creation are key components to making this happen.

Honduran President, Juan Orlando Hernandez, studied in New York and is aiming to put the Honduran education system on a par with the U.S. His educational initiatives include a bonus system for teachers meeting the curriculum, and a target student graduation rate of 98%. Currently 80% of the country’s public schools have computers and internet access. In November 2014 the Honduran government signed an agreement supporting a program to train English teachers, in which 116 trainers will train 1,000 teachers. High school students (preferably 9th grade and up), contact center and BPO employees, and mono-lingual high school or college graduates are targets for this program.

The centerpiece of hi-tech business in San Pedro Sula is Altia Business Park, the first class A sustainable technology park in the region, which includes smart city amenities. This was the brainchild of Yusuf Amdani, CEO of real estate and textile company Grupo Karim, whom I met during my visit. His vision to create a smart city in San Pedro Sula began in 2007, starting with $25m of investment. To date, the smart city has created ~19,000 jobs.

Amdani has focused on creating opportunities in contact center services, initially targeting the telecommunications industry due to its maturity in contact center outsourcing.

Grupo Karim operates the services Altia Business Park offers to its tenants, including recruitment, support with all legal processes to start operations, floor plan designs, and construction support. Its tenants’ employees have access to a variety of social facilities and a shopping and lifestyle center in the smart city. From a contact center perspective it has a strong foundation, with current tenants including several large U.S. based organizations such as Alorica, Convergys, and StarTek.

Altia Business Park currently has three office towers, is planning to build a fourth tower for completion by the end of 2015, and then a further two towers thereafter. Altia also plans to replicate the smart city in Tegucigalpa, the capital of Honduras, in 2015. Nicaragua and El Salvador are also being considered by Altia for smart cities.

UNITEC University is located in the smart city and is affiliated with Laureate, an international private network of universities. It offers graduate, undergraduate, and vocational programs. At the end of January 2015 it plans to launch a vocational program to prepare students to work in the contact center industry, focusing on English, IT, empathy, and soft skills. It will take students a year to 18 months to complete the program and it has a goal to enroll 500 students. A scholarship program is in place for students from public schools.

According to the Asociacion de Maquiladores and the Altia Business Park, in the region of forty U.S. companies are conducting business in San Pedro Sula, including Texaco, Holiday Inn, McDonald’s, Hilton, Tommy Hilfiger, Office Depot, NCR Corporation, Marriott, Fruit of the Loom, Lear Corporation, Burger King, and Citi Bank.

The following outsourcing vendors are operating in San Pedro Sula (with estimated headcounts): Allied Global (~2,000), StarTek (~1,000), Collective Solutions (~1,000), Convergys (~600), KM2 Solutions (~350), Myron (~150), Alorica (~120), Zero Variance (~100), Levanter Global (~85), and Serve 5 (~50).

Alorica opened its contact center in San Pedro Sula in May of 2014. It has the capacity for 630 seats at the site. It currently has ~120 filled and looks to bring the site close to capacity in 2015. It is primarily targeting clients in the telecommunications, cable, satellite and hi-tech industry sectors.

Companies that have already made the decision to outsource contact center delivery to Honduras include Kyocera, Time Warner Cable, Sirius XM, Straight Talk Wireless, Tracfone, Blue Fusion, Greyhound, AT&T/AIO-Cricket Wireless.

In summary, Honduras (and specifically San Pedro Sula) is making strides to become a viable location for contact center services. Specifically:

- It is currently a viable delivery location for Spanish-speaking services

- With its focus on accelerating English-speaking capability, it promises to become a more viable location for English language contact center services in the near future

- Security and crime remain areas for improvement in Honduras, but the government’s focus on education and job creation, particularly in the hi-tech services industry, with some early successes, suggest that the country will emerge as an attractive nearshore service delivery location.

- Webhelp setting up centers in Cape Town and Johannesburg with an agent headcount approaching 1,000

- Capita transitioning part of its O2 support to Cape Town in the form of a ~1,400 seat operation.

