Whilst ~130 people joined the ADP Innovation Day New York to hear updates on ADP product investments, I had an interesting conversation with CEO Maria Black in the corridor. We discussed why “big” matters and whether being the largest payroll provider in the world with 75 years’ experience really makes a difference. Arguably, the market may be tired of hearing about ADP’s size at every meeting. However, with rapid advances in AI-driven processes, the pure size of ADP alone is likely to offer it a very distinct advantage as it advances machine learning capabilities across its client and product bases. This is the first issue I wanted to explore at the ADP Innovation Day.

As well as its size, ADP is often considered conservative, placing great emphasis on security and having one of the strongest compliance and security frameworks in the industry. A challenge for the ADP product team is to reconcile how the security conscious organization can advance in an AI world where sensitive personal data including financial information is involved. I was curious to see how far ADP has come in its AI journey and where it is investing next.

The second question I wanted to explore is how far ADP has progressed in its journey to achieve the trifecta of offering Global Pay, Global Time and Global HCM. With its recent acquisition of WorkForce Software and launch of Lyric HCM, ADP is growing its capability to support this trifecta of offerings.

Below are my takeaways on AI, innovation and ADP’s global offerings.

ADP’s AI Vision

ADP designs AI-infused products to be Easy (transactions), Smart (with data insights) and Human (experience). AI is powered by ADP OneData and will be included in all key products, i.e. Global Payroll, Lyric HCM, Workforce Now, Workforce Management, ADP RUN, all at no additional cost.

ADP’s AI Assist assistant focuses on chat (e.g. employee questions on pay and pay compliance), insights (e.g. nudges, reporting) and actions (e.g. payroll anomalies). Going forward, AI workflows will evolve to agentic AI offerings. The new ADP Agent control center enables agent actions and scripts to be reviewed with full chat transcripts available. Special mention goes to the AI Feedback tool where users can elect for actions to be automatically repeated for similar cases as part of AI learning user preferences. AI Assist is also now available for payroll practitioners on mobile devices, for instance to highlight payroll anomalies.

The sign of a robust platform is managing errors when things go wrong. The feedback mechanism of ADP Assist has improved, as has user adoption and experience regarding accuracy and reporting on unanswered questions.

Innovation Approach

ADP is broadening its approach to innovation to support greater speed to market, and has introduced a Build/Buy/Partner and Invest approach. Traditionally, ADP focused on building proprietary software, but in 2025 there is a greater emphasis on the partner community as it scales up to support Lyric deployments. Its recent acquisition of WorkForce Software demonstrates ADP is taking a more flexible route to market. As part of its ADP Ventures initiative, a number of companies were introduced to the audience, including Nayya and Ema.

The ADP Marketplace has also been a source for innovation. With API Central, the marketplace options for integration offer greater ability to scale solutions. Flexspring is a partner organization that has been working with ADP to help build API data integrations, data caching and data governance. It supports API connections across multiple countries, the technology is already available in the U.K., Germany and France, and most recently Italy was added.

Global Product Offerings

Global Payroll: ADP processes 112m payslips in its ADP Global Payroll offering, representing 24% growth over the last 3 years. Its largest client in a single country has 108k employees. Highlights were the first wave of SAP clients on Global View migrating to Rise, representing 53 clients. Wave 2 is planned for 2025. ADP Assist for practitioners for payroll variances is also available, and coming soon are ADP Assist for employees and ADP Assist nudges. ADP Assist for legislative updates and data validation is planned for 2026.

Global HCM: Lyric HCM is ADP’s latest HCM product supporting organizations with 1k+ employees for both the U.S. and elsewhere: 243 clients have already taken up Lyric HCM across 38 countries, the largest client with 55k employees. Features updates include data conversion tools using AI for field mapping and position budgeting tools based on compensation data. Lyric customers were center stage to answer questions and confirmed they are using ADP Assist in pilot mode and also feeding back user questions to ADP to support its product development.

Global Time: Following the acquisition of WorkForce Software and its flagship product, the WorkForce Suite, ADP is consolidating its Workforce Management (WFM) offerings and embedding the WorkForce Suite in its strategic HCM platforms for the upmarket – Workforce Now, Lyric HCM and Global Payroll. As a result of the acquisition, the number of client employees served by ADP’s WFM solutions across all platforms grew +40% YoY to ~20M. The WorkForce Suite supports wage and hour rules in 100+ countries and is offered in 25+ languages. Other strategic products in the ADP WFM portfolio include ADP RUN Timekeeping plus Scheduling for small businesses, ADP Workforce Now WorkForce Management for the mid- to up-market and the ADP Kiosk device and ADP Time Kiosk app, to complement ADP’s traditional time clocks, mobile app and desktop solutions for user access.

Other product news: ADP announced a 10-year extension to its UKG agreement for licensing Workforce Manager to enable continued support to clients using the UKG product. It will stop selling UKG Workforce Manager in September 2026. eTime has a new end of life timeframe of September 2030.

WorkforceNow updates: This product supports +90K live clients with 15m client employees paid per month, with core capability covering continuous payroll calculation, anomaly detection, and compensation service offerings. AI is being applied to onboarding new clients. Plus, ADP Assist is already embedded in the product and will support new features such as quick searches, where searching through reports is no longer required, and an improved recruitment experience enabling cross-client talent pools, candidate CV feedback, and alternative job recommendations.

Predictions

- Expect more from ADP Assist: ADP has 67k employees serving 42m client employees across 140+ countries and territories and 14m users on the ADP app. With this size, expect ADP to drive ADP Assist through its platforms at pace, backed by the human in the loop as it validates responses offline with a strong compliance organization. ADP Assist will be the glue across the technologies, working cross-platform and will be multi-modal (voice/visual and text)

- As the ADP products’ user experiences merge, it is becoming harder to differentiate the products. Expect ADP products to expand up and down market as it consolidates its technologies

- Expect to see increased global time functionality filtering into global payroll dashboards, offering not just wage explanations but drill-downs to time data to address bottlenecks, anomalies, trends and data insights.

I recently attended the 2024 UKG Spring Analyst Day, the theme of which was helping organizations become a great place to work through human-centered technology. The event provided clear demonstrations of what the company has delivered as well as a preview of what’s to come. UKG also demonstrated an innovative approach to ensuring client value is at the heart of its product roadmap. Its focus on client value was greatly enhanced by the launch of its client community in 2023.

UKG shared its global perspective on how it designs and services its client base. With annual revenues of $4.31bn in FY2023, representing ~11% growth y/y, and supporting 80k customers across 160 countries, UKG is clearly a major player in the HR technology and services market. However, its size doesn’t detract from its focus on servicing SME, mid, and large market players, with a significant focus on listening to its customers to help design and shape a future-fit roadmap.

It measures customer ideas through its newly launched UKG community. Over the last year, it delivered 40% of the top 10 ideas voted for by customers on its UKG Pro platform, and 60% were delivered via the UKG Ready platform (see next section). Product manager time spent engaging directly with customers is clearly measured and reported to ensure all parts of the business are close to customer needs.

Investment in technology is happening at a fast pace. In 2023, UKG invested ~17% of its revenue in R&D. Over the last year, it reported that 370 new capabilities were delivered through its products. Further, as an early partner using Google Cloud's enterprise-grade GenAI and large language models (LLMs) through Vertex AI, it is progressing at speed, building new GenAI capabilities through its product suites with their UKG Bryte AI capability. UKG has ~100 data scientists, product managers, and engineers supporting AI solution development.

IP Investments & Platform Developments

UKG focuses its IP investments on two go-to-market HCM platforms:

- UKG Ready: for the SME market with less than 500 client employees, with Canadian payroll just added

- UKG Pro: for mid and large market organizations with more than 500 employees, also offered as a WFM/payroll standalone bundle with connectors to other HCM platforms where the large enterprise client might have another preferred HCM.

Within these platforms, WFM (UKG Pro WFM) and Global Payroll (UKG OneView) are offered as standalone products.

