In 2020, the U.S. healthcare payer BPS market saw accelerated growth in the adoption and design of digital solutions across all functional areas. The acceleration is driven mainly by consumer demand for an "Amazon" experience from their health plans and providers, to know the cost of care for associated benefit plans to assist in plan selection or inform decisions about elective procedures and treatments. It is also driven by approaching federal regulation deadlines. Specifically, regulatory requirements from the Cares Act and subsequent rulings from CMS are driving further steps towards interoperability throughout 2021-2024. These requirements follow the initiatives by CMS offering price lookup tools for outpatient procedures and OOP costs for physician visits for Medicare consumers.

Regulatory deadlines drive digital adoption

By January 1, 2022, private payers and group plans must standardize data files to be made publicly available and shared through APIs. The available data will be an opportunity for insurtechs and technology vendors to develop price comparison tools further and price analyses to inform their development.

After January 1, 2023, these payers must offer online plan comparison tools for consumers to view negotiated provider rates and personalized OOP costs estimations for 500 commonly utilized services. This will require real-time underwriting and price aggregation and analysis, with the ability to segment the data by facility and provider. Then, starting on January 1, 2024, individual and group plan consumers will be able to view the estimation of the total OOP costs, including usual tests, procedures, DME, and other items associated with specific treatment plans.

Opportunities for tech vendors to provide services & digital solutions

Without significant digital transformation, meeting the interoperability and price transparency requirements poses a considerable challenge for U.S. healthcare payers. Legacy and "home-grown" systems perpetuate siloed digital solutions, unstandardized data, and difficulties in designing APIs and intake of external data. The disjointed process becomes even more complicated when payers face these challenges on a seasonal basis to perform market assessments, develop products, and price new and renewed plans.

Additionally, payers face the challenge of complying with continual changes in required API formats, currently defined by HL7's FHIR. Payers will need support in converting or implementing the standard format and subsequent testing as regulations and required formats change, such as federal exchange marketplace plans that must implement FHIR APIs with third-party apps for open data access.

Capgemini spotlight: price transparency offerings

U.S. healthcare payers can obtain digital solutions to support regulatory compliance with Capgemini's price transparency solutions. Capgemini has 15 years of experience in the Medicare Advantage space, providing enrollment and member account maintenance management services, solutions, and advisory support. The recent focus has been on designing analytic and AI-driven tools for healthcare payer and provider clients in meeting regulatory guidelines and customer-driven demands for enhanced digital experiences and upfront cost estimations.

Capgemini offers service-line driven pricing for the average cost of medical care from hospitals and healthcare providers in the consumer's area. Capgemini developed the relative pricing guidance for hospitals, with an average of 1200 parameters per hospital for ~700 hospitals, categorizing both operational and overall spend by diagnosis parameters. The hospitals were then ranked into low, medium, high. In addition to overall price analysis, Capgemini parsed hospital spend by service line to provide cost estimations by diagnosis or treatment.

Capgemini is also working with several Blues to estimate OOP cost projections viewable on the member portal. Capgemini designed a cost calculator for a medical procedure at a specific healthcare facility, including the member's expected copay/deductible. A pricing engine was then implemented into a Blue's member portal to provide hyper-personalization, utilizing both internally available eligibility data and the aggregated market data for variable cost pricing. Currently, Capgemini offers implementations of ranking engines enabled by pricing algorithms and provider registries, returning search results of the top 10 providers most relevant for a specific diagnosis or procedure and the estimated cost of copay/deductible/OOP for each provider.

Capgemini's price transparency work is also heavily focused on utilizing MLR for cost-sharing estimations, including telehealth in the cost estimations. For a U.K. health plan, Capgemini implemented a solution to perform plan comparisons against industry standards, such as a specific member with a particular set of demographics and health characteristics, to estimate the eligibility and cost-sharing – competitive pricing. The solution incorporated several analytics tools to perform analysis and reporting on historical cost-sharing.

By the end of 2021, Capgemini's digital solutions in price transparency will integrate the payers' provider search tools to rank relevant providers based on health outcome metrics. Capgemini continues working with certain Blues plans to develop a marketplace with shared data and real-time quoting for care pricing and plan comparisons, involving interoperability and price transparency initiatives to benchmark the cost of services by area and plan. Additionally, Capgemini's development is focused on creating bundled pricing for all procedures and tests associated with a long-term treatment plan, as will be required of healthcare payers by 2024.

Increased demand and opportunities for digital transformation in the near future

The challenges faced by U.S. healthcare private and group payers present opportunities for technology vendors to provide digital solutions and services for payers to meet both the regulatory requirements and consumers' digital experience expectations. Client engagement types will vary by payer size, as many large payers only require specific solution design and implementation within their existing systems, while many mid-market and regional plans will be looking for BPaaS models of engagement with technology vendors. Payers will be looking for digital solutions to provide personalized real-time quotes for procedures and later for bundled pricing by the treatment plan and expanded data sharing to enable price transparency initiatives.

]]>

Digital front doors and transparency a new normal for healthcare?

U.S. healthcare is no stranger to an environment of continuous change and has not been spared the effects of the COVID-19 global pandemic in 2020. The unique circumstances born from the need for social distancing during the pandemic have accelerated healthcare consumers' demands for digital transformation. The ask comes from all healthcare continuum vantage points – patients, providers, payers, and vendors. Healthcare must change its practices to allow for more seamless digital interactions to meet these demands.

As with other service industry sectors, healthcare consumers want the option to access their health services virtually – evidenced by an increase from an 11% utilization of virtual visits in 2019 to over 45% in 2020. Some larger health systems have made this transition without significant challenges, expanding telehealth contracts, and receiving service reimbursements for both commercial and federally funded insurance types. However, many providers were faced with the decision to either suspend their practice or invest in digital platforms or services to offer virtual visits. Cognizant's Core Admin Solutions support providers' internal processes to offer telehealth and payers and providers in efficiently & quickly submitting process associated claims and authorizations via Trizetto's Touchless Authorization Processing (TTAP). The demand for telehealth has become an independent demand from the initial catalyst of social isolation and continues to be at the forefront of patient expectations. Even the senior population is thought to have few barriers to accessing virtual care, with 84% of sampled senior consumers stating they do not have any technical challenges in attending a virtual appointment with their doctor. With the remote operation of the doctor's visit comes the corresponding demand for total digital transformation; payment processing, e-prescription writing, prescription home delivery, and remote patient monitoring. Multi-faceted companies, like Cognizant, offer a variety of bundled or unbundled services and platforms to help healthcare providers and payers address the increased demands for digital interactions. This new digitization is also thought to reduce costs by increasing care coordination, administration, and manufacturing efficiency.

Providers and Payers are finding that digital products also offer the opportunity to clinically manage their patients and members remotely, with IoT, remote monitoring devices, and health wearables. The consumer can utilize various devices, measuring vitals, health coaching through AI, and tracking other metrics related to health risk factors. 65% of consumers utilize some type of wearable. With this percentage of adoption and available data, providers and payers have an exciting opportunity to address their patients' and members' health outside of the doctor's office. Vendors offer bundled platforms or paired digital services to collect, aggregate, and analyze the patient/member data to facilitate care management efforts by both their clinicians and their health plans. Though this digitization also requires a financial investment from the organizations, the vendors promise a visible ROI in cost savings and improved health outcomes.

Driving the transformation

Regulatory bodies have been pushing healthcare providers and payers towards a digital transformation, most recently with the ONC Cure's Act Final Rule. The rule was created to increase interoperability and access to consumer's own health information. Though the rule pushes providers and payers towards the shared goal of an enhanced patient experience, compliance with these requirements will come at a cost. By 2021 payers will be required to allow consumers access to all their claims and health information and to develop APIs to share data with other organizations and regulatory bodies. Though the compliance will be a financial investment for providers and payers, vendors such as Cognizant can implement or offer platforms to achieve such price transparency.

