WNS recently briefed me on its Digital Policy Administrator (DPA) solution/platform, a patent for which is pending and is not yet publicly available. The DPA is positioned as a utility-style third-party administration (TPA) platform for the life and annuities (L&A) sector, built to reduce the burden of legacy technology debt and enable faster rollout of new products.

Market Challenges in L&A

Carriers in the L&A sector face persistent structural challenges. Productivity gains have lagged other industries, even as cost pressures mount. Carriers continue to operate on aging legacy technology platforms, increasing complexity and slow responsiveness. Product innovation cycles are lengthening, just as market volatility and interest rates drive greater demand for flexible annuity products.

Outsourcing is widely used, but it has not resolved these challenges. Four of the top five L&A carriers already outsource parts of their administration. Still, most TPAs remain anchored to labor-intensive delivery models with limited automation. As a result, carriers are unable to fully escape the inflexibility and inefficiency challenges they face.

WNS’ Position in Insurance

Insurance contributes roughly a quarter of WNS’ total revenue, highlighting the importance of this vertical to its overall strategy. It supports ~70 active insurance engagements, employing ~18k insurance specialists. Within this workforce are ~650 actuarial professionals, ~500 data and analytics experts, and ~5k customer experience specialists. The practice also leverages ~50 digital solutions and accelerators to support engagements across all insurance engagements.

Recent acquisitions extend WNS’ digital toolset. Vuram, acquired in 2022, brought automation and BPM capabilities, while Kipi.ai, acquired in 2025, enhanced GenAI development. Together, these acquisitions create a transformation-led approach that is now in ~90% of WNS’ insurance engagements.

Addressing Core L&A Challenges

WNS’ Digital Policy Administrator is designed to address two core barriers for L&A carriers. First is legacy debt: policy administration, billing, claims, and reinsurance are frequently handled on outdated systems that are costly to maintain and difficult to modernize. Second is the challenge of slow product rollout cycles, which prevents insurers from capturing emerging demands in a timely fashion.

WNS positions the DPA as an integrated solution combined with core systems, with proprietary platforms, automation, and global delivery in mind. The objective is to offer insurers an option beyond piecemeal outsourcing, a packaged TPA model focused on measurable efficiency and configurability with speed.

A Utility Model for Policy Administration

The DPA is designed as a utility service rather than as a customized, one-off deployment. Its design principles are straightforward but ambitious. The delivery model follows an automation-first philosophy. In practice, this means processes are automated wherever possible before being offshored; only the most complex elements are retained onshore. The principle is not just to focus on cost optimization but ensuring standardization and consistency across servicing operations.

WNS chose to partner for the policy core rather than build its own. The rationale was speed and flexibility; deploying a proven core accelerates adoption while avoiding heavy in-house development cycles. The platform is cloud-deployed, API-enabled, and designed to support per-policy pricing, aligning costs with actual business volumes.

This avoids lock-in by incorporating open-source components where feasible. Change is driven by configuration, not code rewrites, maximizing reusability and ensuring the system remains upgradable. These design elements support a packaged TPA model that is scalable and adaptable to client needs.

Architecture: Automation-First Design

At the center of DPA is Verisk FAST, the chosen core policy platform. FAST provides new business, policy administration, billing, claims and reinsurance in a microservices and API-based architecture. It minimizes reliance on middleware and reduces the need for patchwork integrations.

Surrounding the core is a set of platforms and frameworks:

- Skense, WNS’ proprietary intelligent document platform for ingestion, triaging, and indexing

- Ushur, supporting voice-to-text, agent assist, and automated outbound correspondence

- Genesys, providing omnichannel routing, IVR, and speech analytics

- Framework integrations, connecting to general ledger systems, policy and agent data, reinsurance, illustrations, and e-applications.

Together, this ecosystem enables straight-through-processing and reduces manual interventions. Automation is designed into the workflow from the start rather than being layered in afterward.

Global Delivery Model

The DPA is powered by WNS’ global delivery model. Work is distributed by geography and complexity. Policy servicing, billing, and collections are managed through back-office teams in India. Voice operations are delivered from South Africa and the Philippines. For complex or high-touch needs such as complaint management, WNS provides onshore delivery to ensure responsiveness and quality.

Supporting layers include IT service desk, infrastructure and security, HR, F&A, and governance/compliance functions.

Early MVP Flows

One example of early product flow is beneficiary change processing, where Skense ingests change request documents and FAST executes the policy updates with no manual interventions.

Additional flows are being added, including surrenders, licensing, and commission management, demonstrating the platform’s ability to move beyond simple transactions.

Target clients are threefold: existing WNS insurance BPO clients looking to modernize, new clients seeking an integrated TPA platform, and current FAST users exploring an overlay model with WNS services.

WNS’ Outcomes with DPA

WNS claims several measurable outcomes from the DPA platform. New product setup can be completed in six to eight weeks, supported by API integrations. The SaaS core is configuration-driven, enabling upgrades without code rewrites. Automation and GenAI augmentation are expected to reduce error rates and operational costs. Pricing is aligned per policy, with fixed implementation costs.

Roadmap for Expansion

AI capabilities are planned to expand into predictive claim prevention, underwriting automation, and advanced pricing models. These additions are positioned to move the platform transactional efficiency toward decision support. The framework is designed for geographic adaptability. WNS has developed an ecosystem framework to allow substitution of core systems to meet geo-specific product requirements, enabling flexibility for clients to operate with technology tailored to their market needs. WNS is currently executing this in the U.K. and Australian markets. It also plans to extend framework services with additional partner integrations and digital servicing capabilities, reflecting insurer demand for configurable ecosystems rather than rigid, closed deployments.

Outlook

The DPA signals WNS’ bid to reposition L&A administration as a standardized utility rather than a labor-led outsourcing model. Anchored on Verisk FAST and supported by proprietary IP (e.g., Skense), the platform reflects an automation-first philosophy designed to scale beyond piecemeal modernization efforts.

While many TPAs and policy administration systems are already moving toward cloud-based, API-enabled, and automation-augmented models, most progress has been incremental and concentrated on standard transactions. Complex flow often remains heavily manual, and pricing still leans towards fixed contracts rather than usage-based structures. Few offerings in the market have demonstrated a fully standardized utility-style model that combines automation across simple and complex flows with per-policy economics and global delivery at scale.

The real test is whether carriers will entrust a third-party utility with functions historically viewed as too core to externalize. Early MVP flows (beneficiary changes, licensing, commissions) are a proving ground, but large-scale adoption will hinge on demonstrating resilience, compliance, and cost predictability under production conditions.

If WNS succeeds with this nascent offering, the DPA could reset expectations for L&A policy administration by introducing per-policy economics, faster product adaptability, and a scalable alternative to fragmented outsourcing. If execution falters, it risks becoming another example of a TPA promising modernization without delivering differentiation. The upcoming 12 to 24 months after market introduction will determine which outcome prevails.

]]>

EXL recently briefed me on how it is leveraging agentic AI in the insurance industry, a sector that is at a turning point in its AI journey. Early experiments with large, general-purpose models have proven what’s possible, but they’ve also revealed what does not work. Hallucinations, high costs, and generic outputs are incompatible with an industry built on precision, regulation, and trust. The next phase of AI in insurance is not about size, but about fit, embedding intelligence directly into workflows, tuned to exact personas that power the insurance value chain.

EXL is combining access to proprietary data with fine-tuned, lightweight models, moving beyond demonstrations of AI potential into real-world deployment. Its approach is rooted in a simple but core concept: building AI agents that think, behave, and make decisions like insurance professionals.

Why General Models Are Not Enough

The promise of massive LLMs like GPT-5 or Gemini is undeniable. They are powerful tools for research, writing, and general reasoning. But in insurance, the stakes are different. Claims adjudication, underwriting, and fraud detection demand more than a generalized understanding of language. They require context, accuracy, privacy, and compliance, all while operating within cost constraints.