Key platform developments over the last 12 months include:

- OneView Global Payroll: through recently acquired Immedis (which has added 13 new wins), UKG can offer global payroll delivered using three models:

- Direct delivery, leveraging an existing client payroll partner where the client manages the process on the platform

- Managed payroll

- Connected, a single view with no services attached, where the management of the payroll process remains outside the platform.

- Bryte GenAI Experience: built as a suite of connected agents to remove friction and increase insights and guidance. UKG now has ~2.5k active AI models delivered across its suites, interacting with ~10m customer employees per month. Recent use cases include the UKG Talk Weekly Digest feature and configuration suggestions to simplify onboarding new customers

- UKG Flex: introduced UKG webhooks for real-time integrations (launched in April 2024) and its marketplace added 65 new solutions over 2023

- Benefits Hub: enabling new hires and open enrollment via mobile

- Great Place to Work (GPTW) Hub: leveraging data from UKG’s GPTW is core to delivering client value and actionable data insights. GPTW offers industry as well as client KPI trends, correlations, and recommendations

- UKG Pro Skill: the UKG Skills Recency Index supported by its new partnership with Lightcast offering detailed, actionable skills data that goes beyond proficiency and adds in a recency measure.

The key benefits clients derive from investments in the UKG platforms are the ability to:

- Bring modern, simple, and efficient experiences to their organizations, such as the manager hub and mobile life events

- Reduce manual data entry, such as integrating the onboarding experiences to share people's data

- Support global requests such as visibility and management of global payroll processes.

What’s Next?

UKG’s significant roadmap developments for 2024-2025 include:

- UKG Ready will soon be launched into the German market for SMEs. Expect additional European payrolls to be added in 2024

- GPTW light version coming to UKG Ready

- Contingent worker management features and functionality

- OneView payroll and ESS to be available through the UKG mobile app later in 2024

- Expanding the use of its Bryte AI framework and Flex platform across the UKG Pro platform

- Enabling workforce planning and strategic planning reviews that leverage skills capabilities and skill gaps, having recently announced its partnership with Lightcast in March 2024.

NelsonHall Perspective

UKG prides itself on making the “hard stuff simple”. It addresses some of the most challenging areas in HR, such as time and payroll for hourly workers, and it now offers this on a global scale. Uniquely, UKG is able to draw upon insights from its GPTW research globally. With these insights, its investments in AI through its product suite offer great potential to SMEs and mid- and large-sized organizations.

UKG’s products also offer significant potential for marketplace providers to “surface” where it counts. The UKG Bryte AI will increasingly be used to drive hyper-personalized experiences, enabling point solutions in its marketplace to be recommended based on individual needs.

Over the next few years, it will be interesting to follow how the AI insights offered in UKG Ready compare to that in UKG Pro. It is clear that UKG has the capability to deliver substantial insights to help clients develop future-proof workforce strategies as they grow from start-ups to mature organizations. The start of GPTW on the Ready platform will be the first step in this much anticipated journey.

]]>

ADP's annual global payroll customer event took place in London recently, bringing together 224 decision-makers from some of the world's largest companies, representing ~20m employees. The event featured a global economic update, ADP's strategic vision, and product development updates. The event also included a "round the world" experience sharing insights into local payroll nuances and topics.

Key highlights

Highlights from the event include:

- ADP Assist (announcement here), ADP’s GenAI solution, built by domain, clearly demonstrated how productivity gains can be made; e.g. a scenario where nudges indicate higher than normal levels of overtime and prompting emails to be sent to all relevant supervisors to validate overtime levels, with options to chose a tone of language that is casual, formal or shorter and more direct

- ADP Roll (announcement here), ADP's newest payroll product with chat-only features, demonstrated how work is changing, where only 3% of its users leverage a desktop and a whopping 97% process their payroll through mobile only

- ADP is enabling a workbook configuration within the ADP Global Payroll software

- Requirements for pay/gender (DEI legislation) and pay transparency are growing, and ADP DataCloud is looking to support these needs globally

- The buyer needs of a global payroll mobile app vary, but there were examples of how it is being used across Pay and Time in multiple countries; for instance, ADP client Principal uses the app to punch in/out through the etime product as well as being able to see payslips.

CEO Maria Black took the stage to share her priorities after one year in office. This is a milestone year as ADP celebrates 75 years in the industry and has been led by only seven CEOs. She shared how she sees the organization balancing its long history of stability alongside ongoing innovation. Maria focuses on the importance of "listening" to help drive the investments of products and services. For example, she has a practice of placing an empty chair in every room to represent the client in every meeting.

The ADP client base has a huge demand for new services and high expectations of ADP. Helping navigate global payroll needs in the complex global environment takes maturity, skill and a lot of listening. ADP is taking purposeful steps in its design decisions and looks to build lasting and innovative solutions.

What to look forward to from ADP's global payroll

Expect to see the following payroll developments from ADP:

- Marketplace developments will be growing on an international scale

- Variance check improvements

- Unified practitioner experience (ADP GlobalView and Celergo)

- ADP Integration Hub will be expanded to include both in and out activities, all in one place

- GlobalView and ADP Workforce Management will be integrated in 2024

- Benchmarking and payroll efficiency are coming

- ADP Roll will be expanded to Europe in 2024; this product is one to watch being one of the first GenAi- built and chat-only payroll products on the market

- An increase in the adoption of the ADP app across its customer base. With the addition of intelligent self-service prompts within the app, it will bring an elevated payroll experience, helping catch anomalies at source and once the ADP marketplace is expanded through the app, HR and payroll functions will be able to drive greater innovation and flexibility to support their workforces.

As we move into another year where salaries are not growing at the rates seen in previous years, payroll is becoming increasingly important for organizations. My point of view is that organizations should be looking to ensure their employees receive the best payroll experiences possible and should include this in how they measure employee experiences.

]]>

Last month, NelsonHall participated in the SD Worx Analyst Day, which included an update on key milestones since Kobe Verdonck took the reins as CEO in September 2019. The last three years have seen SD Worx supercharge its European growth and intensify its focus through achieving:

- Geographic expansion from 10 to 23 countries in Europe, where it utilizes its own IP in 17 of these

- Revenue growth from €768m to ~€1bn in gross revenue

- Customer growth from 70k to ~82k customers.

SD Worx has shared its vision for the next 5 years, keeping its course for pan-European growth through further targeting:

- Geographic expansion from 23 to 30 countries in Europe

- Revenue growth from ~€1bn to ~€2bn in gross revenue

- Customer growth from 82k to 100k customers.

To achieve this growth, SD Worx is looking to focus on the following key areas of differentiation:

- Integrated end-to-end HR solutions using the SD Worx, Gro, Flo or Pro service models

- SD Worx payroll software and subject matter expertise as the core method of delivery rather than using in-country partners

- Bringing local expertise, whereby in-country presence is core to its delivery model

- Consistent user experience, as all employees will have the same experience irrelevant of underlying software

- Aiming for a top 3 position in countries with a population >10m

- Being an employer of reference to attract talent.

SD Worx will look to support customers of all sizes and in all industries, locally and internationally.

However, as SD Worx actively drives payroll consolidation across the European HR and payroll market, one of its main challenges will be to establish the SD Worx brand and operational frameworks in its new markets.

Its aim of driving one experience across all platforms is ambitious, but with the client scale it is looking to achieve and through ongoing investments and acquisitions to support scale, this vision has strong promise. We can expect further acquisitions over the next five years to support its growth targets, in particular in Eastern and Southern Europe. This builds on recent acquisitions supporting the company’s expansion, including Integrho (Spain), Intelligo (Ireland), and HRPRO (The Balkans).

]]>

Last week marked Neeyamo's Payroll Beyond Borders' virtual global payroll industry event. The keynotes were delivered by payroll industry leaders Dan Maddux, Executive Director, American Payroll Association, and Ken Pullar, CEO, CIPP. The event had around 1,200 participants from around the world and was the first global coming together of global payroll industry experts since the start of the pandemic. As well as looking at the impact of the pandemic on payroll operations, there was also attention paid to how global payroll and agility is increasing in importance, reflecting changing priorities and the need to "meet the employee" where they want to work.