The Centers for Medicare and Medicaid Services (CMS) has similarly taken steps to guide providers and payers towards a better patient experience. In the 2021 Medicare Advantage Final Rule, CMS announced a change to its CMS Star Ratings measures, increasing the weight of the patient experience metrics. Payers must now invest more heavily in their consumer requirements – digital transformation to achieve an end-user-friendly suite of digital platforms. Cognizant addresses another of these drivers by offering several applications and platforms that facilitate both back-end processes and consumer-facing platforms in assisting payers in meeting heightened digital demands from their consumers. Cognizant's continued investment in Trizetto products offers payers such an opportunity for an enhanced user experience with an automated enrollment platform. Such an offering would make a payer more attractive in the upcoming Medicare Advantage and ACA Marketplace OEP (open enrollment period).

Healthcare organizations are also feeling the pressure for change from InsurTech companies and their partnerships with healthcare providers. These initiatives are attracting members and patients with their omni-channel user interfaces and strategic focus on digital platforms and processes.

Product Suites to Achieve the New Normal

Amongst Cognizant's comprehensive suite of product offerings, their digital healthcare platforms and services support over 200 million lives in the U.S. Payers and providers alike have the option to select a la carte products or bundled services to meet the changing regulatory requirements and evolving demands of their consumer and patient bases. Cognizant continues to exact leadership and be forward-thinking in its current and planned digital transformation offerings and continued investment in Trizetto Healthcare Products ($100m):

- Core Payer and TPA admin solutions, for claims processing and management

- Payer-provider solutions, for facilitating contract pricing and modeling and payment administration. Cognizant has planned offerings for onboarding and credentialing

- Government and Quality Solutions, for enrollment and encounter data management, and support of quality rating measures and reporting. Cognizant is planning offerings for enhanced care coordination

- Care Solutions, for clinical and utilization management and value-based benefits. Cognizant is planning offerings for for automated authorization and referral management

- Data orchestration SoE solutions for data aggregation and engagement. Planned offerings include additional integration and analytics for interoperability.

While Cognizant, and other vendors, offer a wealth of products and platforms for health systems and payers, for many the financial investment required has been a barrier. But COVID-19 is having an impact, in spite of an estimated four-month loss of $202.6bn for hospitals and health systems in the U.S. Every U.S. health system recently interviewed by NelsonHall regarded digital transformation as more important as a result of COVID-19, with increased investments planned in SaaS and cloud infrastructure. Overall, hospitals & health systems in the U.S. have shortened their planning horizons to address short-term priorities and investments. One major healthcare system stated that their planning horizon was now weeks rather than years. The same reduction in planning horizon is also evident in healthcare payers, but here with a need for customer retention combined with a much stronger emphasis on cost control.

As is true in other sectors, the pandemic will likely increase the acceleration of digital transformation initiatives across healthcare, with a clear focus on achieving short-term results (rather than in years), producing very immediate improvements in both productivity and customer experience.

]]>

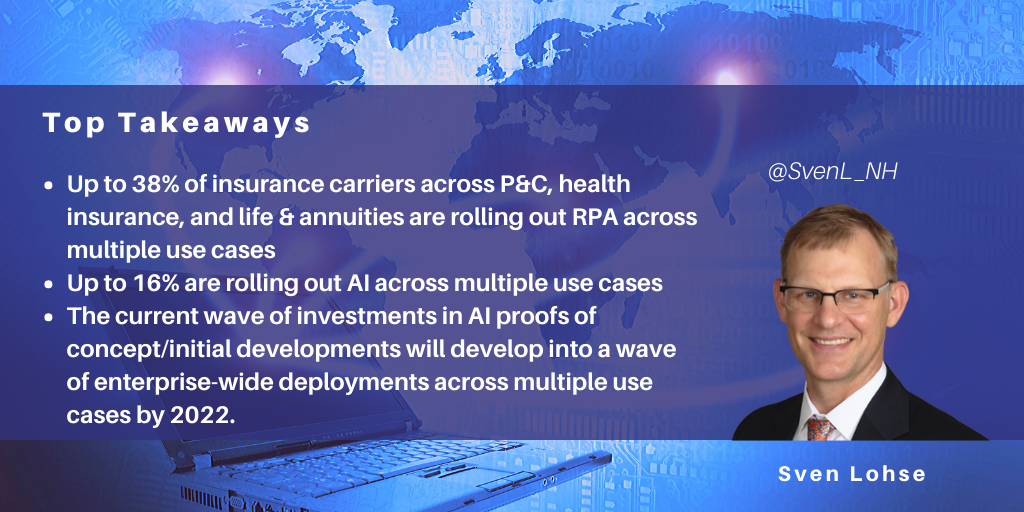

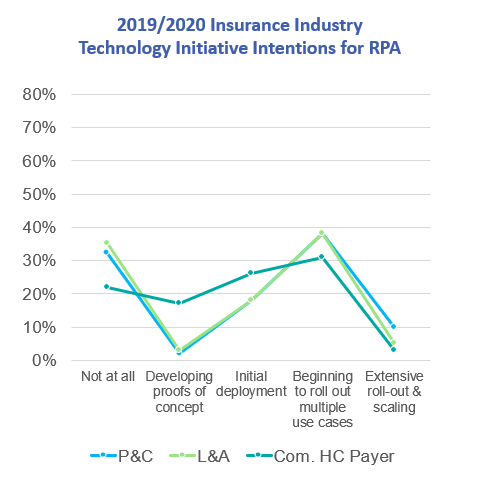

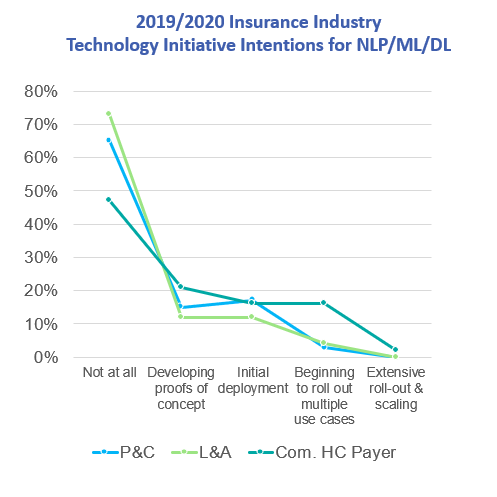

NelsonHall predicts that by 2022, 35% of insurance industry carriers will be in the process of adopting AI technology across multiple use cases within the enterprise. This is based on NelsonHall survey data from the insurance industry that tracks adoption of both RPA and AI (NLP/ML/DL) technology across the property & casualty, health insurance, and life & annuities insurance sectors.

Survey findings

Between 31% and 38% of surveyed carriers are beginning to roll out RPA across multiple use cases, while between 3% and 16% are beginning to roll out AI across multiple use cases – this range includes P&C (3%), L&A (4%) and healthcare payers (16%).

We expect a similar rate of maturity development for AI as for RPA. For RPA, we have seen a wave of investments in proofs of concepts/initial deployments in 2016/2017 develop into enterprise-wide initiatives in 2019/2020. We expect to see the current wave of investments in AI proofs of concepts/initial developments to develop into a wave of enterprise-wide deployments across multiple use cases by 2022. As was the case with RPA, we see a wide variety in the rates of adoption for different types of AI (in particular for natural language processing, machine learning, and deep learning).

The business functions that lead in adoption of AI include:

- P&C insurance: policy origination, underwriting automation, and capacity to manage changes in volume of customer interaction in real-time

- Life & Annuities: policy pricing optimization, contact center real-time customer support, investment support

- Health insurance: product pricing optimization, marketing decision-making.

AI adoption will likely reflect the following broad trends:

- U.S., U.K., and Asia/Pacific carriers will in general lead their counterparts in Continental Europe in the implementation of AI

- Some business functions will provide more fertile ground for adoption of AI, e.g. personal lines insurance policy origination, and customer service will continue to adopt AI more quickly

- Continental carriers will emphasize the importance of customer service and increased speed/ease of new business acquisition in comparison to straight through processing, which is more frequently the top priority for U.K., U.S., and Asian carriers.