A generic model might summarize a news article. But it cannot reliably triangulate 800 pages of medical records, calculate fair claim valuations, or spot subtle fraud indicators buried in policy notes. Bridging the gap between general potential and domain precision is where EXL is building an advantage.

Persona-Based Domain Models

Rather than chasing the biggest model, EXL is building smaller, purpose-built models that mimic specific roles inside an insurance organization. Claims specialists, underwriters, and subrogation adjusters each have their own reasoning process, data dependencies, and decision criteria. By training lightweight models on proprietary derivatives datasets, EXL has created a portfolio of “co-workers” designed to fit seamlessly into insurance operations.

This persona-based approach is reinforced by a deliberate balance across five design factors: accuracy, hallucination control, cost efficiency, data privacy, and latency. The result is AI that not only works, but works in production environments when regulators, clients, and customers demand reliability.

Use Cases Across the Value Chain

Claims Adjudication/Medical Claims Review

- AI agents summarize months of claim history into clean, chronological narratives

- Adjusters can query claims directly with natural language questions, retrieving answers instantly

- Document intelligence agents process incoming files and communications, updating propensity models for fraud, recovery, or liability. In some cases, they even draft recovery letters automatically

- In workers’ compensation, disability, and liability lines, medical files average 500-800 pages

- EXL’s models tag ~40 key sections, generate structured summaries, and deliver consistent interpretations that reduce reliance on overburdened medical staff, eliminating human error.

Life Underwriting

- Finely-tuned models triangulate across medical, financial, and lifestyle data to recommend underwriting decisions

- Instead of a weekly manual review, underwriters gain structured insights in minutes.

Property Underwriting (Multimodal)

- Moving beyond text, EXL integrates images from mobile apps, drones, and satellite surveys

- AI agents review property images to surface underwriting concerns, allowing underwriters to make faster, more informed decisions.

Intellectual Property and Market Adoption

This work is not just conceptual; EXL has secured a U.S. patent for its insurance LLM, with additional patents underway for Claims Assist and other solutions. Early adopters in APAC, the U.K., and the U.S. are already deploying modules, whether for claim summarization, fraud propensity scoring, or recovery optimization

The modular design is intentional. Insurers no longer have to rip and replace existing systems. Instead, they can embed targeted AI agents where pain is the greatest, cutting review times, improving decision quality, and reducing costs step by step.

Why it Matters

For insurers, the benefits are clear:

- Efficiency: reducing adjuster review times from 20-25 minutes to seconds

- Consistency: minimizing variation inherent in human-only decision making

- Cost savings: leveraging lightweight models that are cheaper to run than mega-LLMs

- Scalability: applying persona-based designs across lines of business and geographies.

But the bigger story is cultural. Insurers are moving away from AI as an “experiment on the side” and into a future where intelligence is embedded directly into the workflows that define their business.

The Right Model, Not the Biggest Model

The race to build trillion-parameter models makes headlines, but the more pressing question is who has the right model. EXL frames its agentic AI approach as a way of thinking differently about adoption, one that is persona-based, lightweight, and modular, rather than generic or monolithic. By training models to act like adjusters, underwriters, or surveyors, EXL is positioning itself to help insurers address pain points where efficiency and consistency matter.

From an industry perspective, this is notable. Insurers continue to test and experiment with large, general-purpose models, yielding mixed results, as they encounter challenges with accuracy, privacy, and cost. Agentic AI offers a bridge between experimentation and operational adoption. EXL’s proprietary data rights and patent-backed IP are designed to provide a durable foundation for building agentic AI capabilities tailored to the needs of insurance clients.

The approach and opportunity presented here are promising, though hurdles are to be expected along the way. Adoption has already begun in claim summarization, recovery scoring, and underwriting support, and is expected to extend further into decision-heavy functions where explainability and regulatory oversight will be critical. If agentic AI develops as EXL anticipates, it will not only improve near-term efficiency but possibly reshape how insurers structure work and allocate expertise across the value chain in the years ahead.

]]>

In a recent discussion, NelsonHall explored how WNS HealthHelp continues to modernize utilization management (UM) through scalable AI, real-time decision-making, and configurable service models.

WNS HealthHelp’s platform, Consult™, builds on its evidence-based clinical guidance and continues to achieve high ROI and provider satisfaction through automation and more collaborative provider engagement. For example, within cardiology, musculoskeletal, sleep, and surgical services, a health plan leveraging WNS HealthHelp observed a ~50% drop in denial rates while maintaining stable saving levels.

Accelerating Clinical Decision-Making Through AI

WNS HealthHelp has accelerated its investment in AI across the workflow's intake and nurse review layers. A core enhancement is integrating an AI engine that processes submitted clinical documents, matches them against guidelines, and returns decisions within minutes. This innovation removes avoidable delays and enables providers to be productive while the patient is still in the office.

Unlike traditional UM models, where nurses manually triage all submissions, WNS HealthHelp’s engine ensures that only nuanced or incomplete cases reach their Nurse Review or Specialty Provider Outreach sections. As a result, its clinicians, many of whom are active specialists, can focus on high-impact cases that require true peer-to-peer consultation.

A Modular ’Choose Your Own Path’ Model

Health plans are no longer restricted to rigid UM outsourcing arrangements. WNS HealthHelp now offers three service models:

- UM Elite – fully delegated, WNS-managed solution with end-to-end coverage including technology, expert resources, including medical directors, and clinical staff

- UM Plus – shared technology and resources that extend the payer’s internal capabilities

- UM Standard (BPM) – client-run tech stack paired with WNS clinical and operational support.

These flexible models allow payers to align UM support with their internal strategy, whether scaling fast, minimizing abrasion, or improving turnaround time.

WNS HealthHelp also offers flexible pricing models designed to accommodate different levels of engagement. Options include transaction-based pricing, shared savings agreements, and guarantee-based models tailored to performance metrics. This approach enables health plans to align financial risk with service scope and outcome goals, whether they are pursuing full delegation or targeted support. Notably, the pricing structure is particularly attractive to Medicaid plans and smaller regional payers who need high-impact solutions without taking on the cost or complexity of fully managing UM in-house.

Strengthened Partnerships, EMR Integration, and Clinical Content Expansion

WNS HealthHelp continues to expand its reach and interoperability through a strategic partner ecosystem focused on clinical optimization and provider experience. For example:

- For Humata, WNS supports EMR-integrated workflows that simplify case intake and reduce time spent on case creation

- Through its Availity partnership, WNS integrates its portal capabilities into Availity’s front-end interface, allowing providers to initiate authorizations and access clinical resources within a familiar environment

- In collaboration with Anterior, WNS enhances the clinical integrity of its AI engine, leveraging Anterior’s expertise to improve the efficiency of clinical review processes

- The partnership with InformedDNA allows WNS to rapidly scale its genetic testing programs by incorporating best-in-class clinical guidelines and certified geneticists, helping clients manage complex oncology and precision-medicine cases.

Advancing Provider Collaboration and Outcomes

Rather than relying on denials to drive savings, WNS HealthHelp focuses on changing provider behavior through clinical education and consultative engagement. The model uses matched specialists, such as cardiologists speaking with cardiologists to reach agreement on care plans, resulting in lower abrasion, fewer repeat submissions, and improved long-term outcomes.

WNS HealthHelp reports significantly higher net promoter scores than the industry average, driven by its high-touch, consultative approach, and physician-matched peer reviews.

Looking Ahead: Scaling for the Future

WNS HealthHelp is continuing to evolve its offerings with a focus on flexibility, AI integration, and reduced administrative burden for providers and payers alike.