New Payroll Complexities Created by the Pandemic

The pandemic and related regulations or government subsidies meant new levels of complexity were introduced to payroll operations, complexities that needed to be handled without any delays. Payroll leaders highlight that payroll teams, both outsourced and in-house teams, should receive recognition for their efforts. The migration of staff to work-from-home locations put additional strains on payroll departments, both because of the associated risks and also the challenges in managing employment taxes in alternative payroll jurisdictions. Employees don't always feel the need to tell their employers where they are located if they are working remotely. Over the next year, some organizations may be facing the tax impact of changed employee locations retrospectively. The business continuity plans that were activated were not designed or expected to remain in place for months on end as lockdowns were extended.

The pandemic and the general ensuing migration to WFH has helped shift the employee/employer power dynamic in favor of the employee. Employers will increasingly need to meet their employees' requirements as to where they want to work and how they want to work if they are to keep talent. Payroll systems need to be agile to support additional payroll jurisdictions, and payroll managers should consider adding new processes to enable employees to include remote locations for recording their place of work.

Employers are advised to re-evaluate business continuity plans and payroll controls. This is a time to upgrade and improve business continuity by investing in more robust digital processes to enable payroll to continue flexibly. The pandemic has exposed significant manual processes based on outdated systems that need to be re-evaluated to keep the payroll running during times of crisis.

On-Demand Payroll Increasing in Significance

There has been a growth in on-demand payroll offerings, otherwise known as ESAS (employer salary advancement schemes), particularly in the U.S. and the U.K., which are the primary markets currently. The pandemic has helped accelerate this growth: in the last two years, more workers have had to contend with financial stresses caused by a combination of limited or zero savings, reduced income, and unforeseen emergencies. And as the cost of living continues to rise in most markets, this isn't going to get better any time soon. Even amongst workers with above median, secure incomes and a decent level of savings, a growing proportion has been facing problems with their financial budgeting, perhaps due to timing mismatches between income and major outgoings. The household debt-to-income ratio has been rising for years, and in the U.S. and U.K. is over 100. With the current war for talent, there has been an increased focus by organizations on employee retention and the employee experience – and this includes improving employees' financial wellbeing. It should go without saying that employees that are financially stressed are not going to be the most productive, healthy, safe, or loyal members of the workforce.

But there are major considerations to be taken into account by employers when considering introducing on-demand pay systems, among these:

- The potential impact on company cash flow, though this is not an issue for organizations that work with third-party ODP providers

- Providing employee education on the principle that having access to a proportion of their pay on an on-demand basis does not automatically lead to financial wellness. Placing restrictions on the frequency with which an employee can apply for on-demand pay might help employees in their debt management and/or financial budgeting to an extent

- The risks of exposing employee data to financial services companies who might push other loan products.

So which types of employees are more likely to be interested in on-demand pay solutions?

- Younger employees with little or no savings, who are also facing large one-off outgoings, and who are new to financial budgeting

- Part-time and temporary employees, who will continue to represent a growing proportion of the overall workforce in all geographies

- Industries like hospitality and industries that have a high proportion of hourly-paid workers, especially industries with significant amounts of overtime (not having to wait to the end of the month when you have done a lot of overtime and have an immediate financial need is a significant benefit)

- The public, healthcare, and education sectors, which are major employers.

There were some concerns about on-demand payroll expressed by payroll leaders at the event. Among these was a concern that, given many companies have spent decades moving employees away from weekly pay cycles to monthly (U.K.) or two-weekly (U.S.) cycles, and thereby reducing operational payroll costs, is going on-demand a backward move for both employer and employee? However, from the employee's perspective, having access to on-demand pay is likely to be an attractive element in a benefits package.

The pandemic has changed organizations' priorities in terms of their people and operations. And it has thoroughly tested the robust nature of payroll operations, to unprecedented levels. There was a general consensus at the event that there is a continuing need to prioritize agility and automation in global payroll operations.

Nobody should underestimate how essential payroll is, though putting money into the bank accounts of employees in an accurate and timely way is often a thankless task. Payroll processes need to be robust if they are to support new ways of working, and Neeyamo's event was a valuable way to discuss and test thought leadership ideas.

]]>

This past week, CloudPay announced the launch of CloudPay NOW, its latest offering focused on modernizing the way workers are paid globally.

The employer-integrated Earned Wage Access (EWA) solution is a key addition to CloudPay’s offering that pairs its unified database and technology-enabled operating model, with its deep global treasury capability to offer one of the most comprehensive end-to-end global pay solutions available in the marketplace.

How CloudPay NOW Works

CloudPay has enabled CloudPay NOW by leveraging a strategic acquisition it made very quietly in 2019 to boost its mobile payment technology. The solution integrates with CloudPay’s unified global payroll database, including workflow based on client payroll calendars, mobile technology, and its highly adopted global payroll treasury offering. The new offering can support EWA in 130+ countries and 168 global currencies. It further enables digital payments globally and in real-time leveraging established global payment RAILS.

The CloudPay NOW user experience is enabled through apps for both iOS and Android and provides employees with real-time access to earned wages for on-demand pay capability across the countries where CloudPay offers treasury support. Users are offered in-app support with chatbot and live chat options.

The benefit is cost-free for employees (employers are charged on a per employee per month basis) and provides them with early earned wage access, and real-time debit/credit card-based transfers to third parties, including person-to-person and person-to-entity. Because CloudPay NOW leverages a combination of credit and ACH RAILS, withdrawals can be performed in less than one hour, including on weekends, a much faster option than traditional bill payment solutions can provide. Transactions can also be scheduled for future dated payments and transfers based on automated target thresholds.

Further, the solution has been enabled with curated insights, guidance, and tools to support employee financial empowerment and wellbeing. Employers define set “business rules” within CloudPay NOW to guard and control employee access and withdrawals to ensure healthy usage of the capability. Employees can also adjust preferences (within client business rules) to support personal thresholds and limits.

The impact of CloudPay NOW

For employers, a globally unified payroll solution that goes beyond gross-to-net calculation to payroll funding and payment fulfillment offers real value for multinational firms supporting a global workforce. Traditional payroll solutions stop short of global payments, leaving employers to sort time-consuming money movement and foreign exchange complexities, often extending the pay cycle and timeframes for payments to reach employees.

With payroll at the heart of the employee experience, employers across sectors seek more ways to compete for top talent by providing differentiated experiences. On-demand pay breaks down lengthy pay cycles, and empowers employees to control the timing of their pay, boosts financial wellness, and offers them personalization to meet their unique financial needs (e.g., remittance to family members) and aspirations. Early adopters of employer-integrated EWA have seen measurable and impactful results beyond simply driving up direct deposit and digital payment adoption, with positive impacts on talent attraction, hiring, retention, and engagement resulting from deploying the benefit.

To date, EWA solutions have been most available and adopted amongst U.S.-based employers and employees, with limited solution options internationally. With CloudPay NOW, multinational employers can offer the benefit of an on-demand payment solution to all of their employees globally, something other EWA solutions have failed to provide, as they are often enabled for a single country, or a few at most.

It empowers employees with control to determine how and, more importantly, when their earned wages are distributed. Payroll processing has long favored the employer with lengthy pay cycles, forcing employees to wait as much as a month for their earned pay. Meanwhile, their lives and financial needs are occurring in real-time, often leaving workers to tap risky alternatives to address unplanned expenses.

CloudPay NOW provides employees with a tool that converges their pay with day-to-day life in real-time and provides tools to support money access and transfers, with insights to make more informed decisions with their earnings to reduce debt, advance savings, or navigate financial challenges as and when they occur.

The future for CloudPay NOW

The launch of CloudPay NOW is well-timed, given the groundswell of momentum building around digital payment solutions and their adoption. With digital payment adoption rising globally and mobile-first experiences fueling consumer expectations for on-demand experiences, the convergence of payroll with these factors has made employer-integrated earned wage access a standard element in modern payroll solutions. Further, in the environment of COVID-19, many firms learned just how challenging yet vital and impactful the ability to move earned wages to employees in a timely fashion can be – particularly those operating with multi-country footprints. Building resilient global payroll operations will require adopting modern digital capabilities like CloudPay NOW and its underlying treasury capability.