One (of many) attributes that make South Africa such an attractive destination to CMS BPO vendors (and to organizations looking to setup captives) is the tax grants offered. Recent announcements by the South African DTI have indicated that in order to qualify for future tax grants foreign BPO providers would need to have a level four BEE status, the qualification of which is soon to become more stringent. Serco South Africa is ideally positioned to take advantage of this, given its 100% South African management team and partial black ownership. Serco is in a fortunate position in that it can comply with the new BEE Level 4 requirements which kick off soon, although they are due to be reviewed again at the end of next year.

Serco initially opened a 500 seat center in Cape Town in March 2013, as part of a move to transition some of the CMS support for U.K retail client Shop Direct from onshore to offshore locations in India and South Africa. Serco has built up a thriving center in Cape Town, and currently has ~700 FTEs deployed on the Shop Direct contract.

When Serco originally entered South Africa its sole aim was to provide offshore support to U.K. and potentially Australian clients; this strategy has since undergone a rethink with the upheaval of its U.K. reputation following the e-tagging scandal in 2013 which, although happening in a different part of the Serco Group impacted the ability of its private sector BPO business to win new deals. Serco is now also actively courting domestic South African clients in the telecoms, media, BFSI and retail verticals. It is currently running a customer care webchat pilot for a domestic telco and is also in talks with a local retailer to provide in-store e-commerce support. If all goes to plan Serco should have ~700 FTEs providing domestic support in its Cape Town operation by end of Q2 2015.

Serco’s agent acquisition program in Cape Town has a very personal flavor with the country MD Fagri Semaar, conducting radio appearances as well as University and school presentations in order to acquire talent. Currently the company has 64k applicants on its database. 45% of applicants are inexperienced in contact center delivery, though the vast majority are from a previous customer service background. Serco has moved away from a purely skills-based hiring approach in its Cape Town operations with applicants initially completing a psychometric evaluation that is weighted towards the vertical, service line and end user position the applicant is applying for. Currently Serco is hiring one in five applicants in its Cape Town operation.

Now with Serco’s recently announced strategy review, what does this mean for its South African operation? As part of Serco’s private sector business, it will be one of the units to be sold off. Whilst this will result in uncertainty in the near term, the dropping of the Serco brand should help the U.K. private sector business in its go-to-market efforts which potentially means increased work for South Africa.

]]>Sitel wants to be known for creating great experiences, and its focus now is ‘people first’. It recently hired a new chief HR officer, Elsa Zambrano, who has created a new executive position to focus on global talent management efforts. Brandyn Payne, in the role as VP of global talent management, is focused on talent development and measures for attrition and absenteeism. In addition, Sitel has created a new index with contacts at Vanderbilt and outside consultants. Sitel stated that it is ‘in the third inning of a nine inning game’ with this investment.

Sitel explained how it is leveraging technology to assist its agents in supporting clients. In an effort to improve agent coaching, Sitel is rolling out a proprietary platform, 20/20, so coaches will be able to provide ongoing documented feedback to agents and learn from tracking common issues. Sitel also highlighted its Intelligent Desktop, a cloud-based CEM platform that provides agents with a full view of all customer interactions across all contact channels.

Improving employee communication is another focus area for Sitel, and CEO Bert Quintana is acting on his commitment to connect with Sitel’s employees by recording a five-minute video segment for employees each Friday, wherever he happens to be in the world (including, to date, from Colombia, Germany, the Philippines, the U.K. and the U.S.). He has also introduced his leadership team, clients, agents, and industry analysts to Sitel employees: my colleague Mike Coo, and I had the pleasure of participating in one of these segments.

Listening to its clients is another Sitel commitment. It illustrated this by providing more in-depth interactions with industry analysts at the meeting this year than in the past. The clients benefitted by posing questions to a panel of analysts, with topics ranging from site selection to use of work at home agents (WAHA), to vertical market questions and many more. The clients also participated in round table discussions with analysts on topics including site location selection, multi-channel, flexible labor force, metrics, analytics, agent retention, and web based engagement. Sitel even took that tough yet courageous step of asking clients to discuss with analysts what Sitel could do better; the feedback was shared with Sitel. This is a bold move, and it now has the opportunity to turn that feedback into positive change.