What a difference a year makes.

Atos recently held its second North America business event in Dallas, just under a year since completing its acquisition of Syntel. Last year’s event focused on the newly formed Atos-Syntel organization in North America, and also on how, with a new CEO in place, North America was starting to address some legacy problems and to manage a situation where a chunk of business had gone away with some contract non-renewals: we felt that Atos North America was on a more positive trajectory than it had been in 2017, also that the integration with Syntel was being done less hastily than some of its previous large-scale IT services acquisitions (see our blog on the 2018 event here). This year, some major strides appear to have been made in North America in GTM, account management, portfolio and positioning – and there are some areas of good practice that Atos North America could export to other regions in time.

One priority has been to improve service delivery; if a very considerable improvement in NPS is anything to go by, this has been addressed. And issues in one problematic contract (going back to the acquisition of the IT services business of Xerox) have now been resolved.

In terms of portfolio, there has been a significant hiring of new talent, including a North America Digital Transformation Officer and a new head for its SAP practice, both with a mandate for offering development and innovation.

The new Digital Transformation Office is working on simplifying and packaging offerings from across the portfolio so that these resonate more closely with clients’ digitalization priorities, which it categorizes as:

- Being cloud ready

- Enhancing CX

- Improving innovation and agility

- Securing the business

- Using all their data

- Scaling their business

- Automating business processes.

That these are typically major priorities for enterprises today is undeniable. Overall, the messaging has come a long way from the product centricity of the Digital Transformation Factory; it is becoming more centered around use cases and on potential client benefits, though in some areas it remains a work in progress. Overall, there is an increasing emphasis on more flexible modular solutions from across the portfolio, and on flexible consumption models (the latter very different from some legacy infrastructure deals).

With SAP, Atos’ capabilities in North America have not historically been anywhere near as extensive as they are in geographies such as Germany and even the U.K., and they have focused on SAP BASIS ops. Initiatives in the last six months include setting up a small SAP consulting team as part of an ambition to target SAP transformation opportunities such as S/4HANA implementation/migration services; also, offering SAP HEC as a managed service on GCP. There are clearly strong ambitions here.

The fact that the global head of B&PS, Sean Narayanan, is based in New York indicates the importance being attached to Syntel. Benefits from the offshore delivery capabilities, the intelligent automation tools (the Syntbots platform) and agile delivery capabilities that Syntel has brought in should become apparent fairly quickly. Atos has completed the reverse integration of its larger B&PS contracts in other English-speaking geographies in a timely manner. Taking certain Syntel portfolio capabilities and exporting and expanding these across the group will take longer, as will developing more industry-specific offers for sectors such as healthcare payer and financial services.

While the Business & Platforms Solutions (B&PS) division in North America has been transformed with the addition of Syntel, the region’s legacy Atos Information & Data Management (IDM) division has also been busy, including working on adapting its GTM strategy. There has been a shift from the former pursuit of large managed services deals: the focus now is getting in front of clients earlier in their cloud journey and targeting smaller deal sizes such as cloud assessment engagements through which it can develop the relationship with the client to become a partner of choice for cloud design, migration and operations services.

Atos has said all year that North America would be back to organic growth by the end of 2019: in fact, it has achieved this in Q3. Something that perhaps would not have been expected a year ago is that the growth has come from IDM, which has done well to catch up the lost business from last year so quickly, rather than B&PS, which saw negative growth in its two priority sectors of healthcare and financial services

So, what next for North America? Of course, the ambition is to cross-sell the portfolio: this is likely to take time for a number of reasons, including little sector overlap in the region between legacy Atos and Syntel and lack of brand awareness. As we noted last year, in the short to mid-term, Atos North America is more likely to win broad-scope (infrastructure plus applications services) deals with mid-sized enterprises.

We expect to see an increasing focus in 2020 on vertical-specific offerings, most obviously healthcare, financial services and insurance.

And Atos North America might be exporting messaging about certain areas of the portfolio to the broader group; for example, the concept of ‘Singular IT’ mentioned a few times at the event – watch this space.

NelsonHall recently published an updated Key Vendor Assessment on Atos that includes its Q3 2019 results: for details, please contact [email protected]

]]>

It is a decade since Thierry Breton assumed the mantle of CEO and Chairman at Atos, his arrival marking the end of a troubled period for the company. In that time, the company has improved its profitability (when he arrived, its operating margin was just 4.8% and all service lines were experiencing a deterioration in profitability, so his ambition of a double-digit margin seemed ambitious). Also in that time, the company has grown in scale and geographic presence through a series of fairly significant acquisitions in both the Atos and Worldline businesses. These acquisitions have also led to some dramatic changes to its portfolio.

Atos recently posted its Q4 and full year 2018 results. These have been discussed in NelsonHall’s Quarterly Update on Atos, and a more comprehensive Key Vendor Assessment on the company will be published in the next few days.

But the real news had already happened two weeks before, at its Investor Day: this featured several major announcements, including the intended deconsolidation of Worldline, the next three-year plan for Atos, and also succession planning in place for Breton.

So why has Atos embarked on its next three-year plan one year before the current three-year plan is due to complete? In short, the time is right: two acquisitions, both completed in the last quarter, have provided heft and scale to both Atos and Worldline. With the additions of Syntel and SIX Payment Services, each business is now in a stronger position to pursue its own ambitions.

Five years after its carve out, Worldline becomes a standalone company

The first major announcement at the Investor Day was Atos’ intention to reduce its stake in Worldline from 50.8% to 27.4% through a proposed distribution of 23.4% of Worldline shares to Atos shareholders (who will receive 2 Worldline shares for every 5 Atos shares held), thereby deconsolidating Worldline from the Atos Group from early May 2019 (assuming approval at the AGM on April 30). Atos will remain the largest shareholder, followed by SIX Group with 26.9%.

We were not surprised to hear of this development, coming as it does five years after the 2014 IPO of Worldline and at a time of newly expanded scale: there are clear benefits to Atos shareholders, and to both companies, in becoming standalone. Both Atos and Worldlines’ board of directors have unanimously supported the proposal.

If we include a full year’s contribution from SIX Payment Services, which has expanded Worldline’s revenues from merchant services by 65%, and its geographic presence in the DACH region (primarily Switzerland), Worldline generated €2.2bn pro forma revenues in 2018. It is now a major player in Europe.

Worldline has been very clear about its ambition to become the dominant consolidator in the European payment processing market. And here it is succeeding, despite the disappointment of its failed attempt to acquire Gemalto: since its IPO, revenues have doubled, through a combination of inorganic and organic growth, and adjusted operating margin has expanded from 18.7% to 21.2% (again, pro forma, including SIX PS).

As a standalone company, Worldline will have an enlarged free float (45.7% post transaction, which we think might increase) with increased stock market visibility and be in a stronger position to use stock for acquiring: its ambitions as a payment processing consolidator are if anything even stronger, with the focus moving next to potential opportunities in some of the larger European economies. Separation from Atos might also be helpful in discussions with some banking consortia over potential new outsourcing opportunities; Worldline CEO Gilles Grapinet alluded to some large deals on the horizon.

Worldline shared its 3-year financial targets ambitions for 2019 to 2021. We believe the topline targets to be modest in ambition, given the M&A and large outsourcing deal aspirations.

Atos and Worldline will maintain commercial, industrial and GTM relationships via arm’s length contracts between the entities. This will include joint R&D programs and purchasing agreements.

ADVANCE 2021: the road ahead for Atos

So, what about Atos on a standalone basis?

Firstly, scale: including a 12-month contribution from Syntel, Atos generated €11.3bn pro forma revenue in 2018, with an adjusted operating margin of 10.0%. It remains a double-digit margin business without Worldline.

Secondly, profile: as we have discussed before, Syntel has changed the profile of Atos in terms of both geography and portfolio. With Syntel, Atos becomes less dependent on IT infrastructure services and becomes more balanced both at a global level and in its North America business. The reverse integration of much of Atos’ global B&PS business into Syntel continues in 2019. In its next three-year plan, entitled ‘ADVANCE 2021’, B&PS becomes a more important pillar of Atos’ growth plans for the next three years.