With clients now more commonly looking for their payroll vendors to provide treasury services as part of their managed payroll services arrangements, but not all vendors actively offering global treasury support, CloudPay is particularly well positioned to leverage its offerings synergies to boost adoption; its treasury service alone has been adopted by ~90% of its client base and continues to see similar uptake in new deals.

Looking ahead, CloudPay plans to add a digital wallet capability, including a branded pay card solution and is actively advancing its employee wellness support with expanded budgeting and planning tools. The solution is also enabled for (and has a selection of) non-profit relationships (which it continues to curate) for enabling philanthropic donations by users through their earned wages. It is also in-flight with FCA certification, which it expects to complete next year.

CloudPay will also seek to leverage CloudPay NOW to drive additional recurring revenues. Longer-term, it sees CloudPay NOW as a standalone offering that could begin popping up in vendor marketplaces through integrated partnerships and white label opportunities for reselling the offering. Its in-country payroll partner network will be engaged first, with broader market providers in focus next.

CloudPay NOW already has a sizeable, multinational brand/employer piloting the capability to support 6k employees across 24 entities and 15 countries by the end of summer. The solution is expected to be well adopted by its client base, particularly those firms operating in challenging sectors with high hourly worker populations.

The addition of CloudPay NOW to CloudPay’s global payroll offering provides a unique synergy to drive adoption for its complete offering amongst new buyers. Additionally, it elevates its value proposition considerably amongst buyers of global payroll services, providing it with a differentiated, end-to-end offering that pairs payroll technology and services, global treasury, and global payments within a single vendor solution.

This is the final part of a three-part blog series covering my perspectives on the payroll market based on NelsonHall’s latest annual market analysis, Payroll Services: Globalization and Digitalization. Part One features the payroll buyer perspective, with Part Two looking at the managed payroll service providers currently pushing the pace of innovation. Here I focus on the outlook for the managed payroll services market and what to expect as we move forward.

Managed payroll services adoption

The appetite for managed payroll services remains healthy, and the market looks to rebound to its pre-COVID growth rates over the next three to five years, as digital payroll transformation projects are accelerating and firms seek to modernize this critical process for greater continuity, resiliency, and strategic value. And this is particularly true as payroll buyers more commonly require support from managed service providers in undertaking large-scale payroll transformation initiatives.

The mid-market buyer will remain the largest adopter of managed payroll services globally, while large/enterprise-sized, late adopters of cloud-based core HR platforms will increasingly seek to extend cloud investments with integrated modern global payroll solutions. Small market firms are more commonly seeking payroll services as a core component in broader HCM technology and services solutions and are increasingly finding their footprints creeping to new international markets and require support for multi-country payrolls.

While single country adoption is steady, multi-country service adoption will continue to outpace single country deals by as much as 5x, as firms of all sizes and sectors will continue to see their footprints pulled to new countries of operation, particularly as 'work from anywhere' continues to trend upward, and talent is sourced from new locations. With providers now capable of supporting >150 countries through a single platform, UX, and a tightly integrated operating model – and with the need to modernize and consolidate multi-country payrolls – achieving global payroll transformation through a single vendor solution is more possible than ever.

From a scope perspective, fully managed payroll service adoption will continue to outpace partial services as firms seek to tap into the digital technology vendors have been proliferating in recent years, urging buyers to focus on payroll resiliency (cloud platforms, mobile-first design, on-demand payroll capability, predictive analytics, and dynamic, real-time integrations to bring it together seamlessly).

Additionally, firms operating in fully managed payroll services models during the pandemic had much-needed help in quickly accessing reliable data, interpreting, responding to compliance directives and government support programs, and fundamentally fared better in navigating the unforeseen challenges – further reinforcing the value in managed payroll service engagements. With compliance intensifying and payroll complexity escalating, buyers are keen to adopt fully managed payroll solutions to access best-in-class operating models, vendor advisory in de-risking the critical process, and supporting future growth and scale as requirements change.

Service offerings

The renewed focus, investment, and emphasis on payroll as a critical and core element in the employee experience have created a boom of opportunity for payroll solution providers. Recent years have seen more new technology-driven entrants and pulled some (e.g., HCM tech providers) deeper into the payroll space, crowding the market with many options.

Thus, vendors are commonly differentiating their solutions through the employee and client experiences, providing a modern UI/UX, mobile-first design, augmented and personalized support through AI/ML, and analytic insights – all of which is underpinned by a high-touch client experience that focuses on increasing client value by enabling improved payroll outcomes and driving long-term recurring revenue retention.

With buyers focused on cost containment and often varying in their maturity to digest and manage change programs globally, vendors are creating more flexibility for buyers by unpacking solutions to enable more standalone service levels and tiered service options – thus enabling incremental service adoption to accommodate unique buyer requirements, budget constraints, and appetite for change within the organization.

Vendors are also increasingly offering pre-configured, platform-based software and services solutions for smaller/midsized multi-national firms seeking modern, compliant 'core' payroll and HR capabilities to support long-tail footprints, enabling a turnkey multi-country core HR and payroll solution that can be rapidly deployed.

Lastly, service offerings are expanding to include add-on services to meet buyer requirements and drive increased revenue retention; the top three service additions include treasury and funding services, HR compliance support, and global mobility support and advisory.

Enabling technology

With buyers keenly focused on the employee experience and seeking to align and integrate payroll with their broader HCM tech investments and tap into modern payroll solutions, vendors are focused on advancing and differentiating their UI/UX with roadmaps focused on deeper digital capabilities, including mobile-first design, predictive analytics, and intelligent automation. Modern payroll platforms are now providing practitioners with a single, globally consolidated, real-time view of payroll processing, providing deep transparency, insights, and control over their payroll operations globally.

Providers are also focused on touchless and autonomous payroll enablement – advancing platform automation through RPA, AI/ML/NLP to remove manual, repetitive tasks, detect and address anomalies and data errors in real-time, producing more reliable payroll outcomes (timely, accurate, compliant) while enabling payroll practitioners to focus on value-added analysis and strategic projects and tasks. With payroll holding some of the richest and least utilized data sets in the organization, accessing and leveraging reliable, real-time, globally consolidated payroll insights will be key to payroll pivoting from simple processor to strategic COE and business advisor. Thus vendors are advancing payroll reporting capabilities through real-time analytic reporting, benchmarking, and guided, predictive insights.

Lastly, payroll vendors are increasingly advancing their partnerships to supplement offerings and capabilities, fill white spaces, and offer clients solutions to meet their unique needs through integrated third-party solutions. While formal payroll marketplaces are still somewhat emerging and primarily existent within the HCM technology space, they will become a standard longer-term offering with certified, pre-built integrations to leading HCM technology platforms and a broad range of complementing third-party solutions.

Key integrated third-party solutions increasing in demand and adoption include certified HCM technology integration and partnerships, as firms seek to tightly integrate payroll (globally) with their core HR investments, followed by earned wage access (on-demand payroll) and integrated workforce management.

Although on-demand payroll solutions are largely trending and adopted most by North American-based firms and workers (due to various social and economic factors), demand is gradually increasing globally and will be a standard offering requirement longer term. While most payroll providers have partnered with fintech firms to offer the capability, look for more payroll providers to enable native on-demand pay solutions as we move ahead.

You can read the rest of this blog series here: Part One, Part Two.

]]>

NelsonHall has published its annual payroll services market analysis, Payroll Services: Globalization and Digitalization. The report includes an analysis of two dozen payroll vendors, their offerings, and their buyers' perspectives. The project provided 'behind the curtain' access to many of the major payroll solutions enabling the market today and shaping its path forward.

This blog is a three-part series of my observations from the project and thoughts on what to expect for the payroll services space as we move ahead. Part One features the payroll buyer perspective, including the buyer view of the impact of innovation available today. Part Two continues with a look at the managed payroll service providers pushing the pace of innovation. Finally, Part Three will focus on my perspective on the managed payroll services market's outlook and what to expect as we move forward.