Future roadmap priorities include expanding AI across additional intake and clinical decision layers, enhancing voice automation for call center efficiency, and introducing new analytics capabilities to track order patterns and utilization trends.

WNS is also working to commercialize its internal tools for broader market access, making it easier for payers to adopt individual components (e.g., clinical guidelines engine, nurse AI review, intake automation) as standalone services.

With growing interest from Medicaid and regional health plans, WNS HealthHelp is well-positioned for the next phase of UM transformation by combining proven savings with improved provider experience.

]]>

NelsonHall recently attended the DXC Connect Insurance Executive Forum in Charleston, South Carolina. The event highlighted DXC Technology’s investment in AI-driven solutions for the insurance industry. A key theme was DXC’s commitment to helping insurers address their ‘technology and process debt’ through community-driven collaboration, enhanced application modernization, and AI-driven operational effectiveness using its DXC Assure platform.

Community-driven collaboration

DXC, like other companies, aims to capture industry insights through advisory councils. In particular, DXC uses structured AI advisory groups to identify and prioritize insurance-specific AI solutions over generic options. Ongoing knowledge feedback loops between client engagements are then incorporated into system testing of these emerging concepts against real-world insurance industry challenges for further model refinement.

Insurers face substantial technology & process debt

A substantial amount of technology and process debt is being faced in the insurance sector, representing ~$180bn-$200bn in hidden costs tied to maintaining legacy systems. Approximately 70% of IT budgets is consumed by legacy system maintenance, and insurers struggle with complex integrations that inflate costs and prolong implementation timelines. These complexities can compound over time with temporary workarounds, further exacerbating technical debt. As a result, insurers often experience deteriorating customer experience despite significant investments.

DXC is addressing these issues through emphases on IT modernization, automation, and cloud-agnostic solutions guided by its ‘racetrack’ framework, providing insurers with targeted maturity assessments and actionable insights.

Hastening application modernization

DXC has introduced products to hasten and facilitate application modernization. These include:

- Community Accelerator – an AI-driven framework to facilitate rapid, community-wide deployment of product updates and enhancements to reduce redundant development efforts

- Conversion Accelerator – combining insurance domain expertise and AI-powered tools to streamline insurance application modernization and reduce process complexity.

Streamlining and expediting policy & claims management

Key AI-led automation initiatives include:

- Assure BPM – to enhance operational efficiency across the insurance policy life cycle with AI-driven data integration and workflow optimization. DXC platforms are integrated with ServiceNow to optimize and streamline policy management, billing, and payment processes to improve the customer experience

- Assure Claims – to accelerate claim processing and improve fraud detection. Assure Claims incorporates intelligent document processing (IDP), using GenAI to extract structured and unstructured data from multiple document formats and leveraging historical data to increase levels of fraud detection

- Assure Answers – a GenAI capability that supports use cases such as an AI-powered chat service for underwriting, policy, and product or claim documentation summaries. For example, it can expedite processing policy cancellations, achieving a targeted ~30% reduction in cycle times. This is driven by the intelligent policy cancellation workflow:

1. The policyholder initiates the process by sending an email to notify the insurer of their cancellation request

2. DXC Assure Answers automatically verifies both the email and policy information contained within the email

3. The CRM dashboard is automatically updated, classifying the policyholder’s request as a ‘cancellation’ to ensure accuracy and eliminate manual errors

4. The cancellation is then processed, and a confirmation email is sent to the customer. This automation reduces dependency on manual intervention and allows staff to redirect their efforts toward more high-value, customer-centric activities.

Summary

DXC Technology is targeting the insurance industry’s dual challenges of technology and process debt, empowering insurers to modernize legacy platforms more effectively and mitigate risk before technological and process debt reaches a critical inflection point. At the same time, the company is introducing GenAI to enhance operational efficiency and insight across underwriting through claims management.

]]>

In recent discussions with WNS, NelsonHall explored the company's advanced healthcare management solutions. WNS provides evidence-based criteria to guide providers in ordering the most appropriate tests, procedures, and treatments for their members. This approach enhances patient care delivery and outcomes while improving provider relations and reducing healthcare treatment costs.

For example, a regional health plan was experiencing high prior authorization denial rates and provider dissatisfaction. The WNS Consult™ platform led to a demonstrated net direct savings ROI of 4.9, improved provider satisfaction and overall savings, and reduced prior authorization denial rates.

WNS’ model is proactive and focuses on behavior change rather than denial of services. It involves proactive outreach to ordering providers, offering clinical education with in-house clinicians, and modifying treatment plans to suit patients’ needs while reducing denials and abrasions.

It aims to continue to reform clinical guidance and authorization in two ways: a rigorous approach to clinical guideline development, and leveraging smart technology. At the same time, WNS offers a flexible approach to which activities it performs and which are retained in-house.

A Rigorous Approach to Clinical Guideline Development

Clinical knowledge is derived collaboratively and utilizes ~600 clinicians while promoting proactive peer outreach and integration of practicing physicians. This ensures that clinical decision-making includes comprehensive medical knowledge and real-world practice, leading to the efficacy of healthcare plans.

The platform’s clinical guidelines are based on research across:

- Governmental quality and regulatory guidelines

- Specialty society guidelines

- Evidence-based literature.

The governance model uses an independent panel comprising WNS clinicians and subject matter experts who review and update guidelines quarterly across ~400 topics and seven specialties. This process ensures that the evidence-based guidelines reflect the latest medical research and regulatory standards. These guidelines are then translated into detailed business rules that guide the Consult platform’s clinical decision-making process with branching logic, if-then, and ‘re-direct’ (auto-approval) rules.

Streamlining Authorizations with the Consult Platform

The authorization process begins with an order request submitted by the ordering physician through various channels (e.g., phone, fax, web, EHR). It enters the Consult platform and into its regulatory rule engine, which deciphers the requests against business rules and clinical guidelines. If the rule criteria are not met, the request progresses through a three-tier assessment and review before a denial or authorization is granted:

- Tier 1 – Initial assessment conducted

- Tier 2 – Nurse review

- Tier 3 – Peer-to-peer review.

If an order reaches Tier 3, the peer-to-peer review determines the appropriate course of action, which can result in a major procedure change or withdrawal of the order request. At any of the tiers, notifications are sent to the ordering provider and member if authorization is granted. If a request is denied, WNS issues a denial letter and handles all administrative communications, including denial language.

The Consult platform supports EMR connectivity and API-based architecture to provide seamless integration with existing healthcare systems, facilitating real-time data exchange, and improving the responsiveness of healthcare services. The platform has achieved ~80% automation and ~70% portal adoption, demonstrating high efficiency and user engagement.

The application of predictive analytics and AI within Consult allows for more intelligent decision-making and enhances the ability to forecast patient care needs and outcomes more effectively.

Offering a Flexible Service Model

Recognizing the diverse needs of health plans, WNS offers both delegated and non-delegated models, allowing for flexible integration of their services according to the strategic goals of the health plan. These models range from handing over everything from case intake to appeal management to WNS (delegated model) to health plans opting for non-delegated models, keeping certain services in-house (such as medical necessity decision and appeal management).

Looking Ahead: Continuous Improvement and Expansion

The WNS future roadmap includes clinical and non-clinical investments. Clinical expansion includes increased coverage of genetic testing, oncology clinical pathways, and post-acute programs. The non-clinical expansion includes enhancing the platform’s capabilities to include order pattern intelligence, UMaaS, and enhanced member engagement.

WNS’ initiatives will continue to offer improvements in how healthcare services are managed and delivered, leading to better outcomes for all stakeholders.