As part of ADVANCE 2021, Atos has introduced a new initiative, RACE (Road to Agile Competitiveness & Excellence), essentially the successor to various TOP plans, with a stronger focus on reducing direct costs, rather than optimizing G&A, to achieve further margin expansion. RACE has 12 pillars. We feel that some of these, such as the Global Optimization through Automation & Lean (GOAL) initiative (which started in H2 2018 and includes leveraging Syntel IP, increasing near/offshore delivery, and setting up shared service centers for indirect functions), indicate Atos is in catch-up compared to some of its peers. In terms of divisional margin targets, the division targeting the greatest expansion is B&PS, primarily from leveraging Syntel to achieve a 60% off/nearshore rate by 2021.

The three-year plan includes just 1-2% targeted organic growth in 2019, while North America and Germany (its two largest regions) recover.

IDM will remain a flat business for the next three years

With its Information & Data Management (IDM) division, a key priority is to get back to growth following declines in 2018 in Germany and North America (primarily the U.S.), where, under its new management, the outlook for 2019 appears much better than it was a year ago.

At a global level, IDM is now back under the leadership of Eric Grall, who is also Atos’ COO. The focus over the next three years will be on hybrid cloud orchestration, and IoT/edge computing, these areas balancing revenue stagnation in other units and the ramp-down of its traditional data center service business.

IDM has more growth ambitions for its U.K. BPO unit and wants to expand its financial services BPO business into Europe. Again, we feel the targeted growth over the next three years, which we estimate at around 8% CAGR, is a modest ambition given the healthy growth in many areas of BPO.

Overall, IDM is set to remain stable at around €6.3bn.

B&PS to benefit from market momentum in digital

The Business & Platform Solutions (B&PS) division enjoyed an improved performance in 2018, benefiting from repositioning around Digital Factory offerings. Syntel brings a business growing at ~10% (NelsonHall estimate), provides vertical expertise in the U.S. banking and healthcare industry, and will help capture project and digital transformation services growth in the U.S. There is (at last, we feel), an increasing focus on developing industry-specific propositions in each of its seven targeted verticals, potentially also pulling through IDM in some opportunities. This will be an important element in the next stage of Atos’ evolution. We will be looking with interest at how Atos will harness the industry-specific capabilities it has gained in different regions and develop a stronger cross-regional industry play. Strengthening the GTM approach is a key part of this, but on its own will not suffice.

Overall, B&PS is targeting a 5% CAGR for 2019 to 2021, which, assuming no major changes in the macro-economic conditions, is in line with our predictions for overall market growth in these services.

Atos looking to replicate the growth model of Worldline at BDS

Perhaps one surprise at the Investor Day came from Breton’s comments as to possible intentions regarding the BDS unit. BDS comprises a range of businesses, e.g. security products and services, HPC and high-end servers, mission-critical systems for the defense industry, and secure communication devices and software. The positioned commonality across these different activities is security, AI, and big data/analytics. The division continues to enjoy double-digit organic growth (12.0% organic in 2018) and is nicely profitable (divisional operating margin was 15.4% in 2018). But Atos is unusual as an IT services company in having businesses like these.

It appears that Atos may look to replicate what it has done with Worldline at BDS. Breton alluded to the need for BDS to be listed if it is to be a consolidator in the cybersecurity market and afford the high valuation multiples currently used in security M&As. He did not indicate a time line; however, we would not be surprised to see a listing before end 2020. Again, this would make obvious sense.

Atos has been an active acquirer in the last decade; significant M&A activity appears to be over for a while at least, with Atos focusing primarily on organic growth. Atos in 2021 may not be a significantly larger business, but we think it will have evolved in its profile and positioning.

By Dominique Raviart and Rachael Stormonth

Details of Atos Q4 and full-year results and financial targets in the new ‘ADVANCE 2021’ three-year program are provided in NelsonHall’s Tracking Service, Quarterly Update and Key Vendor Assessment programs. To find out more, contact Guy Saunders.

]]>

NelsonHall recently attended BearingPoint’s analyst event in Lisbon. As it starts its second decade with a new Managing Partner (Kiumars ‘Kiu’ Hamidian, only the second in the company’s history), the strategy that has served BearingPoint well in its first ten years is now evolving in ways that reflect significant developments in the nature of the consulting market.

In its first decade as a company since the 2009 MBO, BearingPoint has been something of a success story in the European management and IT consulting market, achieving sustained topline growth supported by geographic expansion, and steady improvement of its EBIT margin. 2017 revenues were up 13% to €712m, with growth in all geographies and service lines, and the firm is well on its way to achieve its targeted €1bn revenues by 2020.

Key elements of strategy

Elements of BearingPoint’s strategy in recent years that remain key pillars going forward include:

- The ‘One Firm’ mindset, with a common set of offerings and consistency of delivery methodologies across geographies

- The focus on clients headquartered in Europe, achieving a ‘global reach’ to be able to support them in projects outside Europe through an alliance ecosystem (West Monroe Partners in the U.S., ABeam Consulting in Asia, Grupo ASSA in LATAM)

- The business model, comprising:

- Strategy, made up of four service lines: digital & strategy, finance & regulatory, operations, IT advisory

- Solutions: the Solutions unit, launched in 2015, has three product lines: IP in regulatory technology, in particular fintech (e.g. its Abacus suite); advanced analytics; and digital platform solutions for the CSP and entertainment sectors (based on Infonova R6, now offered on AWS)

- Ventures, a more recent capability; e.g. an investment in Norwegian insure-tech start-up Tribe in April 2017. Also includes employee ventures, typically coming from its ‘Be an Innovator’ initiative, and client ventures, emanating from consulting projects with start-ups

- Selective acquisitions, for example in 2017 of retail supply-chain specialist LCP Consulting in the U.K., and an automotive consulting unit in Italy

- An increasing emphasis in recent years on innovation, e.g. the introduction of the ‘Be an Innovator’ process and of shark tank events.

Forward-looking priorities

While BearingPoint’s next five-year plan has yet to be finalized, Hamidian outlined four priorities in the following dimensions:

- Markets

- Portfolio

- People

- Culture.

Markets

BearingPoint is looking to build up capabilities in several European countries, including the U.K. (where the practice is relatively small, focusing on sectors such as financial services) and the Netherlands. In terms of headcount, BearingPoint remains very focused on Germany and France, and has product units in Austria (ex-Infonova) and Switzerland (Abacus): the ambition is to have a minimum of 300 people in each of the major European markets. Outside Europe, BearingPoint is also looking to work with its partners to expand its presence in the U.S. and China, including Singapore, where it has a joint hub with ABeam Consulting in Asia focusing on IP-based reg-tech projects.

Portfolio

There is a very clear drive to shift from the classic process redesign work of traditional consultancy services and focus much more strongly with clients on projects that leverage IP assets, and are more transformational in nature (for example, looking at new business models). The role of the Solutions unit is critical in this. Since January, the unit has had its own P&L and regional managers, encouraging, inter alia, entrepreneurialism in both product development and GTM.

In addition to some well-established assets around reg-tech (for which it is best known), the unit has also developed IP such as its Factory Navigator, which simulates production and logistics processes; LOG 360 vehicle emissions calculation, built on SAP HANA; and Active Manager, used for coaching and training front-line managers, e.g. in call centers, to be more active/effective. All are SaaS-based offerings. One of the clients presenting to whom we spoke is a very strong advocate of Active Manager, having implemented it at a major telco and subsequently introduced it in his next role in a different sector.

Expect to see further developments to the portfolio, including industry-specific solutions. But the strategic element lies in the intersection between Solutions and Consulting – the aim is for consulting projects and also managed services increasingly to have embedded IP.