Managed payroll services: buyer perspectives

The past year has seen a renewed interest in payroll as a key transformational area of opportunity for firms across sectors. While many have focused investments and initiatives in recent years toward cloud HR adoption and advancing talent management capabilities, payroll remained somewhat overlooked.

Fast forward to 2021 and payroll is squarely at the heart of the employee experience, with firms realizing that payroll is far more complex, vulnerable, and desperately in need of modern tools to increase efficiency, resiliency and enable the critical process to better support the strategic direction of the business.

85% of buyers interviewed confirmed that payroll transformation was either underway or planned over the next two years for their organizations, with nearly all citing the need for support from managed service providers as they lacked the ability to undertake the transformation alone. With payroll transformation and digitalization in focus and front of mind for buyers, vendor selection criteria (amongst single and multi-country adopters), centered on vendors that can offer proven expertise and qualifications for the countries in scope and enable digital payroll transformation through an affordable platform-based offering.

What has gone well

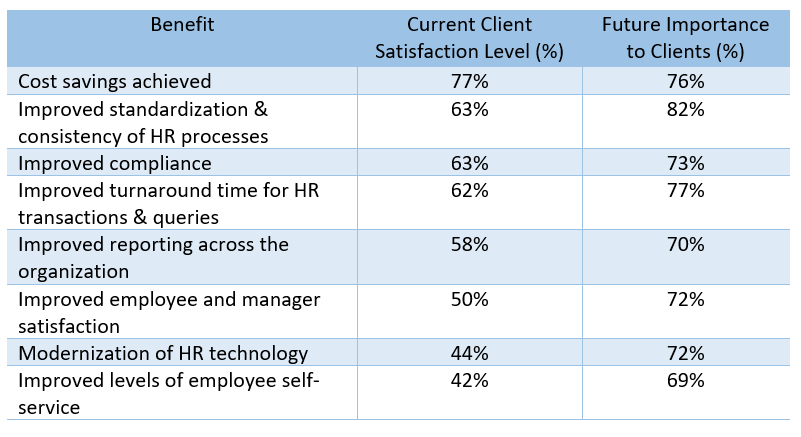

Collectively, buyers pointed to positive overall satisfaction for their managed payroll services and vendor relationships and further indicated a positive outlook for their solutions to meet their strategic needs over the coming three to five years.

With the marketplace crowded and differentiation often coming by way of the user and client experience, vendors are underpinning offerings with a high-touch, localized expertise that focuses on enabling value for the client and driving long-term recurring revenue retention. Buyers showed high satisfaction with their vendors, specifically pointing to the strength of partnership, flexibility, and caliber of personnel as the top aspects of their relationships.

Further, in recent years, vendors have loosened adoption requirements, unpacking offerings to provide more incremental service options, and filling gaps through integrated partner solutions to meet the unique needs of buyers across sectors and sizes – with buyers pointing to a positive outlook and confidence that their solutions can still meet their strategic needs longer-term.

What can be improved

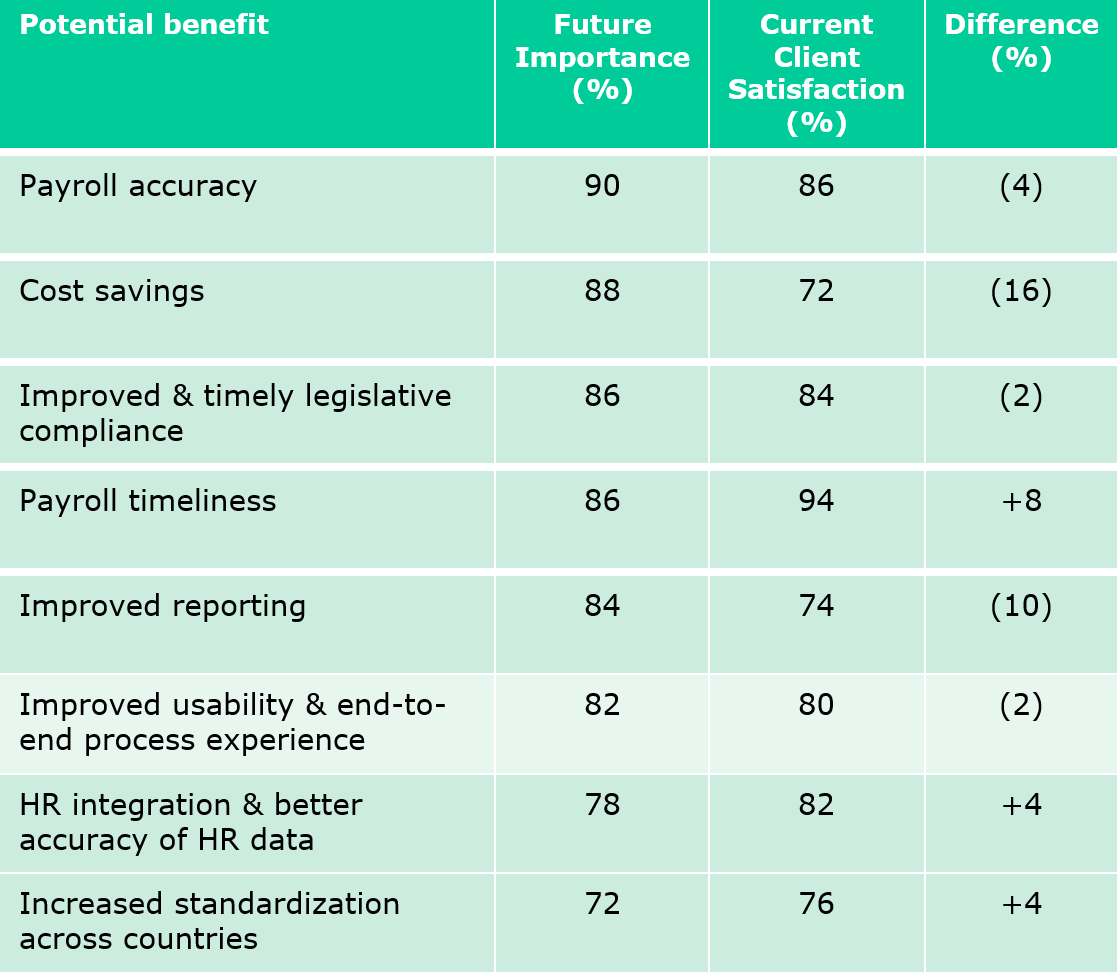

Despite the innovations of recent years and the work both buyers and providers have done, there is room for improvement. Most notable this year was the appetite for digital enablers to transform payroll, yet commonly buyers were somewhat unclear as to what their provider offered in this regard.

With AI/ML still maturing in the payroll space, many solutions still lack an intelligent technology infusion, with the highest maturity and satisfaction seen amongst the HCM tech platform providers offering managed payroll services. However, buyers commonly lacked understanding of how intelligent technology (AI/ML) can help them automate the complex process, as buyers were often unsure if it was present in their solutions or even offered by their vendors.

Further, two critical components required of modern payroll operations that are surprisingly lacking in meeting buyer expectations center on integration and reporting. Like many aspects of managed payroll solutions, not all integration capability is equal and must be thoroughly vetted and tested – deploying any solution lacking seamless integration (both in-platform and to/from the platform) will negatively impact the user experience and reporting, as it prevents data from flowing freely across the operating model, and amongst key systems. Specifically:

- Integrations: 40% of buyers indicated not using, not needing, or didn't know if their vendor offered integrations to third-party platforms, with about half of those respondents indicating a need to integrate those systems in the future, including core HR in select cases (often a decision by the business to hold off on core HR integration for undisclosed reasons)

- Reporting: Overall, a mixed satisfaction levels; lower-scoring satisfaction was driven by a lack of maturity in the offering or capability, e.g., only offering Excel-based reports or "basic functionality" lacking in analytic insights, visualizations, or graphical representation. In select cases, buyers choose to conduct payroll reporting outside of vendor solutions, likely leveraging third-party reporting tools or platforms to supplement the lack of vendor capability.