General guidance for carriers in adoption of AI

Enterprise governance

Effective enterprise-wide rollouts and scaling of new AI technologies will require strong enterprise governance structures. Efforts completed on behalf of similar enterprise deployments of RPA will pave the way for AI adoption. See the following NelsonHall blog for an example from the health insurance industry: How NTT DATA Established Enterprise Automation Governance for BCBS Health Insurance Carrier

Adapt roles and skills within personnel pyramids

Adoption rates and effectiveness of implementation of AI technologies will ultimately depend on the organizational structures and quality of the people used to transform carrier operations. Carriers will therefore be required to redefine organizational structures, roles and skills. (This will be true whether AI adoption is conducted with or without the extensive use of external consulting and/or outsourcing partners.) Expect significant lag time between the articulation of new organizational structures, roles, and skills, and the period in which enterprises can acquire talent. As with most new technologies, AI experts will be hard to identify, attract and retain, whether compensated directly by a carrier or not.

Align with existing procurement strategies

Procurement strategies that manage external AI partner vendors need to be clear, manageable, and adapted to enterprise procurement structures in place. It’s noteworthy that while outcomes-based, or gain-sharing, contracts get a lot of attention, about 90% of P&C transformational outsourcing contracts in the U.S. are still managed on an FTE, fixed-price, or transaction basis. In Asia Pacific, that proportion is even higher. So, especially for early-stage AI projects, insurance carriers should likely consider keeping outsourcing contracts as straightforward as possible.

Get early buy-in

Winning the race to effective, enterprise-wide adoption of a new technology frequently depends on how innovators introduce that technology within the context of the enterprise. Far-sighted planning may include pilot projects that start small, and then earn organizational buy-in based on clearly demonstrable, early wins. Employee upskilling programs can help allay the fears of those concerned with being displaced by new technologies.

]]>

A magnitude-6.4 earthquake struck Puerto Rico on January 6, killing one person, toppling homes and buildings, and triggering a blackout on the island that is still recovering two years after Hurricane Maria. Governor Wanda Vázquez declared a state of emergency and activated the Puerto Rico National Guard to help with recovery efforts.

How might this earthquake disaster have affected delivery of outsourcing services from Puerto Rico (P.R.) to U.S. clients? Infosys’ response to the devastation caused by Hurricane Maria sheds light on whether the buyers of nearshore outsourcing services should expect significant interruptions to service as a result of such natural disasters.

Infosys’ Puerto Rico delivery center

In 2013, understanding Puerto Rico’s risk exposure to natural disasters, Infosys set up a delivery center in Aguadilla, P.R., as part of a deal to optimize global operations for a client Fortune 500 consumer, engineering and aerospace technology company. Advantages from Infosys’ point of view included:

- Local knowledge: prior understanding of the local Aguadilla business environment through its work with the client

- Rafael Hernández International Airport: located near the delivery center, the transportation hub supports a local aerospace industry that sustains a reservoir of local IT and knowledge services skills

- Skilled local outsourcing professionals: P.R. residents enjoy the full rights and legal protection of U.S. citizenship (P.R. is an unincorporated territory of the United States); they tend to be multi-lingual in both English and Spanish, and tend to be inexpensive compared to counterparts in the mainland U.S.

- Tax relief provided under P.R.’s Economic Development Incentives Act: “the cost structure was a little more amenable in comparison to some of the other locations in the U.S.,” said Aniket Maindarkar, head of Infosys’ Americas operations at Infosys BPO, in 2014. The Puerto Rico Industrial Development Company (PRIDCO) offered a 100% exemption on taxes on earnings and profits, and a 90% deduction on local property taxes. PRIDCO’s executive director Medina explained at the time that “although [P.R. is] part of the U.S., we can negotiate tax rates with companies and they do not pay federal tax rates”

- Staff training and other aid: PRIDCO helped train staff and aided Infosys in finding a new facility location

- High profile political support: Infosys’ investment in a P.R. outsourcing delivery center garnered press exposure through the P.R. Governor’s visit at the opening of the new Infosys facilities in Aguadilla.

Disaster resiliency features

At the time Infosys initially established nearshore outsourcing capabilities in P.R., the company publicly announced it envisioned serving U.S. clients in multiple restricted industries, including defense and healthcare. Within a year Infosys had relocated both retained and new personnel into a nearby 12,000 sq. ft. facility that could accommodate up to 300 people. The relocation retained features that would later prove advantageous to disaster resiliency, including:

- Aguadilla’s location on the northwestern side of P.R. helps protect facilities from strong winds and hurricanes that tend to land on the eastern and southern sides of the island

- The local Rafael Hernández International Airport is supported by the infrastructure of a former U.S. Air Force base and is located less than ten kilometers from Infosys’ Aguadilla facility

- The airport offers direct commercial flights from multiple airlines to the U.S. mainland, including the greater New York City area. This is the location of a major Infosys healthcare outsourcing services client served by its Aguadilla personnel

- Backup electrical power, supplied by diesel-powered generators located at the Infosys facility.

Expanding capabilities to the healthcare sector

Since 2016, Infosys has expanded the capabilities of the delivery center from aerospace industry functions to operations in the communications and healthcare industries. For U.S. healthcare clients Infosys began to build out clinical and IT service desk and support for Medicaid business. Initially, Infosys hired half a dozen P.R. clinical nurses with both bedside and corporate/investigative expertise.

The U.S. legal status and U.S. citizenship of the P.R. personnel supports delivery of restricted defense industry and healthcare industry services (e.g. Medicaid program services) with lower local costs than those of U.S. counterparts. According to U.S. Bureau of Labor statistics, median wages for registered nurses in the U.S. are approximately double those of their counterparts in P.R. However, among the nurses with both bedside and corporate/investigative experience that Infosys recruits in P.R., Infosys’ experience is that the discount for clinical nurse labor rates is narrower: 15-20% discount for a nurse in P.R. compared to New Jersey, and 10% discount for other highly skilled resources.

Lessons from Hurricane Maria

When the Category 5 hurricane hit Puerto Rico in September 2017, it lingered over the island for over two weeks, causing over $90bn in damage and approximately 3,000 fatalities. Nevertheless, despite the scale of the devastation, Infosys reports that its service to clients was interrupted only for one day while it implemented its disaster recovery processes. Diesel generators supplied power to employees for the duration, and most employees resided in the facility rather than go home when off duty. Infosys also retained transportation links with its clients. Despite the atrocious weather, Infosys secured approval to fly by private jet into Aguadilla’s airport on an emergency basis and flew some of its P.R. personnel to client locations in the mainland U.S. Infosys also used these flights to transport vital physical supplies and even cash for salary payments to its Aguadilla personnel.

Through the Maria event, Infosys learned that its communications links required further improvement. Deployment of satellite links into Infosys’ global IT network now enable resilient communications and internet connectivity independently of local fiberoptic and telecommunications infrastructure.

Infosys’ responses to the Maria event have reassured healthcare clients that its facilities in Aguadilla are adaptive and resilient in the face of major natural disasters. Since 2017, Infosys’ outsourcing services from Aguadilla to mainland U.S. clients have expanded, and in the last year Infosys reports that it has expanded clinical healthcare outsourcing services to a second U.S. health insurance company. Infosys now employs approximately three dozen nurses at the Aguadilla facility. Infosys is prospecting for more clients, and has developed contingency plans for bringing other Aguadilla facilities online should a major client win exceed current excess capacity of approximately 60 seats.

]]>

Convex Group is a start-up specialty insurer and reinsurer focused on complex risks, launched with $1.8bn of committed capital in April 2019. Convex will underwrite insurance and reinsurance for “complex specialty risks across a diversified range of business lines” in London and Bermuda. The company aims to adopt a conservative investment strategy with a predominantly high-grade fixed income portfolio and duration matched to the profile of the liabilities.