As well as its own IP, BearingPoint is looking to increasingly position around its abilities to orchestrate an ecosystem of technology partner alliances: having started with Salesforce (now a Platinum partner), the emphasis has expanded to RPA and AI and emerging technologies such as blockchain. The last two years have seen a large increase in the number of technology partnerships, and more are to be expected.

The role of the Ventures unit is also important here. While BearingPoint also refers to employee ventures, most coming from its ‘Be an Innovator’ initiative, and to client ventures, emanating from consulting projects with start-ups, the primary focus is on market ventures. It is working with incubators such as LeVillage in Paris and weXelerate in Vienna (see our 2017 blog here) and hosting events like the BearingPoint Insurance Dialog in Cologne that offer speed dating opportunities for early stage start-ups. A recent investment was in Insignary, a South Korean startup with a binary level open source software (OSS) security and compliance scanning solution, BearingPoint’s first investment in an Asian start-up. BearingPoint is leveraging Insignary’s Clarity solution to offer a managed SAST (static apps security testing) binary scanning service in Europe.

The expansion of IP-based services is a key element of BearingPoint’s Digital & Strategy (D&S) offering, which we note has new leadership.

People

BearingPoint’s new Managing Partner has spoken repeatedly about his desire for the firm to provide a very positive employee experience, an important element in both the recruitment and retention of younger talent. Other priorities he has expressed include increasing the firm’s diversity, of generation as well as of gender (one target is 20% female Partners by 2020), and talent development. We do not know the age or experience profile of BearingPoint personnel, but we do detect a desire to have a workforce that is perhaps more balanced in terms of age and experience, and a slight shift away from a traditional consultancy profile.

We also note an evolution in leadership style with a stronger emphasis in transparency and communication: several personnel mentioned in conversation that Hamidian encourages colleagues to email him and is responsive when they do.

Culture

As part of its ambition to change the nature of much of its consulting work beyond operating model improvement to projects that have more radical transformation in mind, BearingPoint is looking (like many consulting and IT services firms) to nurture a culture where entrepreneurialism and innovation are encouraged (for example through initiatives such as shark tank events), and overall to become a more agile organization.

Hamidian is also looking to develop partners’ management and team leadership skills through initiatives such as new partner training programs.

Summary

In its first decade since the MBO, BearingPoint has succeeded in putting in place a strong foundation of an integrated European consulting firm that can claim, through its strategic partnerships, to have a more global reach. The next five years will be marked, not by global expansion, but by an evolution in positioning, with an increasing emphasis on services that leverage its own and partners’ IP to assist clients in their digital transformation, potentially also boosting margins. Expect to see more partnership announcements around IP-based offerings; shortly after the event, for example, BearingPoint announced its regtech product unit and IBM is partnering to offer a BPO service around regulatory reporting to smaller institutions in the DACH region.

Expect also to see an increase in tuck-in acquisitions of small firms operating in its target geographies (including the U.K.) that bring in industry domain and or specialist capabilities. Again, shortly after the event, BearingPoint announced its acquisition of Inpuls, which brings in capabilities in data governance and analytics and also doubles its headcount in Belgium.

As a final note, there were several aspects of the analyst day that stood out from other vendor events we have attended recently:

- The total absence of PowerPoint presentations, with a heavy focus instead on clients telling their stories and describing how BearingPoint has supported them

- The level of female representation (roughly 50% of the speakers) – an all-too common experience is that the only female speakers at analyst and advisory events are those from clients. Large organizations in Europe and the U.S. are increasingly demanding a level of female representation from suppliers bidding for work in certain areas of professional services; for a variety of reasons, lack of gender diversity in the talent mix will increasingly be an impediment in IT and consulting services). The level of female representation was doubtless a deliberate move; gender diversity is clearly a high priority.

L to R: NelsonHall's David McIntire, Rachael Stormonth, Andy Efstathiou, and Dave Mayer

NelsonHall recently attended an Atos North America event in Dallas which focused on the newly formed Atos-Syntel organization in North America. Earlier this year we noted that Atos in the U.S. was still a work in progress (see here). The event was held just days after its acquisition of Syntel had closed and we were keen to learn about the integration plans and the strategy for future growth in North America.

We came away assured that, with a new CEO in place, several problem contracts no longer an issue, and an enlarged set of capabilities, Atos North America is in a very different position from what it was at the beginning of the year. And looking more widely, Atos can now position as offering scale end-to-end services across infrastructure and applications in all its key geographies. We also note that this is an integration that is being done with perhaps less speed than some of its previous large-scale IT services acquisitions.

The significance of the Syntel acquisition

The event was held in Atos' regional U.S. HQ in Irving. Opened last year, the facility is also its first Business & Technology Innovation Center (BTIC) in North America. A clear emphasis throughout was that Atos in North America is now in a stronger position in terms of resourcing for a broad range of application services, including developing cloud-ready applications, as well as being able to support enterprises with reducing their infrastructure spend to invest in digital. It was also apparent that, in the short term at least, the growth opportunities are in mining Syntel’s client base rather than with acquiring new logos.

In July we wrote a short piece on the significance of the Syntel acquisition both to Atos North America and to its Business & Platforms Solutions (B&PS) business globally (see here). As a reminder, among other things, Syntel brings to Atos:

- Increased presence in North America (adding 4.5k employees and ~$825m in regional revenue, expanding it by around a third, and means that Atos North America has a broader set of capabilities it can offer to clients in the region

- A business that will be margin accretive to Atos

- Three large accounts: Amex, State Street and Fedex (which were ~45% of Syntel total revenues)

- A boost to its BFS and Insurance sector businesses (approaching $420m and $140m in revenue in 2017 respectively), also a significant U.S. application services practice in the Healthcare/Life Sciences vertical

- A large Indian delivery capability, augmented by its SyntBots Intelligent Automation platform

- Capabilities in apps development, testing and application modernization services (‘digital’ areas of application services)

- Its 'Customer for Life' ethos, which has been a significant factor in client loyalty.

We also noted that, given the level of reverse integration that is happening in B&PS, and the fact that Syntel had a larger presence than Atos in the U.S., the role of Syntel senior management is critical to the success of the integration. And the transition so far has been seamless: former Syntel CEO Rakesh Khanna, for example, remains as CEO of Atos-Syntel, which now operates as a unit within the B&PS division, and is on Atos’ Executive Committee. He presented alongside Sean Narayan, who heads B&PS globally, and Simon Walsh, the new head of Atos North America (an external appointment) about the capabilities of the combined entities.

Portfolio: with applications plus infrastructure services capabilities in North America, Atos can now position in the region around digital transformation

Atos freely acknowledges that until now, the only examples it could provide where its services were evidently supporting clients in their digital transformation were from Europe. It was not by accident that the event opened with Rakesh Khanna providing some case study examples of recent Atos-Syntel projects with clients outside its top 3 (AmEx, State Street, FedEx) where its services have helped the client play catch up with large digital disruptors in their respective industries. Other examples included a blockchain initiative and supporting an online insurer impacted by a high level of significant technical debt by migrating ~880k lines of code from COBOL to Java.

Three insurance sector clients presented: all are mid-sized organizations and have been clients of Syntel for many years. Common strands were consistency of (quality) delivery and proactivity, e.g. in one case approaching the client with a proposition around the transformation of its underwriting process. One of the three is also a new Atos IT infrastructure services client from earlier this year, having switched from an incumbent provider after 15 years: this client referred to the relative ease and speed of sourcing, appreciating having fresh eyes looking for new opportunities, and an outcome-based pricing model (based on net new premiums) that had been agreed.

Delivery: integration of B&PS into Syntel delivery model already in progress

While little was said about the reverse integration of Atos’ large B&PS accounts into the Syntel delivery model, or of Atos’ India delivery centers into Syntel’s, work on this has already started. The integration includes:

- Transfer of Atos’ North America and large global India-delivered B&PS contracts to Syntel, representing around $1.25bn, roughly one third of Atos’ overall B&PS business, of which $160m is from legacy Atos

- Alignment of Atos’ B&PS India-based delivery with Syntel

- Folding of some Atos delivery operations in Pune, Chennai and Mumbai into the larger Syntel facilities.