]]>

NelsonHall recently attended the DXC Connect Insurance Executive Forum in Charleston, South Carolina, where the theme was ‘Connecting the world’s largest insurance community to solve challenges and drive value’. DXC focused on:

- Its new product strategy to meet insurers’ transformation and investment needs

- The ability to combine its SaaS solutions with BPS to offer BPaaS services

- AI-based enhancement plans.

New product strategy launch

DXC has adjusted its product strategy to enable its clients to adopt an investment strategy or strategies dependent on their level of need to transform vs. minimize new investment. The key elements are:

- Protect – aims to safeguard organizations’ present investment while improving their existing capabilities, managing systems, and refining their environment for optimal performance. This is suitable for organizations that wish to minimize their investments while modernizing their infrastructure and optimizing their running costs by moving to a consumption-based cloud model

- Extend – access to innovative solutions, leveraging APIs and AI, and ensuring a secure system of records. This is the next step to add new functionality incrementally. Here, DXC stresses the importance of an ecosystem approach, though based on the client retaining their existing core insurance platforms. This involves incorporating these platforms into a wider ecosystem with approaches such as RESTful APIs. The ecosystem then facilitates co-innovation through access to additional point solutions, adding new capability and flexibility to switch functionality in and out

- Transform – for organizations looking for a more fundamental IT modernization. This involves digitalizing with AI and cloud-enabled solutions, making new upgrades to the DXC Assure platform, and operating in a more transformative model.

DXC’s improvement and investment strategy is strongly influenced by its user groups. Over the last year, DXC has made ~466 total enhancements to its P&C solutions, and 49% of these enhancements were community-led.

P&C BPS powered by DXC’s Assure

DXC’s Assure SaaS platform enables insurers to efficiently accelerate expansion capacity to new markets/geographies, with DXC BPS personnel providing access to expertise and support options tailored to the client’s transformation journey. DXC provides support across all 50 U.S. states; it will enhance, run, and maintain platforms and currently supports ~$2.6bn of direct written premiums.

DXC supports all insurance LOBs (e.g., workers comp, flood, commercial, specialty, and personal) and notifications services clearinghouse with ~4k trading partners, 40k endpoints, and robotic enablement.

DXC provided a use case of an insurer receiving 1,000 emails with attached documents and involving manual triaging of e-mail type, classification, and data re-entry, leading to inefficiencies in processes and increased chances of human error. DXC leveraged DXC Assure Submission and applied AI and ML. 95% of submission emails were converted to actionable data within 2 hours of receipt with a ~90% accuracy rate.

AI enhancement to DXC Assure solutions

DXC is making a major push to leverage generative, predictive, and cognitive AI solutions. They have established an AI strategy which focuses on three core areas:

- Customer AI – for improved customer experience, areas of change include a hybrid call center, real-time sentiment analysis, and GenAI knowledge assistants

- Company AI – for operational efficiency, appropriate knowledge management, and improving business outcomes

- Community AI – for a collaborative approach with real-time feedback and easier use of innovation.

AI-based enhancements that will be available in Q2 2024 include:

- DXC Assure Legal – end-to-end litigation management solution leveraging AI to automate processes for guideline compliance. Allows greater visibility and control over legal spend, leading to less time reviewing invoices

- DXC Assure Claims – partnering with AWS, a new omnichannel function that enables claims professionals to initiate texts and calls from the claims system. This addition reduces the time needed to resolve claims and furnishes a thorough audit trail of the interaction

- DXC Assure Submissions – leveraging AI and ML to extract data from semi-structured and structured submission documents. The AI is taught to distinguish critical data points from unnecessary data, reducing processing time and error rates

- DXC Assure Cede – integrating GenAI capabilities to enhance data in real-time as users navigate the system. The platform examines current SOPs, manuals, and documents to offer instantaneous summaries, enhancing productivity and user experience.

Next, DXC is further extending its AI use cases to reinsurance and Australia’s workers’ comp, both areas in which the company is already active.

Conclusions

- DXC is aiming to offer smooth migration paths from on-premise legacy insurance solutions to AI-driven SaaS and BPaaS services

- It is developing ecosystems of complementary solutions that insurers can adopt on a plug-and-play basis via APIs

- While not all GenAI PoCs will be successful and become widely deployable, DXC is making a major push to incorporate generative, predictive and cognitive AI into all its insurance modules.

In 2020, the U.S. healthcare payer BPS market saw accelerated growth in the adoption and design of digital solutions across all functional areas. The acceleration is driven mainly by consumer demand for an "Amazon" experience from their health plans and providers, to know the cost of care for associated benefit plans to assist in plan selection or inform decisions about elective procedures and treatments. It is also driven by approaching federal regulation deadlines. Specifically, regulatory requirements from the Cares Act and subsequent rulings from CMS are driving further steps towards interoperability throughout 2021-2024. These requirements follow the initiatives by CMS offering price lookup tools for outpatient procedures and OOP costs for physician visits for Medicare consumers.

Regulatory deadlines drive digital adoption

By January 1, 2022, private payers and group plans must standardize data files to be made publicly available and shared through APIs. The available data will be an opportunity for insurtechs and technology vendors to develop price comparison tools further and price analyses to inform their development.

After January 1, 2023, these payers must offer online plan comparison tools for consumers to view negotiated provider rates and personalized OOP costs estimations for 500 commonly utilized services. This will require real-time underwriting and price aggregation and analysis, with the ability to segment the data by facility and provider. Then, starting on January 1, 2024, individual and group plan consumers will be able to view the estimation of the total OOP costs, including usual tests, procedures, DME, and other items associated with specific treatment plans.

Opportunities for tech vendors to provide services & digital solutions

Without significant digital transformation, meeting the interoperability and price transparency requirements poses a considerable challenge for U.S. healthcare payers. Legacy and "home-grown" systems perpetuate siloed digital solutions, unstandardized data, and difficulties in designing APIs and intake of external data. The disjointed process becomes even more complicated when payers face these challenges on a seasonal basis to perform market assessments, develop products, and price new and renewed plans.

Additionally, payers face the challenge of complying with continual changes in required API formats, currently defined by HL7's FHIR. Payers will need support in converting or implementing the standard format and subsequent testing as regulations and required formats change, such as federal exchange marketplace plans that must implement FHIR APIs with third-party apps for open data access.

Capgemini spotlight: price transparency offerings

U.S. healthcare payers can obtain digital solutions to support regulatory compliance with Capgemini's price transparency solutions. Capgemini has 15 years of experience in the Medicare Advantage space, providing enrollment and member account maintenance management services, solutions, and advisory support. The recent focus has been on designing analytic and AI-driven tools for healthcare payer and provider clients in meeting regulatory guidelines and customer-driven demands for enhanced digital experiences and upfront cost estimations.

Capgemini offers service-line driven pricing for the average cost of medical care from hospitals and healthcare providers in the consumer's area. Capgemini developed the relative pricing guidance for hospitals, with an average of 1200 parameters per hospital for ~700 hospitals, categorizing both operational and overall spend by diagnosis parameters. The hospitals were then ranked into low, medium, high. In addition to overall price analysis, Capgemini parsed hospital spend by service line to provide cost estimations by diagnosis or treatment.

Capgemini is also working with several Blues to estimate OOP cost projections viewable on the member portal. Capgemini designed a cost calculator for a medical procedure at a specific healthcare facility, including the member's expected copay/deductible. A pricing engine was then implemented into a Blue's member portal to provide hyper-personalization, utilizing both internally available eligibility data and the aggregated market data for variable cost pricing. Currently, Capgemini offers implementations of ranking engines enabled by pricing algorithms and provider registries, returning search results of the top 10 providers most relevant for a specific diagnosis or procedure and the estimated cost of copay/deductible/OOP for each provider.