Further, buyers pointed to a clear opportunity for vendors to support them with process reimagination of payroll service and processes. Those citing lower satisfaction pointed to a lack of proactive engagement by their vendors for continuous process improvement. While technology innovation has undoubtedly helped, more can be done to engage buyers with new solutions, tools, and methods for addressing their unique requirements. As with the feedback on digital enablers, there is also a gap in buyer understanding of what vendors can offer and what is possible in terms of payroll transformation and process reimagination.

Vendor opportunities

Buyer lack of strategy or change management plan

In reviewing feedback from both vendors and buyers, there is a clear gap in payroll transformation strategy that puts both parties in a poor position from the start, particularly for multinational firms seeking to enable global payroll transformation. Buyers are often setting out to transform payroll with a limited or no strategic plan, assuming that adopting a particular solution or vendor model will instantly transform payroll. While this can certainly move the payroll operating model forward, it must be accompanied by a clear strategic path and underpinned by a comprehensive change management plan. I often see buyers deploy the latest solutions (across HR towers) without doing the uncomfortable work of shifting habits and adopting the solution's full potential, only to find that they didn't transform after all.

While payroll vendors have expanded offerings in recent years to include front-end advisory and business case support, change management is often a key element lacking and generally isn't a core competency or service offered by payroll providers. This is an area I think vendors have to do better in supporting buyers, as it benefits both parties over the long term.

Process reimagination and innovation

A key area of opportunity that resonated across buyers and was evident amongst vendors across geographies and solutions was the absence of ongoing, proactive process improvement and service reimagination. Buyers commonly pointed to an appetite for deeper proactive engagement and consultation by their vendor post go-live. Capabilities like design thinking and proactive outreach to introduce and incorporate new innovations and tools into client programs are lacking. Many buyers simply didn't understand what their vendors could offer or how it could be leveraged to meet their specific needs and maximize the value of the relationship.

Payroll service providers can look to HCM technology providers as a model for how this can be improved. The HCM technology firms do an excellent job of staying closely and deeply engaged with their user community, assessing their engagement, satisfaction, and monitoring usage of their systems to proactively help clients maximize the value of their investments and drive the transformation they seek.

They also do a great job of enabling communication channels between vendor and client as well as client to client. This open collaboration leads to the platform community driving its future through steady user feedback, thereby shaping significant portions of the roadmap and enabling direct impact for users for the challenges they face daily; further solidifying the partnership; boosting the investment in the success of the platform for all parties; and driving long-term recurring revenues.

Part Two continues with a look at the managed payroll service providers pushing the pace of innovation.

]]>

Part 1 by Pete Tiliakos & Liz Rennie

This is Part 1 of a 2-part blog presenting an analysis of key trends from NelsonHall's HR Technology & Services team. Part 1 looks at the key outsourcing trends around core HR functions, including cloud HR transformation, payroll, and benefits administration services.

Cloud HR Transformation Services

The drive to digital has kept many cloud HR transformation projects on track, despite some large enterprise signings being delayed. The 2020+ HR challenges look different from those in 2019, with organizational challenges related to workforce safety, workforce productivity, security, cost containment alongside deepening cost pressures, and a need to ensure all processes are digital. Pivotal to success is the agility of HR organizations to drive restructures supporting significant market upheavals across so many industries. Adapting to rapidly changing and compliance needs will also be a challenge.

Cloud HR transformation services are adjusting to a FluidWorkLife era, defined by greater people engagement to support fluid, individual work and homelife needs in a consumer-like way – while addressing higher-speed digital deployment through improved use of automation and technology to better manage the pace of business change and industry consolidation.

Outlook:

Key themes and drivers expected from the Cloud HR Transformation Services market in 2021+ include:

- Managing workforce restructuring and HR & payroll compliance: with unprecedented layoffs and furloughs, in contrast to significant growth in industries such as online shipping, couriers, and communications, HR has played a key role in supporting the business through change. Ensuring timely, accurate, compliant payroll was the top operational priority in 2020 and will remain critical moving ahead

- Workplace tools to support workplace change: with employees working from home, a greater focus on worker tracking to support a safe return to work, enabling touchless workplace services, monitoring social distancing interactions, and supporting contact tracing

- Effective employee engagement is table stakes: employees will have diverse needs and individual personal demands, requiring greater HR flexibility, including where employee solutions might need to be co-created. Enabling tools such as HR chat to support improved engagement will increase in importance, plus more regular employee surveys or pulse-checks

- Security is increasingly important, with more cyber-attacks evident during 2020

- Greater resilience through cost improvements, digital processes, and agility are also key to HR delivery models. Priorities are expected to focus on solutions that help make workforces more resilient, including employee health, voluntary benefits, risk, and cost. Companies will be looking for greater agility for changing business needs. In the light of COVID-related revenue and cash flow challenges across many industries, it is expected there will be a greater focus on delivering longer-term cost improvements.

Payroll Services

This past year has been a stark wake-up call for many organizations and their payroll operations. The effects of the pandemic strained and exposed operating models up and down market, leaving many firms across sectors realizing investments to futureproof payroll operations for greater resiliency can no longer wait.

At the same time, 2020 has been payroll's 'time to shine', with practitioners stepping up to answer the call and keeping workers around the globe paid on time and accurately during arguably one of the most challenging times in recent history, despite the shortfalls in capability.

On the managed services front, the shift to work from home enabled payroll providers to put their digital technologies to the test, proving out the very solutions they had been proliferating in recent years and urging buyers to focus on: cloud platform adoption, mobile-first design, on-demand payroll capability, predictive analytics, and dynamic integrations that bring it all together seamlessly. Additionally, firms operating in managed payroll services arrangements had much-needed help in quickly accessing reliable data, interpreting and responding to compliance directives and government support programs, and they fundamentally fared better in navigating the unforeseen challenges, reinforcing the value in managed payroll services.

Outlook:

While payroll service provider revenues were negatively impacted by the global economic downturn and subsequent job losses, and buying decisions were put on hold, the appetite for digital payroll solutions and managed services is quite healthy and is escalating as we move into 2021.

With payroll a critical, core element in the employee experience, global footprints creeping, and compliance risks rapidly intensifying, buyers are keenly focused on payroll as a key area of investment moving ahead, and thus service provider pipelines are healthy, signaling a gradual return to the growth levels experienced before the pandemic.

Five key themes and drivers expected from the managed payroll services market in 2021+ include:

- Compliance is THE priority: quite possibly the leading driver for managed payroll services adoption today and one that will intensify as we move forward; buyers will focus on tapping into the tools, localizations, expertise, and global capability that vendors can offer at scale in removing risk and ensuring complete and timely compliance as statutory requirements evolve

- Digitalization up and down the process: no process in the employee lifecycle has been historically more neglected or overlooked than payroll. Vendors will continue leveraging cloud platforms as the launchpad to enabling deeper digital capabilities with a heavy emphasis on automating the highly manual process through RPA, AI, and ML infusion, inching toward eventual fully autonomous processing. With payroll sitting squarely at the heart of the employee experience and wellness, look for deeper mobile capabilities, expanded use cases for AI/ML, and NLP-enabled virtual assistants that augment users and personalize experiences with guided, predictive insights to drive best practice and data-driven decision making

- On-demand earned wage access will be a game-changer for payroll: if the pandemic taught us anything, it's just how vital and impactful the ability to move earned wages to employees in a timely fashion can be. With the employee experience, engagement, and wellness top of mind for HR leaders, on-demand payroll capability helps with each by empowering employees with greater control and insight over their earnings. Look for the solution to continue its hypergrowth trajectory with adoption led by the U.S. and Canada, but increasing slowly internationally

- Payroll becomes a strategic partner: payroll has long been viewed as a simple processor and cost center, often overlooked in key HR decision-making or strategic decisions. Yet payroll controls one of the most critical processes in the employee lifecycle and houses some of the most underutilized and generally misunderstood data sets in the entire organization. With the continued proliferation and criticality of globally consolidated predictive analytics, and benchmarking capabilities, pared with the advancements in digitalization, payroll has the opportunity to truly shift its focus toward becoming a strategic advisor to the business

- Multi-country deals will escalate: with many MNCs operating on legacy, disparate, and often poorly integrated payroll solutions globally, the appetite for consolidating and modernizing global payroll remains strong, particularly with many firms finding their global operating models ill-equipped to handle the next major disruption. With multi-country payroll solutions able to support 100+ countries on average, look for buyers to tap into vendor offerings that can consolidate, digitalize, and automate payroll globally through a single solution.