Any new B&PS deals incorporating global delivery will be pursued under the Syntel model.

The use of the Syntbots platform is expected to play a significant part in the ongoing delivery transformation in the RISE 2.0 program of the B&PS unit (which in our opinion had been in catch-up mode in the application of automation and AI). Atos is also assessing how and where Syntbots can play a part in its Infrastructure services business, e.g. in applying ML to incident management.

Improving sales execution & delivery performance in I&DM in North America

Three former problem contracts were terminated or expired earlier this year. The remaining few have been or are being addressed; one large problem contract has been reset and the new North America CEO holds a major incident review call every morning: there is evidently close attention being paid to improving delivery execution, also in staying close to other I&DM clients.

Following a period of disappointing sales performance, Atos is refreshing its I&DM pre-sales and sales personnel and architects in North America. There have been some new wins recently and the net new business is apparently strong.

Syntel clients happy with the larger scale of Atos

In the two weeks following the acquisition, Atos CXOs (Thierry Breton, Sean Narayanan, Eric Grall) managed to visit all Syntel’s key clients, representing ~70% of its total revenues; most were positive in that, as part of Atos, they can potentially look to Atos-Syntel for support in other geographical operations or in other services.

Future growth: farming rather than hunting; mid-market the primary focus

Among the attributes of Syntel emphasized by clients at the event were its effectiveness in forging deep relationships with them over the years and its consistency of delivery. Nearly all of Syntel’s revenue was through its existing client base and it brings to Atos strong account management and significant presales and solution architecture capabilities in North America, albeit for relatively (for Atos) small engagements.

Atos North America intends to leverage Syntel’s model and look primarily for smaller deals to grow wallet share in existing accounts. This is a significant change in emphasis in the GTM: both cross-selling and targeting smaller engagements are new areas of emphasis for Atos. An integrated approach into the Syntel client base has already commenced. Syntel’s 'Customer for Life' ethos brings in a new and improved approach to managing customer relationships; at the event there was a clear emphasis on client-centricity and on selling to specific client needs with a strong awareness that their appetite for the pace of change may differ significantly.

We note that in North America there is little sector overlap between Atos and Syntel: for example, Atos will have few local client references in financial services that it can draw on, though for smaller opportunities this will not be as critical a factor in vendor selection as it is in large deals.

Expect to see more vertical-specific offerings mid-term

Before Syntel, Atos’ portfolio in North America was primarily horizontal IT infrastructure services, though its earlier acquisitions of Anthelio Healthcare and three small healthcare consulting firms (two from Conduent) had indicated an intention to expand its presence in the U.S. healthcare sector. Syntel now brings in some application services business in the payer sector. Developing an integrated end-to-end portfolio for targeted segments of the healthcare sector remains an ambition.

We also expect to see a stronger play in the longer term in specific sectors within FS&I, also in manufacturing & retail.

Outside its top three clients, Syntel’s client base is typically drawn from mid-sized organizations, which is not where Atos has typically played.

Summary

The integration of Syntel immediately improves Atos North America’s ability to speedily resource B&PS deals without having to use resources from other regions, something which has at times been a competitive impediment. A large deal team remains in place and the legacy Atos North America focus on larger-sized enterprises for I&DM services remains. The ambition is also to cross-sell legacy Atos services into Syntel clients and to make a broader move overall into the mid-size market, and it is here that Atos is more likely to win broad-scope (infrastructure plus applications services) deals in the short to mid-term.

The increased emphasis on client intimacy in North America is also becoming more evident in the larger I&DM business in the region, where, with a new CEO in place, we also note a stronger focus on improving delivery reliability.

As well as having an immediate impact on Atos North America's offerings portfolio, Syntel is also a powerful boost to the B&PS RISE 2.0 initiative.

]]>

A year ago, following a TCS analyst event in Boston, the theme of which was Business 4.0: Intelligent, Agile, Automated, and on the Cloud, we wrote about how TCS’ new service line structure has been designed to support the company’s emphasis and positioning around Business 4.0 (see the blog here)

Underpinning its positioning around Business 4.0, over the past year TCS has been emphasizing two key capabilities:

- Location-independent agile

- Machine first delivery model (MFDM).

These two provided the core themes at the company’s recent analyst event in London. In our discussions with TCS execs, we were impressed by the speed and determination with which the company is moving to achieve the bold ambition it shared in 2017 to become 100% “enterprise agile” by 2020, also by its consciousness of how the nature of software engineering services will transform in the longer term.

Location-independent agile

With its stated target to be “enterprise agile” by 2020, TCS firmly placed a stake in the ground: to the best of our knowledge, no other IT services vendor has made a similar claim. TCS seems to be well on the way to achieving this objective with an estimated 250k of its 410k+ strong workforce already ‘agile ready’.

So, what is TCS doing to make this happen?

Unsurprisingly, there has been a massive retraining drive, accompanied by various efforts to nurture a culture where employees expect to continually learn (“making learning addictive”), something that becomes increasingly important as more roles become inter-disciplinary. A key asset underpinning its micro-learning platforms is its Karma gamification framework which has analytics and event-driven digital ‘nudging’ capability, used when an employee has been inactive.

Another core belief is that an employee’s contextual knowledge is more important than any specific technology skills – the aim is to train employees to become generalists rather specialists, particularly from roles that are next to be automated, by broadening the bar in their T-shaped skills profile to a V-shaped profile, e.g. training database managers on Hadoop, machine learning, and/or cloud systems administration. TCS estimates that its associates have on average four skills.

In line with this, performance management has moved from yearly assessments to micro targets.

Enabling tools that TCS has developed include:

- Jile, a cloud-based agile DevOps framework-agnostic product designed to help scale agile at the enterprise level. TCS launched Jile as a commercial product back in January (priced at $9 PU/PM)

- An Agile maturity model, an ‘agility debt’ framework with 27 characteristics codified from its experience with 300 clients, which it is now using to assess an organization’s agile readiness levels across the dimensions of structure, workforce, technology, and culture.

But enterprise agile also demands a transformation of the workplace: Krishnan Ramanujam told us that TCS is indeed transforming some of its larger delivery centers in India, including consolidating six campuses in Mumbai; removing cubicles in existing centers and installing large screens for interacting with team members based in other locations. We were assured that there is a “significant” investment in thus workspace transformation, but that there is no pressure on margins.

TCS’ emphasis on its capabilities in location independent agile is unsurprising: distributed agile is obviously important for large enterprises, and for many, their agile teams remain pockets of excellence. But getting distributed agile to work effectively is absolutely critical for those application services providers (by far the majority) that have an off/nearshore-centric global delivery model. Offshore delivery is not going away.

Machine first delivery model (MFDM)

As we have noted before in our Quarterly Updates on TCS, MFDM is not (just) using automation and AI for operations optimization. It is about giving technology the “first right of refusal” to sense, understand, decide, and act within a networked environment equipped with analytics and AI. The human interface is used for exception handling, training the machine to reduce exceptions, and for the application of contextual (often industry) knowledge.

The emphasis in the ‘Machine-first’ philosophy in the interplay between people and technology is how augmenting human capability can help unlock exponential value. The positioning is that MFDM can enable transformation in the client’s businesses (and, thereby, growth) for example through STP, new business models, increased speed to market, transformed CX, etc.

MFDM is thus a key element in TCS’ efforts to gain mindshare with stakeholders outside the CIO. We think there is more to be done in the articulation of the philosophy, as some clients (and, we noted, analysts) are honing on the automation aspect rather than the more disruptive business transformation play.

Ignio: in or out of TCS?

TCS describes its intelligent automation platform ignio as “the intelligent machine” behind MFDM. As with last year, most activity to date has been around IT operations (we estimate around 75%) though there is beginning to be increasing use of ignio to support applications development activities. The application of ignio in TCS’ Cognitive Business Operations business is in its infancy: obvious use cases include working on increasing the level of STP in activities such as finance, and accounting, supply chain, claims or mortgage processing. So, there are still considerable opportunities to leverage ignio across the portfolio.