Capgemini's price transparency work is also heavily focused on utilizing MLR for cost-sharing estimations, including telehealth in the cost estimations. For a U.K. health plan, Capgemini implemented a solution to perform plan comparisons against industry standards, such as a specific member with a particular set of demographics and health characteristics, to estimate the eligibility and cost-sharing – competitive pricing. The solution incorporated several analytics tools to perform analysis and reporting on historical cost-sharing.

By the end of 2021, Capgemini's digital solutions in price transparency will integrate the payers' provider search tools to rank relevant providers based on health outcome metrics. Capgemini continues working with certain Blues plans to develop a marketplace with shared data and real-time quoting for care pricing and plan comparisons, involving interoperability and price transparency initiatives to benchmark the cost of services by area and plan. Additionally, Capgemini's development is focused on creating bundled pricing for all procedures and tests associated with a long-term treatment plan, as will be required of healthcare payers by 2024.

Increased demand and opportunities for digital transformation in the near future

The challenges faced by U.S. healthcare private and group payers present opportunities for technology vendors to provide digital solutions and services for payers to meet both the regulatory requirements and consumers' digital experience expectations. Client engagement types will vary by payer size, as many large payers only require specific solution design and implementation within their existing systems, while many mid-market and regional plans will be looking for BPaaS models of engagement with technology vendors. Payers will be looking for digital solutions to provide personalized real-time quotes for procedures and later for bundled pricing by the treatment plan and expanded data sharing to enable price transparency initiatives.

]]>

WNS has a highly developed property & casualty (P&C) insurance practice handling 30 million claims transactions and ~$12 billion in claims spend annually. The company has extensive capability in property & casualty supporting motor, property, casualty, employer and public liability for insurers, fleet operators, MGAs, global corporates, and municipal authorities. WNS has strong capability in the Lloyd’s & London market supporting specialty lines products. The company has developed a range of proprietary solutions in support of its P&C and Speciality BPM business.

The company has now taken its proposition to the next level by reinventing, automating, and digitizing its claims handling capability to assist insurers in competing with the new generation of digital disrupters.

WNS Seeking to Reengineer P&C Claims Handling to Touchless Process: Proposition – ‘Simplified Claims’

WNS’ strategy is to assist its P&C insurance clients in moving to contactless, touchless claims, with their or clients’ staff only intervening for the decreasing proportion of exceptions that need manual handling, typically for risk appetite, strategy, governance, or customer proposition reasons.

This has the potential to enable insurance companies to dramatically reduce their operating costs while simultaneously speeding up the claims process and increasing customer NPS.

For example, for motor claims, key elements in this strategy include:

- Establishing the liability for approx.70% of claims at the first notice of loss (FNOL) stage, whether received via a portal, email, or voice and then automating all downstream claims management in these cases

- Minimizing dispute timescales and costs by providing a self-serve option for the customer and third-parties to acknowledge an accident’s circumstances and share their versions of events in a timely fashion

- Automating the downstream processes if the policyholder is at fault, with third-party and subrogation interventions handled digitally

- Identifying and progressing fraud throughout its life cycle

- Handling Third Party exposures via complex AI, ML models to assess unstructured data, complete valuations, and make offers.

Similar disruptive solutions to drive high levels of straight-through processing (STP)/one-touch claims are deployed for property (personal and commercial) and casualty products.

WNS is also looking to minimize the insurance supply chain cost. For example, in property insurance, this will involve using images and video calls to cash settle more property claims at one touchpoint, eliminating the necessity for visits by loss adjustors.

Using New Digital channels for More Timely and Effective Claim Notification

One of the pain points with commercial customers and fleet companies is the amount of time taken by end customers/drivers to report accidents. In these large corporate and municipal accounts, WNS has found the average notification time to average 33 days, which leads to a loss of opportunity to intervene and reduce the loss incurred.

Accordingly, WNS is piloting the use of new digital channels so that the driver of a vehicle can effortlessly report a claim in one touch and upload images, enabling WNS to receive details such as the third party’s registration number details within minutes of the incident. This has the potential to be particularly effective in the case of drivers whose lack of fluency in English may be inhibiting accident reporting.

Similarly, for property surge events, whenever there is a warning of a weather event, such as an Australian bushfire, WNS will identify the post/ZIP codes for the areas likely to be impacted and use this new digital approach to share a prepopulated claim form with customers a day or two in advance of the weather event.

This avoids the need for customers to phone potentially heavily loaded contact centers. Instead, they upload details of their losses, and WNS will respond within 30 minutes, providing details of coverage and dispatching services accordingly.

The new digital reporting channel pilots for motor and property claims are at the completion stage and have been successful from customer experience and indemnity spend standpoints.

Enhancing the Competitiveness of a Major P&C Insurer

WNS has applied its claims strategy components to assist a major global insurer in substantially improving its competitiveness through a fundamental reinvention of its claims processes.

The insurer had carried out a competitive benchmark with a major consultancy, which estimated its OPEX to be very high on a like-for-like basis, with contributory factors being the excessive fragmentation of the insurer’s onshore delivery across more than ten onshore sites and its comparatively low usage of automation and digitalization.

WNS initially addressed these issues by consolidating the insurer’s onshore sites to two centers. WNS also made operating model changes at one of these sites, introducing a collaborative team structure with client staff working alongside WNS staff on a co-branded production floor. A WNS site head runs the site, and in addition to agents, the WNS site personnel include process leads, continuous improvement consultants, and RPA and analytics specialists. The overall client operations delivered by WNS leverage a combination of onshore and offshore delivery.

Secondly, considerable automation and digital interventions have been introduced into the insurer’s motor, property, and casualty claims process. These digital interventions are funded through an innovation funding mechanism that ensures “continuous improvement is a way of life by design”. WNS initially provided resources to deliver productivity improvements, taking a share of the resulting savings, part of which is then used to self-fund further productivity initiatives to establish a continuous reengineering cycle.

Within the new digital model, each new claim reported via the digital channel is run through an automated liability solution, followed by an early settlements, total loss, recovery, and fraud identification model, all integrated via a simple process flow running seamlessly in the background. These interventions are followed by automation of the appropriate downstream activity, such as booking the vehicle for repairs, courtesy car allotment, etc. For suspected total losses, the claim details are run through a total loss predictive tool. These processes for both repairable and total loss motor claims are supported throughout by a self-serve E-FNOL app and fraud screening.

The liability predictive model used by WNS within this contract is based on partner insurtech technology. The system automates digital liability handling within motor claims, including:

- Prompting using image-based questions to establish the accident scenario, including testimonials from witnesses, using links to Google Maps and historical meteorological data to help pinpoint the accident's exact location and weather conditions at the time

- Sending allegations to the third party for self-serve input and responses

- Integration with case law to assist in decision-making

- Built-in AI to identify fraud and subrogation opportunities.

Overall, WNS uses various commercial models ranging from FTE, transaction-based pricing, management consulting fees, and gain share within the contract. Although personal lines claims within the contract are largely paid on transaction-based pricing, WNS is additionally committed to guaranteed percentage efficiency and indemnity improvements together with customer journey improvement.

The overall benefits achieved for this insurance company included:

- Improvement of 15-20 NPS base points

- Improvement of +30 employee NPS (ENPS) base points

- ~50% OPEX reduction

- ~2% motor indemnity reduction.

Digital front doors and transparency a new normal for healthcare?

U.S. healthcare is no stranger to an environment of continuous change and has not been spared the effects of the COVID-19 global pandemic in 2020. The unique circumstances born from the need for social distancing during the pandemic have accelerated healthcare consumers' demands for digital transformation. The ask comes from all healthcare continuum vantage points – patients, providers, payers, and vendors. Healthcare must change its practices to allow for more seamless digital interactions to meet these demands.