Development of an Insurance-in-a-Box Operating Model

As a start-up, Convex had no legacy infrastructure or operations and was looking for an “out-of-the-box” insurance and reinsurance infrastructure and operations model, priced on a per transaction basis to enable it to achieve a new level of cost ratio performance.

Accordingly, Convex evaluated multiple vendors against three criteria:

- The extent to which each vendor could align on their operating model and provide an “insurance-in-a-box” offering

- The detailed service model and the ability of the vendor to underpin this model with technology

- The ability to mobilize experienced personnel quickly and execute in a short timeframe.

Following this evaluation process, Convex signed a long-term strategic partnership with WNS in April 2019. The key factors that differentiated WNS following discussions and site visits by Convex in Pune, India included:

- Their depth of insurance industry domain expertise and scale of investment in the industry. WNS has extensive experience in working with global specialty insurers and reinsurers and brokers

- Their service excellence and risk management focus

- Their flexibility in adapting to Convex’s requirements at speed.

WNS has subsequently created a onshore/offshore target operating model and has successfully implemented the technology stack in the initial start-up period of 6 months to manage the HR, Finance and Accounting services, and multiple Industry-specific activities including claims processing, and inward (re)insurance underwriting support. Convex will largely deliver product development and underwriting.

The technology being used is Sequel insurance software, already implemented in support of underwriting, with Oracle cloud software implemented in support of HR and accounting.

WNS Free to Offer Solution to Other (Re)Insurers

With this contract eventually aiming to move toward a per transaction pricing basis, WNS is banking on substantially increased revenues from the contract as Convex becomes established and captures market share in the reinsurance sector, with both Convex and WNS perceiving that the resulting lower cost from this new operating model will provide a source of competitive advantage. Indeed, Convex perceives that by using WNS and this operating model, it will be able to target a cost ratio of 10%-11% rather than the 13%-15% typically achieved.

Convex believes that as a first-mover and start-up with no legacy baggage it can derive greater short-term advantage from this solution than its established competitors, though WNS is free to offer the “insurance-in-a-box” solution developed for Convex to other (re)insurers and sees this as a major new market opportunity as insurers look to reimagine their operating models.

]]>

Dozens of influencers recently attended the WNS U.S. Influencer Day in New Orleans, where the theme was 'Co-create to Outperform’. Through general overviews of its approaches and through client presentations, the company provided insight into its recent success and its future plans. The backdrop for the conference was cheery, buoyed by 7% annualized growth over the prior fiscal year.

Here I look at a couple of highlights from the event, focusing on WNS’ healthcare business and at its approach to business transformation generally.

Healthcare domain expertise

HealthHelp, a company WNS acquired in September 2017, has become the central pillar of WNS’ healthcare business. HealthHelp was likely much larger (NelsonHall estimates >$40m in revenue) than the extant WNS healthcare segment business at the time, hence it is likely HealthHelp became the core around which WNS organized the rest of its healthcare business. Potential integration problems seem to have been avoided by granting HealthHelp a long leash; HealthHelp remains branded as “HealthHelp, a WNS Company”. Both the acquired and the acquiring companies appear to be learning from each other. The broader WNS business may be adopting some of HealthHelp’s approaches to supporting services with proprietary software. HealthHelp’s proprietary software platform reportedly supports the stickiness of its services, and WNS is contemplating ways in which it can further support client services in other verticals using similar proprietary software platforms.

Houston, TX-based HealthHelp provides the foundation for healthcare revenue that is now approaching or exceeding 15% of total WNS revenue. The healthcare vertical anticipates double-digit growth in 2019. WNS’ “non-denial” clinical services enable payers to support providers within its network to provide optimal, cost-effective care. WNS facilitates educational, supportive interactions that enhance provider satisfaction rather than a confrontational or abrasive interaction that degrades provider satisfaction. WNS does this by bringing expert staff from its network of clinical specialists at academic medical centers into conversation with its providers in order to resolve cases that have been determined by the payer or by WNS to be inappropriate for any reason, clinical or economic.

The company’s value proposition and strategy appear directionally unchanged, although more may develop in this regard following the recent promotion of Kariena (Zacharski) Greiten to the role of CEO for HealthHelp. Prior to this promotion, Greiten had been Chief Product Officer at Magellan Healthcare.

Transformation approach

The Co-Creation theme of the conference (and of WNS marketing) was expounded by WNS executives such as Adrian McKnight, EVP of Transformation and Quality, who said “We look to be a transformation partner rather than an outsourcing partner.”

WNS believes that perspectives on outsourcing are maturing. Initially, potential clients may consider outsourcing a piece of the value chain. But if they don’t begin with an end-to-end analysis of what the business could deliver to the end user, they begin to ask “What is beyond the KPIs of the outsourcing contract? What are the broader operating and business models required to facilitate the customer journey?” Then companies realize they are looking to buy transformation, not outsourcing. While outsourcing can be an aspect of a solution, it may not be the core requirement.

Domain expertise such as that which WNS offers through HealthHelp creates opportunities for WNS to take a seat at the table in discussions with clients on how to realize digital transformation. An intimate understanding of a healthcare payer’s organization helps immeasurably as WNS assesses the potential for transformation.

The iterations required to plan, build and implement client solutions rely on good collaborative practices, which, in turn, are founded on IT agile methodology. In WNS’ view, IT “agile” has matured to become a more holistic set of practices that integrate the functional needs of the client organization from all areas, not just IT. WNS claims to focus heavily on this broader view of the strategic position of its clients because culture and the speed of agility depend on this contextualized perspective. These eventually drive IT development projects and outsourcing contract requirements.

As WNS works through business problems with clients towards appropriate solutions, the ultimate success of WNS Co-Creation relies on the relevance and meaningfulness of its capabilities. Speed is also of primary significance. Whether those capabilities are supplied internally by the WNS enterprise or via its network of partners, WNS aspires to remove friction and increase the speed at which it can cycle through iterations, particularly in the implementation phase of a Co-Creation experience.

]]>

In this blog, I look at how NTT DATA worked with a large Blue Cross Blue Shield (BCBS) health insurance carrier to establish an enterprise governance structure for automation, and at the lessons learnt along the way.

Like many other large BCBS carriers, the company had piloted RPA initiatives, and from the somewhat frustrating results of these experiments, it had formed two conclusions:

- An IT department-driven center of excellence delivering bots will not achieve the full potential of automation

- Point solutions being driven within individual towers/business units are not scalable across the enterprise.

The company concluded that before it could proceed with its automation journey, it required an automation governance structure that aligned with the enterprise strategy. A business-driven (rather than IT-driven) deployment of RPA needed to coordinate the needs, requirements and deployment of RPA across the front, middle and back office functions, as well as shared and internal ancillary services.

The BCBS carrier hired a team from NTT DATA, led by Deana Rhoades, the Global Practice Lead, Healthcare Automation “to create an enterprise-wide governance structure customized to their corporate strategic objectives and organizational culture”. Within the context of the enterprise’s goals, strategy, and current workforce, the company tasked NTT DATA to create the automation strategy, the decision frameworks and the organizational structure. While the BCBS company had long before established solid objectives, frameworks and management systems for its human workforce, the company realized it needed to lay the foundation for the same kind of structure for automation (and the bots) of its “digital workforce”.

Starting in August of 2018, NTT DATA began its work creating an enterprise level governance structure for automation. It focused on scalability considerations and governance, treating bot development “almost as an afterthought”. The tactical view about how to purchase and deploy automation solutions and build bots on different platforms would flow from the enterprise’s strategic objectives and from appropriate integration of the human and the proposed digital workforces. It took two months for NTT DATA and its client to articulate the following governance model, composed of three layers:

Layer 1: Sponsorship

Champions of the RPA transformation articulated the vision and goals for the automation journey and monitored performance of the COE. Sponsors include high-level representatives of the COO, the CIO and the HR departments, coordinated by a Program Management Office (PMO). Strategic frameworks now articulate the enterprise’s objectives, categorize potential automation projects within that context, and facilitate decisions about deployment in terms of (for example):

- Potential cost savings (prioritized over revenue)

- User experience (prioritized over productivity).