At the same time, there is increasing traction for ignio as a commercial product, sold at times by other systems integrators. TCS highlighted that in FY18, its third year of operation as a commercial product, ignio achieved revenues of $31m, substantially more than many other SaaS enterprise products and also commented that it is looking to achieve >$100m in annual revenues in the next two years.

There is some tension between these priorities, and in discussions with execs, we noted some uncertainty as to the optimum model for ignio: as one of several product units within TCS, a separate subsidiary, or a standalone ISV which can sell more easily to other IT services providers.

The service portfolio revamp is helping drive digital; work to be done on full stakeholder play

In the last 12 months, TCS’ revenues from ‘digital’ services and solutions have increased by 49% to nearly $5bn. And the rate of growth has been accelerating: in Q2 FY19 revenue from digital services and solutions was up nearly 60% and accounted for >28% of the quarter’s total revenues (see TCS Quarterly Updates for more information). Moreover, this is organic growth. There is, of course, the caveat that there is neither commonality nor clarity as to different vendors’ determinations as to what classifies as digital, and in TCS case it has won some very large platform-based outsourcing wins that it would classify as digital. Notwithstanding, we are not aware of any other IT services vendor enjoying this level of organic growth at this scale, in what is primarily a services, rather than solutions, business. All IT services providers are undergoing a process of reinvention. Among the larger players, TCS is unusual in succeeding so far in achieving this through internal transformation.

Among the new standalone practices within the Digital Transformation Services (DTS) group, IoT and the larger Analytics & Insights unit are enjoying very strong growth. Taking longer to take off is Blockchain, with most activity still at PoC stage, a reflection of where the market is currently, but the pipeline is building up.

Among other things, the new service delivery structure has worked in helping advance TCS’ full services play and support its ambitions for its offerings to be more business outcome focused, and “to address issues of board-level significance”. However, this is not quite the same as having direct access to CxOs. While we appreciate that TCS does have direct access in some service areas and in some clients to stakeholders such as the CFO, we think there is more work to be done around the full stakeholder play and in elevating the TCS brand from technology to business partner, both in increasing thought leadership and also in the portfolio.

What next at TCS?

We have been aware that TCS’ messaging around Business 4.0 is resonating well with clients, but, as noted above, feel that the business transformation potential of the MFDM philosophy is less well understood. Expect to see more messaging in 2019 which provides specific client examples demonstrating the benefits realized from MFDM, and how the value proposition coming from the MFDM approach supports the delivery of specific services.

While TCS has focused on organic growth in recent years, we were keen to know whether there might be any tuck-in acquisitions to augment, for example, the design capabilities of TCS Interactive (and increase TCS’ access to client’s marketing budget stakeholders), or perhaps its managed security services capabilities. In short, we think that there is a possibility of both, that the recent acquisition of a design studio in the U.K. will be followed by other tuck-ins in other geographies, also that a cyber specialist asset, perhaps in the U.S. is attractive.

In terms of target markets, also expect to see an increasing focus on the U.S. public sector, for example, that builds on its experience in state Unemployment Insurance platform modernization.

Summary

A major focus of the event was to show why and how TCS has been redesigning and adapting organizational structures, facilities, processes and policies, and also its workforce culture to align with location-independent agile and with the MFDM. In our discussions with execs, we also picked up that the thinking is looking further ahead, to a time when there is virtually no coding and computer science skills become less relevant, and a primary key skill is data science.

One presentation referred to the great Wayne Gretzky's (dad Walter’s) advice to “skate to where the puck is going” (rather than where it is). This may have become an over-used aphorism in the corporate world, but, like all good aphorisms, is effective in neatly capturing a concept or principle. In our discussions with execs, we were convinced that TCS has a clear vision of the future of information technology, and it is investing to make sure that it will remain relevant even when the nature of IT services has changed dramatically from what it is today.

]]>

This week started with the announcement by Atos of its intended acquisition of Syntel for $41 a share, a total consideration of around $3.57bn including Syntel’s net debt of $201m, in an all-cash deal.

Syntel being acquired is not a total surprise: the company has faced some challenges recently, and in the previous four weeks its share price had been going up strongly (from $31.61 a share on June 27 to $39.13 at the end of last Friday, a jump of 24%). And Atos making a significant acquisition in the U.S. was very much on the cards. In fact, the companies said that they have had discussions about a possible tie-up going back to 2014, predating Atos’ previous major acquisition expanding its North American presence, that of Xerox ITO in 2015.

At nearly 3.7x revenue and 14.5x EBITDA, the purchase price at first glance looks high, but it’s a premium of just 5% on Friday’s close and of 14% on the last 30-day share price average. Assuming regulatory clearance, the acquisition will transact (unlike Worldline’s hostile bid for Gemalto): Syntel’s founders and affiliated entities (who own 51.1% of the company’s shares) have committed to vote their shares in favor, both companies’ boards have unanimously approved the transaction, and we do not expect to see a counter bid. Barring any regulatory challenges, the companies expect the acquisition to close by the end of the calendar year.

So why is Syntel attractive to Atos? In short, Syntel will provide:

- A boost to Atos' North America business ($823m revenues in 2017, representing 89% of its total revenue), in particular for application services – filling in the Business & Platform Solutions (B&PS) gap in Atos’ North American business we have commented on previously (see here for example)

- Three large clients: Amex, State Street and FedEx, which together accounted for just under 45% of Syntel’s revenues in 2017 (~$415m)

- A boost to its BFS and Insurance sector businesses (approaching $420m and $140m in revenue in 2017 respectively), also a significant U.S. application services practice in the Healthcare/Life Sciences vertical to complement Atos’ recent healthcare sector acquisitions

- A large Indian delivery capability: Syntel has ~18k (mostly delivery) personnel based in India with some large campuses in Mumbai, Pune, Chennai and Gurugram (previously known as Gurgaon) and has developed an effective resource planning model enabling fast deployment in new projects

- And, unlike some recent Atos’ acquisitions, it will be immediately margin accretive.

Syntel’s challenges have included its heavy dependence on H-IB visas with little substantive onshore capability, and a lack of discretionary budgets in many of its major accounts, particularly in BFS: the company’s revenues have been declining for some time (2017 revenues were down 4.4%, with BFS sector revenues down over 11%, the primary factor being a 30% decline in revenues from AmEx, following the completion of a large project).

Atos refers to 40% of Syntel’s revenues coming from digital (cloud, social media, mobile, analytics, IoT and ‘automation’). Syntel currently reports that revenue from digital projects accounted for 20.5% of total Q1 2018 revenue (Q4 2017: 19.7%), growing at 21.6% y/y with the other ~19.5% of revenues related to the automation and modernization activities that build the foundation for implementing digital capabilities.

Major initiatives have included:

- A focus on growing some of the top 4 to 50 clients, and here there has been some success: in Q1 2018, this group represented 52.5% of total revenue, growing at around 17% y/y

- Ongoing enhancements to its Syntbots intelligent automation platform, underpinning all its service lines, including additions in machine vision, NLP, ML and virtual assistants

- The Syntel X.0 workforce transformation model launched in 2017, aligning competency building with career planning and performance management to develop a future-ready workforce.

The simple addition of Syntel to Atos will:

- Increase its global revenues from €11.9bn to around €12.7bn

- Boost its operating margin from 10.6% to 11.5%

- Extend its Business & Platforms (B&PS) business from 26% to 31% of its global revenues

- Extend its North American business from 16% to 21% of its global revenues

- More than double its India-based headcount, to 32.5k.