As with other service industry sectors, healthcare consumers want the option to access their health services virtually – evidenced by an increase from an 11% utilization of virtual visits in 2019 to over 45% in 2020. Some larger health systems have made this transition without significant challenges, expanding telehealth contracts, and receiving service reimbursements for both commercial and federally funded insurance types. However, many providers were faced with the decision to either suspend their practice or invest in digital platforms or services to offer virtual visits. Cognizant's Core Admin Solutions support providers' internal processes to offer telehealth and payers and providers in efficiently & quickly submitting process associated claims and authorizations via Trizetto's Touchless Authorization Processing (TTAP). The demand for telehealth has become an independent demand from the initial catalyst of social isolation and continues to be at the forefront of patient expectations. Even the senior population is thought to have few barriers to accessing virtual care, with 84% of sampled senior consumers stating they do not have any technical challenges in attending a virtual appointment with their doctor. With the remote operation of the doctor's visit comes the corresponding demand for total digital transformation; payment processing, e-prescription writing, prescription home delivery, and remote patient monitoring. Multi-faceted companies, like Cognizant, offer a variety of bundled or unbundled services and platforms to help healthcare providers and payers address the increased demands for digital interactions. This new digitization is also thought to reduce costs by increasing care coordination, administration, and manufacturing efficiency.

Providers and Payers are finding that digital products also offer the opportunity to clinically manage their patients and members remotely, with IoT, remote monitoring devices, and health wearables. The consumer can utilize various devices, measuring vitals, health coaching through AI, and tracking other metrics related to health risk factors. 65% of consumers utilize some type of wearable. With this percentage of adoption and available data, providers and payers have an exciting opportunity to address their patients' and members' health outside of the doctor's office. Vendors offer bundled platforms or paired digital services to collect, aggregate, and analyze the patient/member data to facilitate care management efforts by both their clinicians and their health plans. Though this digitization also requires a financial investment from the organizations, the vendors promise a visible ROI in cost savings and improved health outcomes.

Driving the transformation

Regulatory bodies have been pushing healthcare providers and payers towards a digital transformation, most recently with the ONC Cure's Act Final Rule. The rule was created to increase interoperability and access to consumer's own health information. Though the rule pushes providers and payers towards the shared goal of an enhanced patient experience, compliance with these requirements will come at a cost. By 2021 payers will be required to allow consumers access to all their claims and health information and to develop APIs to share data with other organizations and regulatory bodies. Though the compliance will be a financial investment for providers and payers, vendors such as Cognizant can implement or offer platforms to achieve such price transparency.

The Centers for Medicare and Medicaid Services (CMS) has similarly taken steps to guide providers and payers towards a better patient experience. In the 2021 Medicare Advantage Final Rule, CMS announced a change to its CMS Star Ratings measures, increasing the weight of the patient experience metrics. Payers must now invest more heavily in their consumer requirements – digital transformation to achieve an end-user-friendly suite of digital platforms. Cognizant addresses another of these drivers by offering several applications and platforms that facilitate both back-end processes and consumer-facing platforms in assisting payers in meeting heightened digital demands from their consumers. Cognizant's continued investment in Trizetto products offers payers such an opportunity for an enhanced user experience with an automated enrollment platform. Such an offering would make a payer more attractive in the upcoming Medicare Advantage and ACA Marketplace OEP (open enrollment period).

Healthcare organizations are also feeling the pressure for change from InsurTech companies and their partnerships with healthcare providers. These initiatives are attracting members and patients with their omni-channel user interfaces and strategic focus on digital platforms and processes.

Product Suites to Achieve the New Normal

Amongst Cognizant's comprehensive suite of product offerings, their digital healthcare platforms and services support over 200 million lives in the U.S. Payers and providers alike have the option to select a la carte products or bundled services to meet the changing regulatory requirements and evolving demands of their consumer and patient bases. Cognizant continues to exact leadership and be forward-thinking in its current and planned digital transformation offerings and continued investment in Trizetto Healthcare Products ($100m):

- Core Payer and TPA admin solutions, for claims processing and management

- Payer-provider solutions, for facilitating contract pricing and modeling and payment administration. Cognizant has planned offerings for onboarding and credentialing

- Government and Quality Solutions, for enrollment and encounter data management, and support of quality rating measures and reporting. Cognizant is planning offerings for enhanced care coordination

- Care Solutions, for clinical and utilization management and value-based benefits. Cognizant is planning offerings for for automated authorization and referral management

- Data orchestration SoE solutions for data aggregation and engagement. Planned offerings include additional integration and analytics for interoperability.

While Cognizant, and other vendors, offer a wealth of products and platforms for health systems and payers, for many the financial investment required has been a barrier. But COVID-19 is having an impact, in spite of an estimated four-month loss of $202.6bn for hospitals and health systems in the U.S. Every U.S. health system recently interviewed by NelsonHall regarded digital transformation as more important as a result of COVID-19, with increased investments planned in SaaS and cloud infrastructure. Overall, hospitals & health systems in the U.S. have shortened their planning horizons to address short-term priorities and investments. One major healthcare system stated that their planning horizon was now weeks rather than years. The same reduction in planning horizon is also evident in healthcare payers, but here with a need for customer retention combined with a much stronger emphasis on cost control.

As is true in other sectors, the pandemic will likely increase the acceleration of digital transformation initiatives across healthcare, with a clear focus on achieving short-term results (rather than in years), producing very immediate improvements in both productivity and customer experience.

]]>

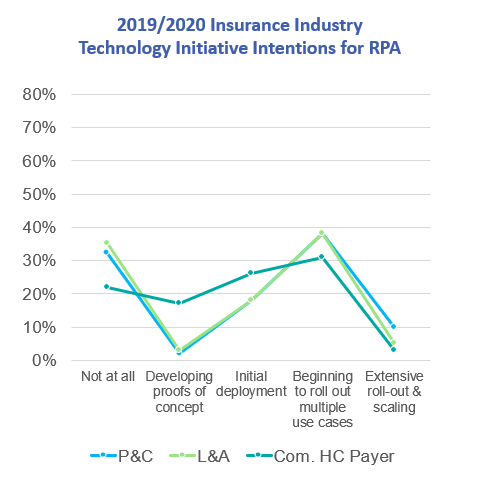

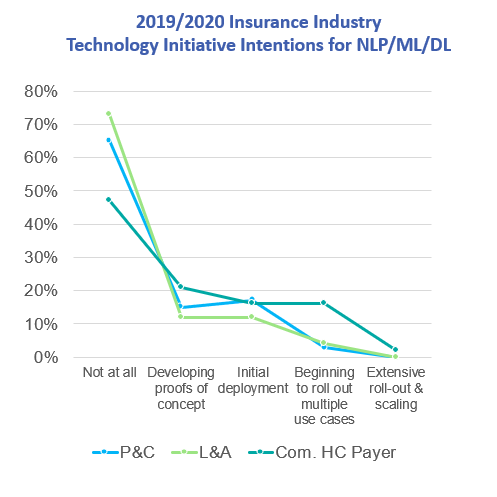

NelsonHall predicts that by 2022, 35% of insurance industry carriers will be in the process of adopting AI technology across multiple use cases within the enterprise. This is based on NelsonHall survey data from the insurance industry that tracks adoption of both RPA and AI (NLP/ML/DL) technology across the property & casualty, health insurance, and life & annuities insurance sectors.

Survey findings

Between 31% and 38% of surveyed carriers are beginning to roll out RPA across multiple use cases, while between 3% and 16% are beginning to roll out AI across multiple use cases – this range includes P&C (3%), L&A (4%) and healthcare payers (16%).

We expect a similar rate of maturity development for AI as for RPA. For RPA, we have seen a wave of investments in proofs of concepts/initial deployments in 2016/2017 develop into enterprise-wide initiatives in 2019/2020. We expect to see the current wave of investments in AI proofs of concepts/initial developments to develop into a wave of enterprise-wide deployments across multiple use cases by 2022. As was the case with RPA, we see a wide variety in the rates of adoption for different types of AI (in particular for natural language processing, machine learning, and deep learning).