Layer 2: Enterprise Capability Center

This team unites leaders and dedicated resources from the following functions: HR, Data and Analytics, IT, Security, Organizational Change Management, Business Process Management, and Operations. Six workgroups develop and provide expertise on the core COE capabilities. The COE subgroups cascade the automation strategy into action plans that provide capabilities across automation development teams and business units. Focus areas include:

- Strategy and Measurement – turns strategy into executable components; owns success criteria, key performance indicators (KPIs) and objectives and key results (OKRs); quantifies the value of the COE

- Pipeline Management – generates demand for automation at the process level among BCBS company employees, prioritizes and schedules the resulting workstreams

- Workforce Strategy – defines needed FTE skills and gaps, owns the organizational change management (OCM) plans and provides training for BCBS company employees

- Automation Standards – develops the standards, tools, repositories, policies and procedures that guide all automation initiatives

- Data Strategy – maintains data management strategy, defines how automation software accesses and collects data, and how the automation efforts comply with risk and security policies

- Virtual Workforce Monitoring – maintains a centralized command center to monitor and oversee the bots in production.

Layer 3: Automation Factory

Delivery and deployment teams work under the aegis of the leadership priorities and plans developed in layers 1 and 2 with complementary aims:

- Demand generation – generating awareness and demand for automation within the enterprise at the level of the teams that manage specific processes. A change management team trains these teams on capabilities of RPA and helps them see the value of implementing the technology

- Technology delivery – agile development teams automate processes using the appropriate tools and platforms, such as Blue Prism and UI Path.

For the next phase of work, NTT DATA has begun to create a complementary hybrid (or “federated”) operating model for agile delivery of bots. This hybrid model is supposed to establish the guardrails and frameworks needed by individual business units that have the skills and the desire to build their own bots. The hybrid model is expected to augment the centralized enterprise governance model by 2020.

The human response?

With NTT DATA, the BCBS company has worked to communicate with various business units and with their leaders to resolve their questions and any potential anxiety about the use of bots. During the BCBS company’s prior work with another IT consulting firm, it had developed its own home-grown automation tools. The in-house deployment of an RPA platform had introduced the company to concepts and practices at a tactical level. Activities surrounding these pilots had been widely broadcast through various communication channels, including robotic roadshows, Yammer, and email. As a result of this in-house publicity, NTT DATA reported that it met with more curiosity and less resistance than expected. NTT DATA also reported that company business units and employees had already begun to form opinions about automation through the lens of their experience with their prior RPA tool, opinions that needed to be considered if and when other development tools were introduced.

The business consequence?

NTT DATA believes that the BCBS carrier has taken a significant stride up the automation maturity curve by articulating a governance model with the following elements

- Charter

- Roles and responsibilities

- Leaders

- Change management

- Resources dedicated to organizational communication and demand generation

- Resources dedicated to development of a broader set of intelligent automation technologies.

RPA initiatives that predate the NTT DATA-led exercise in defining automation governance now have a structure and resources available when they need to escalate issues, and have realized greater ROI. Furthermore, the BCBS carrier’s “ox in the ditch” initiatives have now been organized into six workstreams, and in future the company believes that its governance structure and measured approach will yield expected ROI and that its human and virtual workforces will complement each other efficiently.

]]>

In my previous blog, I described how, since 2017, Sutherland has created a shared services model that obviates the need for participating California health plans to separately build and update parallel databases to track the availability of providers of nonurgent care for Medicaid recipients.

The company estimates that through its consortium of member health plans it has reduced associated health plan physician data management costs by 75% through elimination of duplicative work and by improvement in survey execution workflow and other areas. For an estimated 80,000 physicians in its CA directory, Sutherland now estimates that it reduces the touch rate on providers related to the Provider Appointment Availability Survey (PAAS) from three to one call per practice. The initiative also improves reporting and other interactions with the California regulatory body (Department of Managed Healthcare, or DMHC) and improves patient access to timely care.

Sutherland’s success with its coopetition/shared services model begs an interesting question: can this model be extended across the U.S. and, if so, how?

Uncovering value from duplicated effort

The coopetition model now proven in California might provide a useful template for future work at the national level. Data from Sutherland’s efforts in California indicate that national health plan provider networks significantly overlap and that much of the work they pursue in building and maintaining their physician databases is therefore duplicative and wasteful. In California, Sutherland reports a 48% overlap of providers between the top three CA health plans. That is, of ~20,000 physicians that are currently contracted to plans managed by one of the top three health plans in CA’s Medi-Cal Medicaid program, over 9,000 are currently contracted with all three health plans. Each health plan in California is required by the DMHC to maintain accurate data on each provider so that patients can gain access to timely care. Each health plan is further required to manage this dataset in order to maintain its own operations. The difficulties in maintaining these parallel datasets result in a myriad of problems for different stakeholders, including wasted effort.

Stakeholders include vendors of business outsourcing services. Prior to Sutherland’s involvement in the shared services initiative, the data collected by the DMHC was of such poor quality that it resulted in a directive to all CA health plans saying that the vendor then in charge of managing the provider data collection effort would no longer be allowed to work in CA.

Sutherland reported that, at that time, 40% of data records contained errors or omissions. The result was that health plans could not confirm members for timely and appropriate access to care, and providers were subjected to unnecessary inconvenience, cost and fatigue. The opportunity for a vendor of business outsourcing services, conversely, was significant. Since two-thirds of data collection efforts by different health plans required the same basic information from providers, Sutherland identified an opportunity in California to generate value by eliminating unnecessary work and collecting a slice of the resulting value, while simultaneously providing value to the regulatory body, providers, and patients.

Geographic & market segment extension of the model

The geographic extension of this model in physician network data management beyond California may be a logical next step. Sutherland itself calls its shared services model for the provider appointment availability survey (PAAS) a “proof of concept”. The fact that Sutherland has successfully united the interests of competing health plans with those of providers, patients, and the state regulatory body lends credence to the idea that other health plans in the U.S. might be convinced to join a similar consortium. Note that some health plans would likely never be candidates, such as Kaiser Permanente, which is based on a vertically integrated model that unifies the management of provision and reimbursement of care. (While Kaiser provides Medicaid services in California, it is not a member of Sutherland’s current shared services model in CA).

However, whether led by Sutherland or another entity (private or public sector), such a consortium could eliminate waste on a state-by-state basis, or even more broadly. The model could be extended to other government healthcare. It could standardize and streamline data collection, present accurate data to a wide range of stakeholders in timely fashion, standardize reporting, reduce provider fatigue significantly, and improve customer/patient access.

Generating leverage

Creating a public utility by mandate may lead to inefficient, unintended consequences, but Sutherland’s success seems to indicate that a market solution can be viable. The CA consortium currently counts 14 health plans, but replicating this success outside CA would require customization to other economic and political circumstances. The mission of the Council for Affordable Quality Healthcare (CAQH) and other associated alliances, non-profits, and government agencies may align with such efforts. Companies that specialize in providing outsourcing services have, as Sutherland proves, many of the capabilities required. Short of a government-sponsored mandate, how can health plans be induced to share proprietary data and data methodologies?

Political leverage might be hard to generate among consumers/patients, but physicians may present a more unified and sharply-focused interest group. If a doctor contracts with a single health plan for multiple products (e.g. Medicare Advantage, Mental Health, etc.) and that doctor’s information needs to be verified for each product, this would require multiple touches, cost, inconvenience, and fatigue. According to Sutherland’s experience in CA, that doctor may, on average, contract with 20 health plan products. The doctor is therefore incentivized to reduce this duplicative and wasteful interaction, and the argument that physician rosters can be harmonized among health plans with minimal interaction (leveraging web portals rather than call centers) is not hard to make. Having thus grasped the challenge, the physicians’ professional organizations may be well-placed to work with health plans to set up more consortia similar to Sutherland’s in California.