But, of course, Atos is looking for more than a simple addition. In its rationale for the acquisition, Atos declares it is looking for additional revenue synergies, reaching ~$250m by 2021, with half achieved by 2020, from cross-selling opportunities in both the European and U.S. client bases. We think there are significant opportunities from:

- Cross-selling Syntel digital offerings, offshore-delivered apps development, testing and application modernization services into some of Atos’ European clients, particularly in BFSI and retail

- Cross-selling Atos’ infrastructure services into some of Syntel’s larger U.S. accounts

- Developing an integrated end-to-end portfolio for targeted segments of the U.S. healthcare sector.

Atos also expects the increased offshore delivery and revenue synergies will add $50m to the operating margin. To facilitate this, Atos is moving ~$1.2bn of its current B&PS work (~33% of 2017 global B&PS revenues) to operate under the Syntel model upon completion of the acquisition. This includes the entirety of the North American B&PS footprint (~$160m, <5% of global B&PS 2017 revenues), plus select contracts from other regions. Key aspects of Syntel’s delivery model that Atos is looking to utilize include increasing offshore leverage also the use of automation and agile delivery.

Atos is also targeting ~$120m from G&A optimization by end 2021 from the combined scale, including consolidation of facilities in India (Atos expects to move its employees based in Chennai and Pune into available space in Syntel’s larger campuses in these cities), plus the alignment of KPIs in B&PS

Will there be challenges in the integration? Of course. Some of the immediate ones that come to mind include:

- Aligning Syntel’s 'Customer for Life' ethos, with its implied customized approach, with Atos’ more standardized “Digital Transformation Factory” framework

- Managing attrition in India, though we imagine this will be easier now that employees will be working for a larger, more global organization

- Managing the reverse integration of some of Atos’ B&PS larger contracts into the Syntel delivery model

- Up and/or cross-selling larger transformational engagements into Syntel’s top 4-50 client base, which includes a long tail of small accounts; this will require substantive awareness raising.

Given the level of reverse engineering in B&PS, the role played by Syntel senior management will be fundamental. Syntel CEO Rakesh Khanna will join Atos’ Executive Committee and will be key to driving this.

And of course, Atos has a well-honed integration methodology and has successfully integrated some large and some more problematic acquisitions over the last decade.

The addition of Syntel will certainly fill in the B&PS hole in North America, add substantive offshore delivery, bring in IP such as its SyntBots and MIII (manage, migrate, & modernize) framework, and improve B&PS margins.

The acquisition should accelerate the B&PS transformation globally including in the application of intelligent automation to service delivery. It also means Atos globally has a more balanced portfolio in its IT services offerings. We think there are further potential benefits, for example in leveraging some of the IP that Syntel will bring in to develop more industry-specific offers for sectors such as healthcare payer and financial services.

]]>

Readers of the NelsonHall Quarterly Updates on Tech Mahindra over the last two years will be aware of initiatives that have taken place to turn around the LCC business it acquired, and also of recent investments such as a minority stake in Altiostar. This blog looks at some of the other sectors in which Tech Mahindra operates, and at some broad developments around service delivery.

Two recurring themes in the presentations at Tech Mahindra’s recent global analyst event in Hyderabad were ‘Future’ (a refreshing change from ‘Digital’) and ‘3-4-3’ – indicating the overarching intent to demonstrate how Tech Mahindra is developing its offerings portfolio to be relevant to clients in each of its target markets. Also evident was a strong focus on upskilling of personnel and innovating service delivery. Tech Mahindra is well known for its heritage as a specialist IT and engineering R&D services provider in the communications vertical, for engineering services in the auto and aerospace sectors, also for its work in supporting other Mahindra Group companies. To what extent is the company able to leverage these capabilities today to support other types of enterprises in their digital initiatives?

3-4-3 approach informing vertical initiatives

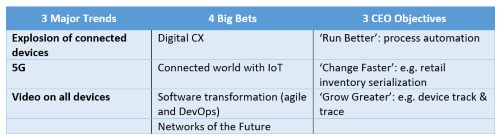

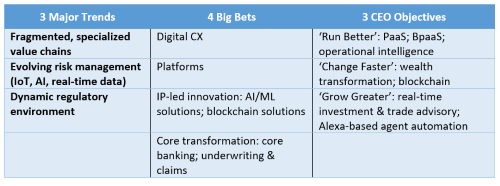

In his keynote, CEO CP Gurnani introduced the ‘3-4-3’ theme informing the portfolio strategy. For each target vertical, the company has picked 3 major trends, which have informed the selection of 4 focus areas in portfolio development (the ‘big bets’), and also the sector positioning in helping clients address 3 core CEO objectives: 'Run Better, Change Faster, Grow Greater'.

To briefly illustrate the application of the ‘3-4-3’ approach to two sectors: Communications, its largest and most mature (while Tech Mahindra’s dependence on this sector group has been reducing, it still represents nearly 43% of revenues) and BFSI, one of its smallest vertical units (13% of revenues).

Communications industry

BFSI sectors

Articulating what 3-4-3 means at sector level appears to be a work-in-progress (the links across the 3 dimensions are not always clear), but it is a neat approach for clarifying investment priorities and for developing a narrative around business outcomes for each target vertical: ‘Run, Change, and Grow’ workshops are likely to have been an important instrument in the very evident recent improvement in client mining (see recent NelsonHall Quarterly Update for details).

Tech Mahindra would be expected to have a strong narrative around the future of the Communications sector, so how does the 3-4-3 strategy translate into its investment priorities in the financial services sectors? Well, the acquisitions since 2015 of:

- BIO Agency brought in capabilities around digital CX (~£12.5m rev)

- Target Group (~£51m rev) brought in a platform BPaaS capability for processing lending and investment products. Target subsequently acquired the mortgage processing platform of Commercial First

- Sofgen in 2015 brought in Temenos and Avaloq core banking capabilities, focusing on German-speaking Switzerland.

BIO and Target Group both operate in the U.K. However, we have not seen cross-fertilization between them to develop more of a transformational story. Tech Mahindra continues to target relevant smaller scale opportunities in the mid-sized banking sector in the U.K. and EMEA.

Manufacturing industry

Let’s look at another broad vertical, one where Tech Mahindra has been enjoying double digit growth recently: Manufacturing. Here, it is benefiting from:

- Existing domain experience around connective devices, its strong heritage in product engineering services, also from supporting other Mahindra Group divisions, and from this, a close understanding of how AI and IoT technologies can be applied to enable new digital business models

- Some recent investments, such as its ‘Factory of the Future’ Lab in Hyderabad, which focuses on the use of technologies such as IoT, cloud, analytics, robotics, and AI in the manufacturing sector

- Its acquisition of Italian automotive product design house Pininfarina

- Partnerships, such as with Toshiba Digital Solutions.

In short, in discrete manufacturing, Tech Mahindra is well positioned for newer types of IT services around IT/IoT convergence and is investing in developing a range of new offerings. We might possibly see further tuck-in acquisitions, perhaps to help it better leverage Pininfarina for offerings around connected device.

More likely, we think, are additional digital agency tuck-in acquisitions, perhaps folding these into the BIO umbrella, with the U.S. the most obvious geography, to scale its digital agency capabilities and align these more closely to Tech Mahindra’s principal target sectors.

‘New Age Delivery’ for software of the future

As well as the vertical stories, we also got a brief introduction to this initiative to transform how software development is done, essentially to increase the speed (and quality) of code production. Tech Mahindra’s ‘New Age Delivery’ platform (it might be branded differently, but for this blog I’ll refer to it as NAD) combines various approaches and tools the company has been developing in the last few years. Key attributes and related assets (both proprietary IP and third-party) include:

- Automation and AI across the SDLC, leveraging its AQT (Automation, Quality, Time) suite of automation and AI tools, including TACTIx (IT and network ops), FixStream Meridian (IT ops) LitmusT (testing), Entelio (chatbots) and UNO (RPA), and Acumos, an open source platform for building and sharing AI applications

- Enabling the adoption of Agile and DevOps at scale, leveraging the ADOPT framework that it launched back in 2014, based on the CollabNet TeamForge ALM platform. Includes an Agile training kit

- Reusability, leveraging its ‘Blue Marble’ cloud-based business service integration platform for microservices

- Collaboration, using the Xtra Mile crowdsourcing platform

- Upskilling/reskilling capabilities including through gamification

- Co-creation with clients.