The business functions that lead in adoption of AI include:

- P&C insurance: policy origination, underwriting automation, and capacity to manage changes in volume of customer interaction in real-time

- Life & Annuities: policy pricing optimization, contact center real-time customer support, investment support

- Health insurance: product pricing optimization, marketing decision-making.

AI adoption will likely reflect the following broad trends:

- U.S., U.K., and Asia/Pacific carriers will in general lead their counterparts in Continental Europe in the implementation of AI

- Some business functions will provide more fertile ground for adoption of AI, e.g. personal lines insurance policy origination, and customer service will continue to adopt AI more quickly

- Continental carriers will emphasize the importance of customer service and increased speed/ease of new business acquisition in comparison to straight through processing, which is more frequently the top priority for U.K., U.S., and Asian carriers.

General guidance for carriers in adoption of AI

Enterprise governance

Effective enterprise-wide rollouts and scaling of new AI technologies will require strong enterprise governance structures. Efforts completed on behalf of similar enterprise deployments of RPA will pave the way for AI adoption. See the following NelsonHall blog for an example from the health insurance industry: How NTT DATA Established Enterprise Automation Governance for BCBS Health Insurance Carrier

Adapt roles and skills within personnel pyramids

Adoption rates and effectiveness of implementation of AI technologies will ultimately depend on the organizational structures and quality of the people used to transform carrier operations. Carriers will therefore be required to redefine organizational structures, roles and skills. (This will be true whether AI adoption is conducted with or without the extensive use of external consulting and/or outsourcing partners.) Expect significant lag time between the articulation of new organizational structures, roles, and skills, and the period in which enterprises can acquire talent. As with most new technologies, AI experts will be hard to identify, attract and retain, whether compensated directly by a carrier or not.

Align with existing procurement strategies

Procurement strategies that manage external AI partner vendors need to be clear, manageable, and adapted to enterprise procurement structures in place. It’s noteworthy that while outcomes-based, or gain-sharing, contracts get a lot of attention, about 90% of P&C transformational outsourcing contracts in the U.S. are still managed on an FTE, fixed-price, or transaction basis. In Asia Pacific, that proportion is even higher. So, especially for early-stage AI projects, insurance carriers should likely consider keeping outsourcing contracts as straightforward as possible.

Get early buy-in

Winning the race to effective, enterprise-wide adoption of a new technology frequently depends on how innovators introduce that technology within the context of the enterprise. Far-sighted planning may include pilot projects that start small, and then earn organizational buy-in based on clearly demonstrable, early wins. Employee upskilling programs can help allay the fears of those concerned with being displaced by new technologies.

]]>

A magnitude-6.4 earthquake struck Puerto Rico on January 6, killing one person, toppling homes and buildings, and triggering a blackout on the island that is still recovering two years after Hurricane Maria. Governor Wanda Vázquez declared a state of emergency and activated the Puerto Rico National Guard to help with recovery efforts.

How might this earthquake disaster have affected delivery of outsourcing services from Puerto Rico (P.R.) to U.S. clients? Infosys’ response to the devastation caused by Hurricane Maria sheds light on whether the buyers of nearshore outsourcing services should expect significant interruptions to service as a result of such natural disasters.

Infosys’ Puerto Rico delivery center

In 2013, understanding Puerto Rico’s risk exposure to natural disasters, Infosys set up a delivery center in Aguadilla, P.R., as part of a deal to optimize global operations for a client Fortune 500 consumer, engineering and aerospace technology company. Advantages from Infosys’ point of view included:

- Local knowledge: prior understanding of the local Aguadilla business environment through its work with the client

- Rafael Hernández International Airport: located near the delivery center, the transportation hub supports a local aerospace industry that sustains a reservoir of local IT and knowledge services skills

- Skilled local outsourcing professionals: P.R. residents enjoy the full rights and legal protection of U.S. citizenship (P.R. is an unincorporated territory of the United States); they tend to be multi-lingual in both English and Spanish, and tend to be inexpensive compared to counterparts in the mainland U.S.

- Tax relief provided under P.R.’s Economic Development Incentives Act: “the cost structure was a little more amenable in comparison to some of the other locations in the U.S.,” said Aniket Maindarkar, head of Infosys’ Americas operations at Infosys BPO, in 2014. The Puerto Rico Industrial Development Company (PRIDCO) offered a 100% exemption on taxes on earnings and profits, and a 90% deduction on local property taxes. PRIDCO’s executive director Medina explained at the time that “although [P.R. is] part of the U.S., we can negotiate tax rates with companies and they do not pay federal tax rates”

- Staff training and other aid: PRIDCO helped train staff and aided Infosys in finding a new facility location

- High profile political support: Infosys’ investment in a P.R. outsourcing delivery center garnered press exposure through the P.R. Governor’s visit at the opening of the new Infosys facilities in Aguadilla.

Disaster resiliency features

At the time Infosys initially established nearshore outsourcing capabilities in P.R., the company publicly announced it envisioned serving U.S. clients in multiple restricted industries, including defense and healthcare. Within a year Infosys had relocated both retained and new personnel into a nearby 12,000 sq. ft. facility that could accommodate up to 300 people. The relocation retained features that would later prove advantageous to disaster resiliency, including:

- Aguadilla’s location on the northwestern side of P.R. helps protect facilities from strong winds and hurricanes that tend to land on the eastern and southern sides of the island

- The local Rafael Hernández International Airport is supported by the infrastructure of a former U.S. Air Force base and is located less than ten kilometers from Infosys’ Aguadilla facility

- The airport offers direct commercial flights from multiple airlines to the U.S. mainland, including the greater New York City area. This is the location of a major Infosys healthcare outsourcing services client served by its Aguadilla personnel

- Backup electrical power, supplied by diesel-powered generators located at the Infosys facility.

Expanding capabilities to the healthcare sector

Since 2016, Infosys has expanded the capabilities of the delivery center from aerospace industry functions to operations in the communications and healthcare industries. For U.S. healthcare clients Infosys began to build out clinical and IT service desk and support for Medicaid business. Initially, Infosys hired half a dozen P.R. clinical nurses with both bedside and corporate/investigative expertise.

The U.S. legal status and U.S. citizenship of the P.R. personnel supports delivery of restricted defense industry and healthcare industry services (e.g. Medicaid program services) with lower local costs than those of U.S. counterparts. According to U.S. Bureau of Labor statistics, median wages for registered nurses in the U.S. are approximately double those of their counterparts in P.R. However, among the nurses with both bedside and corporate/investigative experience that Infosys recruits in P.R., Infosys’ experience is that the discount for clinical nurse labor rates is narrower: 15-20% discount for a nurse in P.R. compared to New Jersey, and 10% discount for other highly skilled resources.

Lessons from Hurricane Maria

When the Category 5 hurricane hit Puerto Rico in September 2017, it lingered over the island for over two weeks, causing over $90bn in damage and approximately 3,000 fatalities. Nevertheless, despite the scale of the devastation, Infosys reports that its service to clients was interrupted only for one day while it implemented its disaster recovery processes. Diesel generators supplied power to employees for the duration, and most employees resided in the facility rather than go home when off duty. Infosys also retained transportation links with its clients. Despite the atrocious weather, Infosys secured approval to fly by private jet into Aguadilla’s airport on an emergency basis and flew some of its P.R. personnel to client locations in the mainland U.S. Infosys also used these flights to transport vital physical supplies and even cash for salary payments to its Aguadilla personnel.

Through the Maria event, Infosys learned that its communications links required further improvement. Deployment of satellite links into Infosys’ global IT network now enable resilient communications and internet connectivity independently of local fiberoptic and telecommunications infrastructure.