Finding allies

An industry alliance designed to introduce blockchain is aimed directly at the challenge of reducing the estimated $2.1 bn in cost associated with maintaining provider data. According to an April 2018 healthcareITnews.com article, Optum, UnitedHealthcare, Humana, others launch blockchain pilot, these industry titans are exploiting the opportunity to reduce waste associated with provider data: “Five healthcare organizations including insurers UnitedHealthcare and Humana, Optum, Quest Diagnostics and MultiPlan are launching a blockchain pilot to help payers tackle mandated provider directories”.

The mission of this alliance may provide a long-term objective to which one or more consortia based on the Sutherland CA model might be mutually supportive. The hype associated with blockchain might create the attention necessary to establish more provider data consortia, while the political clout of physicians’ professional organizations might bring leverage. In combination, private sector players might then find the resources and support necessary to align economic incentives, manage workflows, normalize and de-duplicate data, execute against state and federal regulations, and package provider data in digestible, accurate, up-to-date formats for the constellation of healthcare stakeholders.

]]>

Benefitfocus, the cloud-based benefits management platform and services provider, recently hosted 1,200 benefits professionals at their annual One Place conference in Charleston, S.C. The conference featured updates on Benefitfocus’ strategy, enterprise benefits management technology platform, and partners from its ecosystem; and presented an opportunity to learn from industry thought leaders, technology partners, benefits suppliers, and insurance brokers. On the final day of the event the company facilitated employer efforts to build benefit strategies and experiences at what was billed as the industry’s “largest open enrollment planning event”.

During the event, Benefitfocus updated customers and ecosystem partners on seven key topics, as covered in this blog.

Shift in corporate strategy

Benefitfocus has embarked on a significant strategic realignment. The company is shifting its company strategy from selling software to facilitating a benefits industry platform (or marketplace, such as Amazon). The company has been influenced by the book Platform Revolution, written by MIT professor Geoffrey Parker, who was introduced via a recorded video after having visited the company at its campus headquarters in South Carolina. Parker’s book instructs leaders how to start and run a successful platform business such as Amazon, explaining ways to identify prime markets and monetize networks.

Benefitfocus’ ambition is to “connect benefits buyers and sellers in unprecedented ways” and be accepted in a new bracket of peers, including Amazon, airbnb, and Uber. In practical terms, newly introduced analytics are designed to allow sellers and brokers using Benefitfocus’ SaaS software to segment employer customers and employee populations for “improved benefit strategy, communications and engagement, while giving employers robust visual interactive tools to quantify the value of their benefits programs and serve their employees.”

However, questions regarding the practical ramifications of this strategic shift remained unaddressed in the general sessions, including:

- The shift from a software development culture habituated to a standard, planned software roadmap and update release schedule to a “platform” culture habituated to agile development

- Adaptation of the Benefitfocus sales channel, sales methodology, sales collateral, sales and marketing resource roles, responsibilities and staffing

- Development of an ecosystem partnership within a complex web of coopetition (in which medical carriers, for example, may currently go to market on the Benefitfocus SaaS software, white label Benefitfocus, and/or go to market concurrently with their own home-grown development platforms).

- Development of the benefits administration professional community within Benefitfocus’ ecosystem of employers, consumers, and benefit providers.

Software updates

Benefitfocus platform updates that resonated strongly with benefits partners included:

- Mobile App: It is now possible to email or text health data to a physician, including proof of insurance. This is a service not only for the consumer but for the insurance carrier that wants to have accurate data conveyed to physicians in real-time. The Mobile App aims to simplify consumer engagement, total rewards details, and digital ID cards. Enrollment can now be accomplished using the Mobile App.

- Chatbot: Embedded in AI engine BenefitSAIGE, this 24-hour chatbot drives content and recommendations to consumers every type of benefit at every stage of life. It also frees the HR professional who is ordinarily called to interface with consumers about the benefits platform and benefits companies. Chatbot communications limit delays generated by hand-offs as a consumer inquiry passes to the HR professional, to a benefits broker, to a benefits vendor, and then returns back to the HR professional and finally the consumer. The chatbot also drives appropriate benefits enrollment in “smart moments” that matter to consumers.

- Digital Wallet: This feature enables flexible payment options beyond payroll deduction. Payment using personal credit cards can also be accomplished using the Mobile App. The platform now allows employees to purchase insurance at any time during the year, not just during a two-week open enrollment period.

Other notable added software functionality includes:

- Data interchange and automation enhancements, analytics and communications enabled by AI engine BenefitSAIGE. The AI engine leverages rules-based systems, RPA, machine learning, predictive analytics, and natural language processing. This AI engine aims to improve data interchange, drive insights, improve the consumer experience, and influence transactions during “smart moments”

- Ecosystem productivity enhancements via data exchange, APIs and automation, supported by security and data protection.

Benefitfocus reports that over 25m consumers are now served by its software platform. Clients include 170k+ employers, from Fortune 500 companies to small employers, featuring 17k brokers, 144 medical benefits carriers, and 30+ marquee voluntary and specialty benefit brands.

Data cleansing

The company reports that a $30m investment has produced a dataset with “99.6% data accuracy on first-pass yield, eclipsing the industry average of 95%”. The dataset includes records of 2.7bn data transactions in 2018 alone.

Adding a portable life insurance partner

BenefitsPlace now features Afficiency, an InsurTech that is working with life insurance carriers to offer portable voluntary life insurance benefits.

Adding consumer-directed health partners

The company has also added greater choice of consumer-directed healthcare (CDH) account options, including Wageworks and Payflex. API connections are designed for synchronized, accurate and real-time data exchange. Year-round education and communications should help consumers maximize their CDH contributions, including the triple-tax benefits of funding their HSAs.

Introduction of personal lines insurance products

On the existing software platform, insurance carriers and specialty product suppliers gain a dedicated digital distribution and enrollment channel to more than 23m consumers on the Benefitfocus platform. Carriers included in this first iteration include:

- Bristol West Insurance Group: a member of the Farmers Insurance Group of Companies (PL auto)

- MetLife Auto & Home: Metropolitan Property and Casualty Insurance Company and its subsidiaries, operating collectively under the MetLife Auto & Home brand (PL auto and homeowner)

- Toggle: launched by Farmers Insurance in 2018 (renter’s insurance).

Benefitfocus offers P&C insurance through licensed brokers at discounted rates.

Innovation incubator

Benefitfocus announced its InnovationPlace, a startup partner program. The company aims to introduce innovative products and services to employers and their employees through its SaaS facilitated marketplace. The company has created an innovation incubator on the company’s South Carolina campus, and welcomed its first occupant, Rock Health, an innovator in women’s health.

]]>

In this blog, I look at how Sutherland tackled the challenge of health plans maintaining accurate provider data in the state of California.

The challenge: inaccurate health plan data about providers

It’s been difficult for health plans in California to maintain accurate, up-to-date information on the current status of providers in the state. According to outsourcing vendor Sutherland, experience indicates that 60% of provider directories contain serious material errors. Health plan data frequently indicated that doctors were no longer accepting new patients, even though they in fact were. The data frequently presented the state regulatory body, health plans, and patients with inaccurate information about whether doctors continued to practice their specialty, had moved to new locations, or were contracted to work with particular health plans or their products.

The context: gaining access to timely CA medical services

Since 2017, Sutherland has created a shared services model for over a dozen CA health plans that obviates the need for participating California health plans to each separately build and update parallel databases that track the availability of provider appointments for urgent and non-urgent care for health plan members. The State Department of Managed Healthcare (DMHC), which regulates the state’s health plans, requires that health plans and providers make available appointments for urgent and non-urgent care, varying by specialty, from two to 14 days. Until recently, each health plan created and updated its own massive database of providers that participated in each of those plan’s products.