Some of these assets have been used by Tech Mahindra for some years; others such as Acumos, launched a few months ago, are much newer. Acumos, co-developed with AT&T and hosted by The Linux Foundation, is a marketplace where users can access AI and ML models packaged into microservices and connect them to data sources to build new AI applications. Self-organized peer groups, e.g. within a company, can share, test and review AI solutions. The initial target sectors (unsurprisingly given it is an AT&T and Tech Mahindra collaboration) are Telecoms, Media & Technology: use cases suggested include development of AI applications for use in video analytics, content curation and AR/VR. Acumos thus supports the key principles of reusability and co-creation noted above. Development of AI models will primarily be on open source; this is a timely move.

Tech Mahindra’s NAD platform also includes ‘Design Thinking as a Service’ (DTaS), 'Capability as a Service' (CaaS) and 'Upskilling as a Service’ (UaaS) which includes online training (takes in a developer’s rankings from the crowdsourcing platform).

The platform is helping Tech Mahindra position as a services aggregator, managing projects in which onboarded ‘capability partners’ can bid for pockets of work (code packages) in projects. The next stage of the initiative appears to be onboarding partners with the requisite skillsets (e.g. mobile) into the platform.

As well as extending Tech Mahindra’s reach in areas where there are skills shortages, the UaaS elements are of critical importance in re- and up-skilling its internal talent for newer technologies and methods of working (it includes a predictive tool for identifying appropriate candidates).

The NAD platform thus aims to address a number of critical success factors in software delivery today. It is clearly particularly useful for complex digital transformation projects. Presumably, Tech Mahinda can also extend its use to managed services engagements.

Tech Mahindra is currently using the platform with four clients in the telecoms and retail sectors.

All tier 1 IT services providers are busily accelerating their use of automation and AI in service delivery, with the focus still primarily in infrastructure operations. Tech Mahindra’s approach with its NAD platform (which focuses on software development) has a broader vision, one that includes harnessing crowdsourcing in a systematic manner, bringing in specialist partners, UaaS, and the Acumos marketplace, all of which are likely to be very attractive to clients.

The NAD initiative will be a key asset in evolving its delivery capability to help it achieve its target of having 50% of revenue from digital services by 2020.

TechMNxt: positioning statement and ecosystem program

‘TechMNxt’ is a term being used by Tech Mahindra as a positioning statement, as it works on becoming a ‘next gen’ IT services company in terms of technologies, business model, and employee capabilities. The company is also using TechMNxt to refer to a global program to engage with tech start-ups, alliance partners and academia to develop offerings in the areas of AI, ML, cybersecurity, next-gen networks, big data, IoT, etc., and also to open CoEs. A recent example of an initiative under this banner is opening a Maker’s Lab in a BT Research Campus in the U.K. Expect to see the brand being used increasingly.

Apart from its acquisition of HCI, the company does not appear to be planning to significantly increase its onshore presence in the U.S. to reduce its (relatively high) dependence on H-1B visas and also improve client proximity for (early stage) digital projects. Its strategy appears to continue to focus on the kind of activity that can be offshored.

Summary

CP Gurnani has been vociferous for some years about the need for the Indian IT industry to reinvent itself and to be capable of innovation, and this ambition is very clear at Tech Mahindra. The company’s heritage and domain expertise in Communications and its strong capabilities in engineering services will continue to be an important facet of its specialization. In addition, in separate conversations with the company, NelsonHall has been impressed by how Tech Mahindra is applying AI in its engineering services business.

The NAD platform is also a well thought-through stitching together of a number of approaches to software development.

While Tech Mahindra is convincing in how it is developing its offerings for the Communications and selected discrete manufacturing sectors, there is more work to be done in developing a coherent narrative about its ability in some of its other target sectors to support companies in major digital transformation initiatives. The fact that it still refers to its non-Communications units as its ‘Enterprise’ business is telling. We note that although BIO Agency and Pininfarina (both acquired in 2016) got star billing, there was no mention at all of HCI, its large recent acquisition in the U.S. healthcare sector.

A final note… unlike some Indian-oriented service providers (by which I mean those firms with primarily Indian leadership as well as Indian delivery capabilities, not just those headquartered in India), Tech Mahindra remains very proud of its Indian culture and centricity. Most of the client examples provided over the two days were Indian organizations (though 47% of its revenues are from U.S. headquartered organizations), which gave a slightly local feel to this global analyst event.

]]>

NelsonHall recently attended NIIT Technologies’ analyst and adviser event in London, and we were keen to get an update on developments at the company since the arrival of Sudhir Singh as CEO. We were aware that the last two quarters have seen a significant increase in the number of large deal signings (five, compared with two in H1 FY18), also that there have been a significant number of new appointments - but generally NIIT Technologies has been rather quiet. It is now apparent that the company has been embarking on a major transformation.

From Geographic to Industry Focus

This transformation is most evident in a radical organizational restructure from the former geography-based P&L to one that is vertical-led. In sales pursuits, there has been a sharper vertical-specific narration and a stronger emphasis on capabilities in digital, data, cloud and automation – and this is likely to have helped in at least some of the recent large deal signings.

NIIT Technologies is now structured primarily around three key industries, in each of which there is a focus on a specific sub-segment where the company would like to have a dominant position:

- Travel & Transportation (26% of total revenue), specifically airlines & airports

- Insurance (we estimate ~24% of total revenue), specifically commercial and reinsurance (primarily London market)

- Banking & Financial Services, (~19%), specifically wealth & asset management.

The importance of this is not to be underestimated: in both IT and business process services, deep industry domain expertise, and ideally IP, is a key factor in vendor selection. Having recognized the need to operate at the intersection of selected verticals and emerging technologies, NIIT Technologies has made a wholesale rejigging that goes from go-to-market right through to delivery.

The former ADM organization (which generated two thirds of the company’s total revenue) has now been folded into these three verticals; each now has a Global Head (who may also have a regional responsibility) and a head of delivery. The former head of ADM is now wearing a different hat: as NIIT Technologies’ first ever CTO, his responsibilities include accelerating the use by the company of blockchain, IoT and AI.

The other much smaller service lines of Infrastructure Management Services and BPS stay as standalone units, and there are also separate units for Data/Automation and Cloud.

Singh has also introduced:

- A large deals pursuits team, in parallel tweaking salesforce incentivization plans to increase the focus on large deal ($20m+) wins

- A new partnerships and alliances organization.

External Leadership Hires, Center of Gravity Moved from India to the Markets

Since Singh’s arrival, the company has been on a hiring spree: all the three vertical global heads are new recruits, as are the global heads for Data & Automation (a new service line), RPA, and Cloud.

Several things are evident in these recent leadership appointments:

- They are all external hires, and from much larger firms

- They are all based onshore, close to clients: three of the eight are based in Princeton, NJ (where the CEO is also based) and two in London (near the London market client base)

- There is a clear focus to accelerate the use of intelligent automation (IA) in service delivery, also to expand capabilities in data & analytics.

This influx of new senior execs is not part of a turnaround program: NIIT Technologies’ topline growth in recent years has been steady, if not stellar, and EBIT margin has not been under any unusual pressure. What is happening should be seen rather as an evolution, one that builds on assets and capabilities that the company has acquired or been developing over the last few years, including:

- Proprietary IP such as Mona Lisa for the airlines sector and the suite of products (Navigator, Exact and Acumen) for the commercial insurance sector. As we indicated in our blog last year (see here), the recent focus in product development has been adding microservices (10 were launched last week) and cloud-based tools to improve the UX: next month will see the launch of a smart assistant, Aniita, and an analytics tool, Score

- Capabilities in Pega and Appian, through its acquisitions of Hyderabad-based Incessant Technologies in 2015 and Ruletek in 2017, which expanded Incessant’s delivery presence and client base in the U.S. BPM is a building block in digital process transformation

- Its ‘TRON’ intelligent automation platform. Our perception is that while NIIT Technologies is slightly in catch up mode in the use of IA in its delivery of both application and infrastructure services (e.g., it currently has 4 PoCs in progress using arago’s HIRO), there is a strong push to change this.