Infosys’ responses to the Maria event have reassured healthcare clients that its facilities in Aguadilla are adaptive and resilient in the face of major natural disasters. Since 2017, Infosys’ outsourcing services from Aguadilla to mainland U.S. clients have expanded, and in the last year Infosys reports that it has expanded clinical healthcare outsourcing services to a second U.S. health insurance company. Infosys now employs approximately three dozen nurses at the Aguadilla facility. Infosys is prospecting for more clients, and has developed contingency plans for bringing other Aguadilla facilities online should a major client win exceed current excess capacity of approximately 60 seats.

]]>

Convex Group is a start-up specialty insurer and reinsurer focused on complex risks, launched with $1.8bn of committed capital in April 2019. Convex will underwrite insurance and reinsurance for “complex specialty risks across a diversified range of business lines” in London and Bermuda. The company aims to adopt a conservative investment strategy with a predominantly high-grade fixed income portfolio and duration matched to the profile of the liabilities.

Development of an Insurance-in-a-Box Operating Model

As a start-up, Convex had no legacy infrastructure or operations and was looking for an “out-of-the-box” insurance and reinsurance infrastructure and operations model, priced on a per transaction basis to enable it to achieve a new level of cost ratio performance.

Accordingly, Convex evaluated multiple vendors against three criteria:

- The extent to which each vendor could align on their operating model and provide an “insurance-in-a-box” offering

- The detailed service model and the ability of the vendor to underpin this model with technology

- The ability to mobilize experienced personnel quickly and execute in a short timeframe.

Following this evaluation process, Convex signed a long-term strategic partnership with WNS in April 2019. The key factors that differentiated WNS following discussions and site visits by Convex in Pune, India included:

- Their depth of insurance industry domain expertise and scale of investment in the industry. WNS has extensive experience in working with global specialty insurers and reinsurers and brokers

- Their service excellence and risk management focus

- Their flexibility in adapting to Convex’s requirements at speed.

WNS has subsequently created a onshore/offshore target operating model and has successfully implemented the technology stack in the initial start-up period of 6 months to manage the HR, Finance and Accounting services, and multiple Industry-specific activities including claims processing, and inward (re)insurance underwriting support. Convex will largely deliver product development and underwriting.

The technology being used is Sequel insurance software, already implemented in support of underwriting, with Oracle cloud software implemented in support of HR and accounting.

WNS Free to Offer Solution to Other (Re)Insurers

With this contract eventually aiming to move toward a per transaction pricing basis, WNS is banking on substantially increased revenues from the contract as Convex becomes established and captures market share in the reinsurance sector, with both Convex and WNS perceiving that the resulting lower cost from this new operating model will provide a source of competitive advantage. Indeed, Convex perceives that by using WNS and this operating model, it will be able to target a cost ratio of 10%-11% rather than the 13%-15% typically achieved.

Convex believes that as a first-mover and start-up with no legacy baggage it can derive greater short-term advantage from this solution than its established competitors, though WNS is free to offer the “insurance-in-a-box” solution developed for Convex to other (re)insurers and sees this as a major new market opportunity as insurers look to reimagine their operating models.

]]>

Dozens of influencers recently attended the WNS U.S. Influencer Day in New Orleans, where the theme was 'Co-create to Outperform’. Through general overviews of its approaches and through client presentations, the company provided insight into its recent success and its future plans. The backdrop for the conference was cheery, buoyed by 7% annualized growth over the prior fiscal year.

Here I look at a couple of highlights from the event, focusing on WNS’ healthcare business and at its approach to business transformation generally.

Healthcare domain expertise

HealthHelp, a company WNS acquired in September 2017, has become the central pillar of WNS’ healthcare business. HealthHelp was likely much larger (NelsonHall estimates >$40m in revenue) than the extant WNS healthcare segment business at the time, hence it is likely HealthHelp became the core around which WNS organized the rest of its healthcare business. Potential integration problems seem to have been avoided by granting HealthHelp a long leash; HealthHelp remains branded as “HealthHelp, a WNS Company”. Both the acquired and the acquiring companies appear to be learning from each other. The broader WNS business may be adopting some of HealthHelp’s approaches to supporting services with proprietary software. HealthHelp’s proprietary software platform reportedly supports the stickiness of its services, and WNS is contemplating ways in which it can further support client services in other verticals using similar proprietary software platforms.

Houston, TX-based HealthHelp provides the foundation for healthcare revenue that is now approaching or exceeding 15% of total WNS revenue. The healthcare vertical anticipates double-digit growth in 2019. WNS’ “non-denial” clinical services enable payers to support providers within its network to provide optimal, cost-effective care. WNS facilitates educational, supportive interactions that enhance provider satisfaction rather than a confrontational or abrasive interaction that degrades provider satisfaction. WNS does this by bringing expert staff from its network of clinical specialists at academic medical centers into conversation with its providers in order to resolve cases that have been determined by the payer or by WNS to be inappropriate for any reason, clinical or economic.

The company’s value proposition and strategy appear directionally unchanged, although more may develop in this regard following the recent promotion of Kariena (Zacharski) Greiten to the role of CEO for HealthHelp. Prior to this promotion, Greiten had been Chief Product Officer at Magellan Healthcare.

Transformation approach

The Co-Creation theme of the conference (and of WNS marketing) was expounded by WNS executives such as Adrian McKnight, EVP of Transformation and Quality, who said “We look to be a transformation partner rather than an outsourcing partner.”

WNS believes that perspectives on outsourcing are maturing. Initially, potential clients may consider outsourcing a piece of the value chain. But if they don’t begin with an end-to-end analysis of what the business could deliver to the end user, they begin to ask “What is beyond the KPIs of the outsourcing contract? What are the broader operating and business models required to facilitate the customer journey?” Then companies realize they are looking to buy transformation, not outsourcing. While outsourcing can be an aspect of a solution, it may not be the core requirement.

Domain expertise such as that which WNS offers through HealthHelp creates opportunities for WNS to take a seat at the table in discussions with clients on how to realize digital transformation. An intimate understanding of a healthcare payer’s organization helps immeasurably as WNS assesses the potential for transformation.

The iterations required to plan, build and implement client solutions rely on good collaborative practices, which, in turn, are founded on IT agile methodology. In WNS’ view, IT “agile” has matured to become a more holistic set of practices that integrate the functional needs of the client organization from all areas, not just IT. WNS claims to focus heavily on this broader view of the strategic position of its clients because culture and the speed of agility depend on this contextualized perspective. These eventually drive IT development projects and outsourcing contract requirements.

As WNS works through business problems with clients towards appropriate solutions, the ultimate success of WNS Co-Creation relies on the relevance and meaningfulness of its capabilities. Speed is also of primary significance. Whether those capabilities are supplied internally by the WNS enterprise or via its network of partners, WNS aspires to remove friction and increase the speed at which it can cycle through iterations, particularly in the implementation phase of a Co-Creation experience.

]]>

In this blog, I look at how NTT DATA worked with a large Blue Cross Blue Shield (BCBS) health insurance carrier to establish an enterprise governance structure for automation, and at the lessons learnt along the way.

Like many other large BCBS carriers, the company had piloted RPA initiatives, and from the somewhat frustrating results of these experiments, it had formed two conclusions:

- An IT department-driven center of excellence delivering bots will not achieve the full potential of automation

- Point solutions being driven within individual towers/business units are not scalable across the enterprise.

The company concluded that before it could proceed with its automation journey, it required an automation governance structure that aligned with the enterprise strategy. A business-driven (rather than IT-driven) deployment of RPA needed to coordinate the needs, requirements and deployment of RPA across the front, middle and back office functions, as well as shared and internal ancillary services.