In a state in which Sutherland reports that the average provider contracts with ~ 15 health plan products, the law resulted in a myriad of duplicative efforts, each of which imposed burdensome requirements on providers.

The Sutherland solution

Sutherland has initiated a shared services platform that reduces this burden for health plans, providers, and state agencies, and increases the accuracy of reporting to the DMHC. In particular, Sutherland spearheaded the coopetition of health plans in California in 2017 by creating a shared services model that built and updated the Provider Appointment Availability Survey (PAAS) on behalf of a consortium.

Prior to that, Sutherland had been in conversations with the state of California on a related topic, and that conversation helped initiate Sutherland’s PAAS project with the state. Sutherland had already built a relationship with Blue Shield of CA, which became the anchor client. Other state-based and national health plans joined the consortium in 2017, totaling eight by the end of 2017. By the end of 2018, 12 health plans had joined the consortium and Sutherland now counts that consortium at 14 health plans.

Sutherland estimates that it now touches ~ 100K doctors, each of which has contracts with an average of two plans. This hub-and-spoke shared services model eliminates duplicate outreach to CA providers, saving each participating health plan from the costs of maintaining separate call center facilities and databases, and saving providers from responding to multiplicative health plan outreach regarding the same basic data. Sutherland also manages all the workflows involved with credentialing a new provider, verifying diplomas, board certifications, and combing regulatory authorities for any information on sanctions against providers.

The company estimates that it reduced associated health plan physician data management costs by 75% through elimination of duplicative work and by improvement in survey execution workflow and other improvements. Sutherland estimates that it reduces the touches on providers from 3 to 1 call per practice, improves reporting and other interactions with the California regulatory body, and improves patient access to timely care.

]]>

NelsonHall recently attended HIMSS19 in Orlando, Florida, the largest healthcare IT conference in the world, with over 45K delegates attending and 1.3K vendors in the exhibition. Here are three highlights from the many conversations we had about the state of the healthcare industry.

Obstacles to improving CX

The conversation about “consumer experience” in healthcare organizations invites harder questions about the challenges and obstacles to building customer intimacy. NelsonHall spoke with leaders at several BPO vendors about CX:

- DXC Technology: Gurmeet Chahal (the new VP & GM - Americas Head for Healthcare & Life Sciences) suggested that the chief obstacle to providing better CX appears to be the governance and supply of better data. DXC observes this is especially true among provider organizations

- Atos: Jack Evans (COO - Digital Health Solutions, North American Operations) suggested that healthcare organizations lack the capacity to effectively manage many constituencies and peer organizations “in a multi-source world” in ways that unite operations in their efforts to promote intimacy with customers across business units and channels

- Genpact: Rakesh Nangia (VP, Life Sciences and Healthcare) suggested that healthcare organizations are stymied in their ambitions because they lack clarity on ownership of CX across the organization. While healthcare organizations are investing and experimenting to improve CX, healthcare organizations have thus far failed to reorganize budgets, people, and technology around CX priorities and measures under comprehensive and authoritative leadership.

Each of these vendors is making significant investments to provide better CX offerings to healthcare industry clients under the rubric of “digital transformation.” DXC has invested in internal data platforms that unite front-office and middle-office functions with security, workflow, and automation capabilities. Atos acquired financial services powerhouse Syntel for $3.4b in July 2018 and aims to make that company’s customer intimacy models relevant and compelling to healthcare clients in North America. Genpact also aims to transplant CX expertise from BFI into the healthcare industry. For more information on Genpact’s September 2017 acquisition of TandemSeven and its relevance to CX, see Rachael Stormonth’s blog here.

RCM in the crosshairs

Many BPO vendors see opportunity in the healthcare provider RCM sector. For background see my blog U.S. RCM Outsourcing Services Market Ripe for Consolidation. BPO vendors often see RCM industry fragmentation and inefficiencies as opportunities for consolidation and automation, and we found this view echoed by major BPO vendors present at HIMSS19. They use similar language to describe enticements and hurdles expanding business in this market segment, remarking on:

- Consolidation in the provider hospital systems market, rationalizing RCM operations

- The large scale of U.S. RCM services market

- Labor arbitrage opportunities for smaller RCM services vendors to move operations offshore

- Automation opportunities for IT-savvy BPO vendors to leverage scalable IT platforms

- The relatively low risk of taking over operations that have limited capital requirements and manage stable cash flows.

Depending on the vantage of the BPO services vendor, the relative immaturity of provider organizations’ procurement functions can be viewed as a positive or as a negative. Incumbent BPO vendors that have cultivated broadly-based, enduring relationships with providers enjoy significant barriers to competition. But those entering the space for the first time similarly must earn trust in complex, decentralized clinical and administrative constituencies (many of which are oriented by mission rather than profit) that prioritize “friends and family.” Several BPO vendors we spoke with appear to be actively exploring opportunities for expanding their businesses, cautiously, in the RCM market segment.

No new news on BPaaS

There was only limited discussion of moving healthcare operations root and branch into outsourcing arrangements. Cognizant has been advocating for healthcare payers of all stripes to focus their strategies and find efficiencies by utilizing its business process as a service contract (BPaaS) offering. The sales cycle for such a deal lasts, we expect, for at least two years, but we aren’t seeing fruit from Cognizant’s efforts.

Furthermore, we didn’t hear new news from NTT DATA. With November’s Q3 financial results NTT DATA announced it had sealed a $200m deal with an as-yet unnamed payer client. The investor presentation had stated that a deal for application management services, BPO, and infrastructure services for a U.S. payer had been signed for a seven-year period with a total contract value of over $700m. However, we have yet to learn additional substantive details.

]]>

The healthcare revenue cycle management (RCM) BPS market is becoming technically more advanced as vendors experiment with RPA to drive greater efficiency and productivity, and to improve competitive positioning. Here I look at one such vendor, Access Healthcare, and the lessons they have learned from their own RPA initiatives.

Access Healthcare generates ~$145m in revenue delivering RCM BPS through 11,000 employees, with operations based mainly in India. Both its President and founder, Shaji Ravi, and its Chairman, Anurag Jain, had worked for Perot Systems’ (and then Dell Services’) healthcare practice prior to Access Healthcare being established in 2010. Access began to make strategic technology investments after Anurag joined in 2012, with the objective of improving productivity significantly beyond what was possible with its India-based labor arbitrage business model.

Lesson 1: Assess whether to build or buy your own RPA platform

Initially, Access Healthcare experimented with various RPA packaged software such as that offered by the leading horizontal vendors. According to Jain, his company discovered that trying to apply RPA packaged software to healthcare RCM processes ultimately proved inefficient. “[Packaged RPA software] is like a big Lego set with no instructions,” he said. “Efficiency with IT assets is the key and we found it more efficient to build our own technology platform.”

Ultimately, the company decided to build RPA capabilities onto the company’s existing IT platform (based on Microsoft.NET and SQL Server), calling the platform arc.in.

Lesson 2: Broaden your perspective when identifying efficiencies from RPA

Experimentation with RPA prompted Access Healthcare to think more broadly about the efficiency of its internal IT function and other areas of its organization, including HR management, data management, and workflow. The company resolved to integrate these considerations into the development of its enterprise platform to simultaneously streamline the management of people, data, and finally, customer-facing RCM processes.

As Access Healthcare worked to move beyond labor arbitrage and a transactional business model, Chairman Anurag Jain said he realized that “the real objective is not to make the customer’s processes and transactions more efficient but instead to make their work disappear.” The implication, he continued, is that it requires deeper partnerships with clients that incentivize all parties to generate and share the benefits from the work that disappears.

Lesson 3: An effective, scalable technology platform can generate M&A and partnership opportunities

An RCM BPS company with an efficient and scalable technology platform can expect to benefit by extending its technology capabilities across the operational functions of other RCM BPS companies and across other RCM market segments. And this can create opportunities for acquisitions of, or partnerships with, other RCM BPS companies.