“Engage with the Emerging: Innovate, Incubate, Industrialize”

This phrase neatly captures the journey on which NIIT Technologies has embarked: to build on its existing industry knowledge by expanding its capabilities in emerging technologies and by industrializing service delivery through IA. The ambition is clear: for clients in its target sub-verticals to see NIIT Technologies as a partner of choice for large scale digital initiatives, not just as an offshore ADM provider with experience of operating in their vertical.

So, what will we see at NIIT Technologies over the next year? In brief:

- More industry-specific use-case in the use of cognitive, IoT and blockchain (which has obvious relevance in all its target sectors), with concomitant marketing

- Much greater use of IA across service delivery, particularly in infrastructure services,

- Expansion of the existing partnership ecosystem, e.g. around cognitive tools, analytics, fintech

- Expansion of cloud-based offerings and of API capabilities in each of the three key sectors

- NITL (the insurance software unit) growing its client base outside the U.K., with a particular focus on the U.S.

- Double digit CC growth (EBIT margin expansion coming after: the current priority is topline growth)

And what might we see?

- Stronger interaction between Incessant Technologies and the vertical units in building out vertical-specific digital transformation narratives

- Niche acquisition activity, e.g. around data and analytics

- More onshore hiring, e.g. of solution architects, data scientists, vertical domain SMEs, etc.

- The creation (though unlikely in 2018) of a fourth vertical unit, perhaps manufacturing, or possibly media (though the acquisition of key account Morris by Gatehouse is causing a major dent in this business).

Summary

Sudhir Singh was appointed last May as CEO designate, taking over this January from Arvind Thakur, NIIT Technologies’ first-ever CEO, and now Board Vice Chair. In that seven-month period he was able to put in place some of the building blocks for the next phase of the company’s development, one where it can position on possessing capabilities across vertical domain, emerging technologies, and IA: three absolutely critical attributes for staying relevant to clients.

]]>I was subsequently assured by HP ES leadership that its federal sector business would be an important part of the newco. I should, of course, be mindful of the fact that a business can switch from being deemed “core” to “non-core” at the moment it is divested.

Anyway, six months after the creation of DXC Technology, we have an answer: DXC Technology is to spin off its U.S. federal business and merge it with two Veritas Capital-owned businesses, Vencore (formerly the SI Organization, spun off from Lockheed Martin in 2010) and KeyPoint Government Solutions (provides background investigation services for federal government agencies formerly Kroll Government Services, acquired by Veritas in 2012), creating an independent, publicly traded U.S. government IT services contractor. As with the CSC/HP ES tie up, this is a tax-free RMT transaction, and Mike Lawrie will be Chairman. Is this a total surprise? Perhaps not.

Some Details of the Transaction

- The newco ownership will be 86% DXC shareholders/14% Veritas Capital

- Newco will pay $400m in cash to Veritas and $1.05bn to DXC. It will also assume $700-800m of Vencore debt

- DXC will use the proceeds to reduce debt, repurchase shares, and “for other general corporate purposes” (possibly M&A?)

- Veritas Capital’s Ramzi Musallam will join the newco board

- Newco CEO will be Mac Curtis of Vencore, COO will be Marilyn Crouther of DXC

- The transaction is expected to close by March 31, 2018.

DXC Rationale for the Transaction

DXC highlights that splitting its USPS and commercial businesses will enable each to focus on their respective market dynamics, optimize capital allocation, and “drive customer value through highly tailored offerings and services”.

The press release also states that combining USPS with Vencore and KeyPoint “will significantly strengthen USPS’ competitive position”. This is perhaps the more pressing factor. If we look at the performance of USPS in its Q1 FY18 (the one quarter that DXC has reported since its creation), it had a very low 0.3x B2B. This, obviously, is partly a reflection of lumpiness in large deal awards in the sector, partly a contraction in federal spend, and partly a timing issue (slippage in signing of a large award in the National Security sector), but it does also indicate a lack of competitiveness.

The Newco: a Top 5 U.S. Federal IT Services Contractor

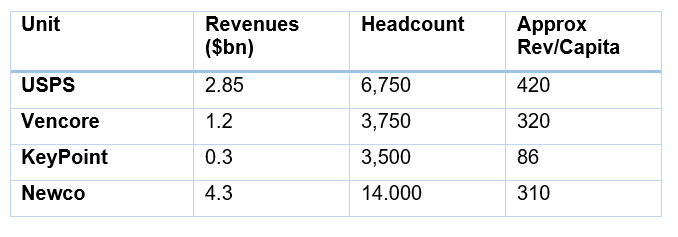

The table below summarizes approximate revenue and headcount for each of the three businesses.

Joining forces with Vencore and KeyPoint will add scale: as a $4.3bn firm the new company will be a top five (by revenue) U.S. federal IT services contractor, similar in size to SAIC and CACI, and not much smaller than (mostly former CSC business) CSRA.

We don’t know the margin profiles of Vencore and Keypoint but suspect that Vencore is at least on a par with USPS (11.4% segment margin in Q1 FY18); its portfolio includes some high margin offerings, also Veritas was looking for a buyer for Ventura in 2015, and is likely to have stripped out costs since. Certainly, in its investor presentation, DXC refers to “industry-leading profit margins”.

While neither USPS nor Vencore has been enjoying topline growth recently, the opportunities for the newco are likely to center more on revenue than on cost synergies, though there will be obvious ones, e.g. around HQ rationalization, also in applying automation to the KeyPoint business.

Vencore, for example, brings to the table capabilities in cyber (enhanced with its 2014 acquisition of Qinetiq North America), and analytics, as well as system engineering.

There is little client overlap: Vencore’s client base includes Intelligence and Defense agencies, whereas, outside its DoN NGEN contract (where the addition of Vencore may be an important factor in the recompete), the USPS federal client base includes the likes of VA, HHS and CMS. The newco will have both a broader portfolio and also access to a broader range of contract vehicles - as Lawrie highlighted, significantly strengthening USPS’ competitive position.

There is shareholder value in this transaction, but what does this mean for DXC?

The transaction will not mean that DXC becomes a commercial sector pureplay: it retains a large public sector business, both internationally and also in the U.S. state and local segments. Looking ahead we suspect further smaller-scale divestment activity may be on the cards.

Meanwhile, DXC continues to invest in expanding certain parts of its portfolio, this week announcing the tuck-in acquisition of Logicalis SMC, further strengthening the already extensive ServiceNow capabilities that CSC then DXC have been ramping up through a series of acquisitions.

We look to see whether there will be also be an increasing emphasis by DXC on certain sector plays, for example Insurance (for example Xchanging brought in insurance software IP and there is the big win a MetLife)): a heavily verticalized (commercial sector) focus has not been a feature of CSC nor HP ES in recent years, but within its GBS business, its Industry IP and BPS businesses could do with a shot in the arm.

Postscript

The initial title of this blog was: "DXC Spins Off U.S. Federal Business: State and Local Next?" However, I overlooked its acqusition of Microsoft Dynamics 365 specialist Tribridge, for which, its Q2 FY18 SEC filings reveal, it has paid $152m. Tribridge, now part of GBS, enhances its offerings and presence in the healthcare, justice, and public safety markets. And of course DXC has a significant presence in the Medicaid sector, with a practice currently included in the health unit of its Commercial segment. Mike Lawrie has sold off a U.S. public sector business twice now; acquiring Tribridge and then doing this for a third time (of units serving various state and local markets) is extremely unlikely. Once USPS is spun off, will we see more clarity about the various non private sector industry practices that currently tucked within Commercial?

]]>]]>