Benefits Administration Services

Benefits administration providers have continued to focus on expanding benefits offerings to tailor to specific needs, while also minimizing administration by improving processes and technology. Significant changes in the way of working have also impacted the industry. Over 2020, benefits fairs were managed online, a first for many. As a result of the pandemic, technology is the driving force to innovation, with greater focus on homegrown platforms or through managed acquisition and tighter partnerships to support ongoing changing needs and client needs for greater visibility of data.

Buyers of benefits programs continue to expect greater flexibility to support change, greater automation, customizations of communications, and improved process efficiencies.

As government relief packages introduced by most major governments greatly impacted health provision and benefits rules, operations had to adapt quickly to apply these changes. As a result, 2020 was a year of increased operational costs for many benefits administrators.

Outlook:

Key themes and drivers expected from the Benefits Administration Services market in 2021+ include:

- Automation and integration: benefits operations will become more streamlined with greater integrations, minimizing risk and manual interventions

- Health costs are increasing in the medium to long term: costs might have reduced in 2020 due to a lower number of medical claims; a high-cost spike is expected in 2021 due to pent up demand for health services

- Keeping up with relief legislation has been challenging, and more changes are expected in 2021: The dynamic nature of the benefits markets will mean more buyers will look to expert providers for guidance and support and bringing greater agility to support compliance

- Compliance, security, and risk management will have growing importance: especially while more processes moved online and electronically, and as companies capture more data about their employees

- Personalization through AI will grow alongside company ethics and brand as it relates to benefits design. AI will increasingly support benefit recommendation engines; personalization will also increase through more fine-tuned communication tools

- Benefit design will have a growing importance in promoting diversity in workplaces and representing the company brand

- Benefits professionals’ roles will change to become more marketeers to communicate benefit programs and be less about interface/error management and processing

- Industrializing and institutionalizing analytics: increasing use of data to support and evaluate program success, employee engagement, cost management, and drive more informed decision making.

In Part 2, Nikki Edwards will look at trends and the outlook for talent management services, including recruitment and learning services.

]]>

Like many HR service providers, SD Worx has been supporting its clients over the last six months by continually making updates to the changing legislation and dealing with client queries and operational challenges. SD Worx also launched a study to better understand changing market needs, the findings of which have just been published. The SD Worx study was one of the most extensive European HR COVID impact surveys, across 20 industries and 3,000 companies from 11 European countries, and it found that the highest HR priorities in 2020 are operational, administrative tasks. As part of its thought leadership white papers, SD Worx has also set out a new vision for HR, to enable clients to balance “Stability” and “Fluidity”.

Key study findings

The study confirms HR’s top priority in 2020 was payroll. When asked, “What priorities or projects do you have (or plan to have) within payroll and HR?” the option “To ensure smooth, efficient payroll calculation and payment” scored the highest (#1 priority for 8 out of 11 countries) across 19 different options covering all aspects of HR. Payroll has never been more valued than in times of crisis; payroll administrators are “essential workers”.

So, when will things get back to normal? Nearly half of European companies surveyed were convinced that COVID-19 would have a lasting impact on their business. We will have to radically change the way we work (together) after the crisis. However, the HR study finds that HR directors rate their level of digital maturity as low: only 37% of surveyed organizations claim to have reached a high level of digital HR maturity. So, as many lives and business models have been disrupted, HR agility has never been more important.

The SD Worx study showed that the top three areas companies look at to leverage external specialists and outsource service providers are:

- HR process automation

- Regulation expertise

- Digital transformation.

Other insights from the study demonstrate that besides payroll and HR services and performance, many European country priorities were as diverse as they are homogenous, something seasoned European HR directors are not unfamiliar with. As well as reflecting cultural priorities that might result in different priorities, NelsonHall expect the variations also be partially due to the timing of the different countries' COVID responses. The study was conducted over the month of June 2020 and during this month, many European countries were at a different stage of their COVID19 responses. The impact of the crisis was just starting to be understood and realized. According to most countries surveyed, the three areas that were the lowest priority were HR policy, reward, and contingent workforce.

Employee experience has been a common theme of many HR strategies over the last few years, and many still aim to optimize the employee experience better. With so many employees now working remotely, the employee experience and employee engagement are more critical than ever before and require modern technology to keep employees connected while ensuring timely, accurate, real-time information, and facilitating reliable outcomes throughout the HR delivery model. The SD Worx study showed ~60% of employers are still actively trying to improve the employee experience, either with existing projects or projects planned over the next 12 months. SD Worx defines employee experience as the digital workplace experience and cultural & inter-personal engagement as well as the physical work environment. SD Worx recognizes a trend towards more personalization in HR, with almost half of companies having “flex reward projects” in progress or planned within the next 12 months.

SD Worx response

In response to the HR study, to meet European countries' needs across such a wide range of industries, SD Worx set out its HR service vision. Its vision is to bring stability to HR services alongside a fluid offering, enabling each company to find its own optimal balance. The concepts of stability and fluidity are outlined below as well as some examples of how SD Worx addresses these:

Stability is defined by SD Worx as:

- Future-proof HR tech: SD Worx offers cloud-based HR/payroll technology offerings in the core markets of the U.K., Ireland, Benelux, France, Germany, Austria, and Switzerland

- Efficient HR processes; SD Worx recently developed its HR SME digital services platform “SD Worx Buddy”, piloted in Q2 2020 in Belgium. Frictionless tools: SD Worx launched its mySDWorx app for absence, expenses, payslip, internal communications, and a FAQ for HR. It has over 160K installations It uses machine learning to determine the ten most asked questions and is tailored to the client's database. It supports conversations designed for the employees (not for the process). Over 2019 it has rolled out an onboarding assistant to capture more employee data; now released in Belgium and UK, and the next country onboarding to be developed is Germany.

Fluidity is defined by SD Worx as:

- Personalization: SD Worx enables personalized remuneration packages through its reward cloud platform. This lets employees tailor their reward components with voluntary elements. Helping employees to value their rewards can not only boost motivation but also complement a cost-efficient overall reward policy

- Empowerment: SD Worx empowers organizations to be proactive and adapt to fluctuations in the workloads through its workforce planning offerings. It takes each employee’s qualifications, availability, seniority and other requirements into account which could be fulfilled by permanent or flexible staff, through the SD Worx Flexible Staffing solutions

- Autonomy: SD Worx solutions support personalized training trajectories, enabling organizations to boost employee engagement, performance and giving them greater autonomy.

For those who want to get more in depth insights on the research, SD Worx is creating a series of publications that will be published on the SD Worx platform (link). These are the first:

- Payroll: highly valued, hardly optimized

- HR, fluid as Hula-Hoop shaking (publication end of October, webinar at Unleash)

Also foreseen are ebooks on Workforce management and on Digital HR and Employee Experience.

The themes of SD Worx’s vision align well with the benefits Cloud HR transformation buyers look to achieve, according to NelsonHall’s Cloud HR Transformation Services market analysis report. According to the NelsonHall report, the top three were improved compliance, simplified and modernized technology, and improved employee experience. In 2020 and following the pandemic, it is evident that improving employee experience as an HR objective is not disappearing. Its definition and the height of the bar is being raised, moving beyond the realm of just a mobile app offering, as vendors strive to deliver more frictionless and efficient offerings.

]]>

Since its IPO in early 2018, Ceridian has remained focused on reaching its goal of achieving $1bn in revenues. A key pillar of its growth strategy toward achieving that goal is the continued adoption of its Dayforce HCM platform by large multi-national buyers across key verticals, and expanding its adoption globally by enabling and offering integrated core HR, workforce management, payroll, and talent management to targeted countries, particularly the U.K. and Australia (which both helped it achieve 150% y/y growth outside of North America in FY’19).