Jain has pursued this line of thinking as he considers what he believes to be his firm’s cost advantage over other, less technologically advanced, RCM BPS vendors. He groups these cost advantages into two categories: workforce management and automation/analytics.

Workforce management

Access estimates that this category generates a 7-10% operational cost advantage over competitors. The costs of Access Healthcare employees equal those of management, which together far outweigh all other costs. Hence, technology that reduces management and employee costs is prioritized for investment. Access has developed proprietary technology for:

- Workflow tools: data and tasks from 150 payers and 300k+ providers are routed to appropriate teams and individuals, resulting in greater per-seat productivity

- Performance analytics: monitoring systems predict when employees are likely to be dissatisfied, when management intervention is necessary, and how managers can address dissatisfaction

- Automated incentive program: employees are motivated and monitored through use of a reward program that can equate to 20% increase in salary and accelerate promotions

- HR systems: help automatically manage a 2% per month attrition rate while simultaneously growing headcount. Every month, Access uses its software tools to manage 4k candidate assessments and 2k people in the recruitment process.

Automation/analytics

Access estimates that this category generates an 18-23% operational cost advantage over competitors. It estimates that when a bot is successfully deployed, a CSR can be spared 30-40% of his or her effort in executing a given process. After experimenting with tools from UiPath, and having evaluated Blue Prism and Automation Anywhere, Access discovered that it gets better results from its proprietary “echo” RPA software suite developed on its in-house arc.in platform. And because the platform is developed on Microsoft.NET using SQL Server databases, it is relatively easy to find the talent necessary to build and maintain its systems. Points of note here include:

- Process improvement team: The Six Sigma team operates with a holistic view of enterprise and client processes. This team identifies/prioritizes/writes requirements for automation opportunities

- 100+ developer team: This team builds and maintains the proprietary platform and tools, and includes 40+ developers to configure and deploy the proprietary “echo” RPA software suite

- Modular architecture: The company believes that the automation architecture should be built with process components in mind. Micro-bots should be able to automatically hand off work to each other if necessary, and micro-bots added to a library by process SMEs should make the architecture scalable

- Bots: The flexible platform enables a 4-6 week build and deploy period for new bots, and 1k+ bots are in production. Automatic logs enable measurement of the impact of bots on transactions and clients

- ML: Machine learning tools predict payer responses to specific transactions over time, enabling Access Healthcare to define and customize more effective workflows. ML tools also help prioritize investment in building and deploying new bots

- Point solutions: The company has also created platform-compatible applications for payment posting, claims follow-up, and denial management.

Confident in the advantages conferred by its own technology platform, Access Healthcare acquired Pacific BPO, another RCM BPS company in an adjacent healthcare market segment, in September 2018. Having assessed that company’s functional processes to be largely manual, Access believes it can use its platform to generate significant efficiencies. Access also believes that it can bring a new level of technology sophistication to a market segment ripe for the introduction of process re-engineering and automation.

]]>

The challenge of rising healthcare costs in the U.S. has been obvious for decades. Or has it? Various interventions have been attempted, but health costs as a percentage of GDP are forecast to continue to climb. National U.S. healthcare expenditure as a percentage of GDP has risen from 17.2% in 2011 to 17.9% in 2017.

In February 2018, the U.S. CMS Office of the Actuary estimated that “growth in national health spending is projected to be faster than projected growth in GDP by 1.0 percentage point over 2017-2026. As a result, the report projects the health share of GDP to rise from 17.9 percent in 2016 to 19.7 percent by 2026.” GDP growth over the last two periods has kept pace with rising healthcare costs over the last two years, but when GDP growth subsides, the healthcare cost challenge will reemerge. The current stalemate at the U.S. federal level about the path forward for healthcare reflects a lack of consensus about root causes and, therefore, advisable policy.

The sector has already undergone major restructuring and intervention, both government and private sector initiatives. This includes:

- The American Recovery and Reinvestment Act of 2009 (ARRA) incentivized adoption of EHRs – the assumption was that a lack of electronic clinical records technology was a primary component of inefficiency and waste. 90%+ of U.S. hospitals have now adopted EHR technology

- The Accountable Care Act (ACA) of 2010 realigned much of American healthcare reimbursement and delivery – the assumption was that decentralized, misaligned organizations created waste and reduced quality. The ACA introduced a raft of initiatives designed to address waste and improve productivity, particularly clinical labor productivity. The results of most of these measures, including the ACA’s Accountable Care Organization initiatives (ACOs) remain inconclusive

- Consolidation: the payer and provider markets have been roiled by restructuring and consolidation. There were 1,412 hospital mergers between 1998 and 2015; physicians also have consolidated into increasingly larger groups. Moreover, the four largest insurers now account for 83 % of the total national market.” [1].

The largest target for improvement in healthcare delivery costs remains the cost of labor. But does more “technology” improve labor productivity? Not necessarily. Technology can drive rather than retard growth in healthcare costs. According to a Health Affairs (HA) article, “technological changes in the [physician and nursing] sector to date have favored, rather than substituted for, those with high skills" [2]. It depends on the type of work or process, on the technology use case, and on the organizational aptitude for adopting new solutions. Administration, management and IT are oft-cited as a source of burgeoning healthcare delivery costs, but these classes of labor may actually be seen as examples to be followed. Over the 15-year period of the HA study, compensation (change in employment x change in earnings) for administration, management and IT rose only 35.3%. Over the same period, compensation for physicians and nurses rose 80.5%.

Taking a step back, have all the industry-level efforts at restructuring mentioned above missed the mark? Have we simply failed to appreciate how unhealthy Americans have become – and therefore overlooked the root cause of precipitous cost increases? The debates and struggles regarding GDP growth, healthcare delivery cost growth, technology adoption, government intervention, and market restructuring may simply be addressing symptoms rather than causes of the rise in U.S. healthcare costs.

The “hidden in plain sight” fact may be that Americans have unhealthy habits which have national ramifications for healthcare costs. In one 2013 study, only 2.7% of the U.S. adult population could be identified with healthy metrics for exercise, diet, smoking, and body fat. As national healthcare expenditures rise towards 20% of GDP, perhaps we should ask whether the challenge of rising healthcare costs can be adequately addressed by industry-level restructuring efforts. Perhaps this challenge can better be addressed by bottom-up rather than top-down initiatives.

[1] The Commonwealth Fund, Insurer Market Power Lowers Prices in Numerous Concentrated Provider Markets, September 6, 2017

[2] Where the Money Goes: The Evolving Expenses of the US Healthcare System, Health Affairs, July 2016

The healthcare revenue cycle management (RCM) outsourcing services market in the U.S. seems ripe for disruption and consolidation. The macro factors include:

- Contraction in the number of hospital locations and hospital systems

- Speedy erosion in the number of small, independent physicians’ practices

- Increasing complexity in reimbursement models and processes

- Increasing experience and scale of off-shore service vendors

- Decreasing costs of managing RCM operations RPA followed by broader AI and digitalization technologies.

The landscape of RCM platform and outsourcing vendors is highly fragmented and provider organizations considering outsourcing have numerous options. Becker’s Hospital Review listed 110 software and/or services vendors in this space in 2016 and expanded that list to over 160 vendors in October, 2017. Will the RCM outsourcing market become the target of a well-capitalized player or set of players, and if so, will technology be a primary driver of RCM industry consolidation?

Some vendors in the RCM industry certainly appear to have advanced down this line of thinking. Recently I spoke with Anurag Jain, Chairman of Access Healthcare, an India-based RCM BPS vendor, about the disruption and consolidation that he and his company anticipate. Jain believes that if the appropriate automation can be overlaid on standardized, optimized processes and people management systems, then the opportunity to take cost out of U.S. RCM far outstrips the capacity of his own company (and, he implied, the capacity of many of his competitors) to meet that opportunity through organic growth. As a result of this opportunity, Jain foresees a major capital infusion into the U.S. RCM outsourcing industry, with consolidation being one of the consequences.