To that end, Ceridian set out to expand its native global payroll capability, targeting ~20 countries over the next few years, and has quickly enabled Dayforce to support seven countries: U.S., Canada, U.K., Ireland, Australia, New Zealand, and Mauritius. Today, it supports nearly 4m users across >60 countries and this is growing rapidly.

Ceridian’s global payroll capability received a huge boost last month when it announced it would acquire Singapore-based Excelity Global, a leading APJ-focused HCM technology and managed services provider producing ~1.2m pay-slips monthly. The move now positions Ceridian as one of the largest and most capable HCM technology and services providers in the APJ region.

Further, with its September 2019 acquisition of APJ-based workforce management solution provider RITEQ, Ceridian now has a highly competitive, combined core HR, WFM, payroll, and talent offering, specifically localized for the APJ region.

Excelity’s impact on Ceridian’s capability

Not only does Excelity bring with it a proprietary cloud technology localized across 13 major countries in APJ, but it also brings a strong managed service offering, expertise, and delivery presence in the region supported by six primary centers, a key differentiator over other firms Ceridian evaluated.

From a technology perspective, Excelity has cultivated a strong proprietary native payroll capability and recently launched an HCM technology offering in 2019, including:

- EPay: PaaS payroll solution targeted to employers with >500 employees and configured for gross-to-net calculation in 13 countries (Australia, China, India, Indonesia, Japan, Hong Kong, South Korea, Philippines, Malaysia, New Zealand, Singapore, Thailand, and Taiwan)

- Ezpayroll: SaaS payroll solution targeted to employers with <500 employees and configured for gross-to-net calculation in 12 APJ countries (Australia, China, India, Indonesia, Japan, Philippines, Malaysia, New Zealand, Singapore, Thailand, Taiwan, and Vietnam). As well as an integrated third-party digital wallet through its GCash partnership in the Philippines

- Excelity HCM: cloud-based integrated HCM platform technology.

It also brings a well-adopted managed payroll services offering that currently supports >300 clients with operations in multiple countries across the APJ region, including several notable brands such as Forbes, Volvo, Uber, and Mondelez, enabled by an in-region delivery footprint and capability that spans five countries (India, China, Singapore, Malaysia, and the Philippines), a key factor in supporting Dayforce’s continued adoption in the APJ region, and boosting Ceridian’s global presence.

The combined organization’s global footprint significantly enhances Ceridian’s “follow the sun” capability in support of service delivery, as well as its further development and innovation of future HCM technology.

Ceridian’s outlook

With the Excelity deal now closed, Ceridian has begun the process of merging and integrating the two organizations and capabilities, which is always the top challenge to any acquisition, particularly with two organizations at opposite ends of the globe.

While Ceridian doesn’t have a deep history of acquiring its capabilities, the complementary nature of the Dayforce HCM platform, combined with the strength of Excelity’s APJ experience and capability, should fit nicely, boosting its product offering, targeting, and adoption by firms in the region, as well as among North American and European based multi-national firms with operations in the APJ region.

A key decision for Ceridian will be deciding how to best leverage the additional technology Excelity brings. Will it be necessary to keep both Epay and Ezpayroll? And what becomes of Excelity HCM now that Dayforce is the parent flagship HCM platform (particularly as it seeks to shift Excelity’s client base to Dayforce)?

Ceridian plans to immediately leverage its global connectors to bring the Dayforce HCM platform and Excelity’s payroll technology together, en route to an eventual full integration. It further intends to enable Dayforce with localizations aligning to the set of countries covered by Excelity, with more expected to come longer-term through its roadmap.

While APJ is well in focus and adoption increasing, Ceridian has its sights set on deepening its global presence and capability. Late in June, it launched localization for Mauritius, with its first client, (IBL Group, a large multi-national firm with ~27k employees in 22 countries), as well as Germany, and Mexico planned by the end of 2021. It further supplements local payroll through its partner network to support broader EMEA and LATAM, and provide payroll coverage for 157 countries.

With Dayforce maturing steadily through its roadmap, including recent capabilities like Dayforce Wallet (U.S. only, with Canada set to launch in 2021), Dayforce Intelligence, Dayforce Safety Monitor, and deeper talent management capability (e.g. AI-driven recruiting), Ceridian is well positioned to gain continued adoption, particularly from strategic-minded, multi-national firms seeking next-generation HCM capabilities.

]]>

Earlier in the month on the NelsonHall HR Quarterly Buyer Market Round-Up session, many buyers agreed that compliance is going to be a bigger issue in 2020 and beyond than it was before. Before it was just table stakes, now it is about survival, and with the new WFH (Work from Home) structures, the risks are higher.

I had this in mind when I joined ADP’s Analyst Day last week. ADP shared how HR priorities are changing and how, as one of the largest HR and payroll providers, they have responded to the many shifting priorities and also staying close to clients to support their changing needs. Here are a few takeaways from the ADP Analyst event, through the lens of Liz Rennie. I consider these to be the most significant as they relate to HR in the pandemic recovery world:

- HR has been focusing on employee safety as the number one priority like never before – this we all recognize and is not news

- 10 years of job growth in the U.S. got wiped out in one single month – and an impact is job insecurity is heightened. HR teams know employee health and wellness, as a result, can indirectly affect productivity

- Employees working on the front line in COVID-19 crisis response industries do not need the extra stress of not being paid on time

- Compliance is now more than table stakes – navigating the relief opportunities offered by the governments in a timely way has meant the difference between a small business surviving or folding.

And just in case you didn’t appreciate your payroll provider enough, this is a glimpse of how ADP responded over the last months and how they are planning to help clients in the near term:

- ADP saw a 50% increase in clients reaching out to ADP the first few weeks of the pandemic compared to normal call volumes

- Implemented 1.4k feature changes from 2k legislative articles across 60 countries

- Responded within three days of the CARES Act passing to support small businesses with the implementation of its Paycheck Protection Program (PPP)

- Enabled 400k clients to run 2m SBA loan application reports, representing a value of $115bn

- Over $600m tax credits processed for 473k employees across 38k clients

- Partnered with Volunteer Surge. ADP’s Workmarket product helped onboard 1k volunteer health workers across 45 states within two weeks

- Offered free trial access of Employee Assistance Programs to clients through LifeCare to support workplace stress - 550 clients signed up in the last two months.

Three clients joined the ADP Analyst Day session to share their experiences of living through the pandemic using ADP services. All were very complimentary of how they had full confidence in the service. They also shared that ADP offered extended support, to the extent that if the client struggled to run a payroll internally, ADP offered to step in and run the payrolls on the client's behalf in the short term if that was needed.

Finally, it is great to see many wider initiatives to help the industry. ADP is assisting the industry through the following methods, which, if you’re not an ADP client, you can also benefit from:

- ADP Research Institute Labor Market Summit 2020: you can still register here

- COVID-19 microsite with employer tools launched 19 June 2020: www.adp.com/Forward

- Collaborated in key research such as The U.S. Labor Market during the Beginning of the Pandemic Recession see: https://www.nber.org/papers/w27159

- Creating thought leadership through the Marcus Buckingham Company with The Feedback Fallacy, Harvard Business Review’s most downloaded article in 2019

- ADP research Institute headed up by Dr. Ahu Yildirmaz produces some powerful insights, my favorite is this one: ADP Workforce Vitality Report – subscribe here

So what’s next for ADP? Don Weinstein, CVP Global Product and Technology, shared the ADP Workplace toolkit to help get employees back to office spaces. So what is good about this?

- Employees that state they are ready to go back can register as such through a survey

- HR organizations can accordingly plan, communicate and prepare the offices for specific workplace returns– allocating employees to different days of the week to enable staggered and rotational returns of different employee groupings

- COVID-19 health surveys regularly sent before returns to support attestation and screenings

- Touchless ADP mobile apps supporting entry on site

- ADP DataCloud to enable reporting and analytics and if needed, contact tracing based on attendance on site