In its Capital Markets Day last week, Atos CEO Philippe Salle unveiled a four-year plan for the company. The ‘Genesis’ plan has the following financial targets for FY 2028:

- €9-10bn in revenue

- A 10% operating margin

- ‘Towards an investment grade credit rating profile’.

The last of these provides an indication of some of the challenges facing the company, which last year suspended financial forecasts as it was restructuring. Now that a restructuring agreement with its creditors has been agreed, Atos can look to the future with less uncertainty hanging over it.

Key components in the Genesis plan include a significant simplification of the business structure, fewer brands, exiting non-core countries, trimming costs, and investments in AI. All of these would be expected in a turnaround strategy.

The stated ambition is for Atos, once a European powerhouse, to be recognized as ‘a global AI-powered technology partner shaping secure end-to-end digital journeys’ and become one of the preferred vendors for global clients.

So, let’s unpick some elements of the plan, the name of which is conveniently an anadrome of Atos – SOTA (Simplify, Orchestrate, Trim, AI-Enable).

Simplify

The Simplify initiatives cover:

- The brands and org structure. The decision to reorganize the former separate ‘Tech Foundations’ and Eviden businesses back to a unified group is welcome. Atos Group now consists of:

- A services business, Atos. This has 6 business lines, including a new business line for data and AI (see below)

- A products business, Eviden. This includes the Advanced Computing business (€800m revenues) currently being divested (to the French state for €500m, up to €625m including earn-outs; this activity is deemed of critical importance for national security). The other units are Cybersecurity, Mission-Critical Systems (the sale of these two products businesses to the French government having been put on hold), and Vision AI

- Geographies. There has been another slight reorganization of the former Regional Bus, not long after a change in composition in Q4 2024. Notably France now becomes a discrete RBU: this makes total sense for Atos. The rest of the former Southern Europe is now folded into International Markets which also includes the former Growth Markets RBU. The intention is to exit from several smaller, non-core countries in this BU, a not unexpected decision in this turnaround strategy

- Governance. Again, none of the initiatives that were outlined to simplify P&L, group and portfolio governance are unexpected. P&L remains with the RBUs, with the business lines having accountability for portfolio and R&D investment

- Offerings, with a reduction in the portfolio to around 40 offerings of which ~20 will be high priority. AI (mainly GenAI) is one priority area, and Atos has created a new entity, Data & AI, which aims to bring together all its offerings and consultants. Data & AI will develop use cases around AI in factory mode for other parts of the portfolio. Cybersecurity, of course, remains a priority for Atos.

Orchestrate

This covers:

- Organization. We note the refreshed leadership team is lacking women running any RBU or business line, a shame given the target to have 40% of the new hires being women this year

- Operating model, with a common, simplified commercial model across the group. As would be expected, the aims are to increase the level of cross-selling within the geos, expand the global large deals team, and to push the high potential growth offerings (where Atos is rapidly expanding its sales specialists).

Trim

Again, there are no surprises in the various initiatives to reduce the cost base. In terms of delivery, Atos plans to:

- Reach 60% offshore delivery by 2028, primarily from scaling global delivery centers in India

- Further industrialize delivery

- Improve bench management, with an 85% billability target by 2028 (up from 76% at the beginning of the year).

We feel Atos has ground to catch up in each of these areas.

And, of course, there will be a streamlining in G&A: the target is to have G&A expenses from 7% currently down to 5% of revenues by 2028. There will be a headcount cut of around 1k.

AI-Enable

Like its peers, Atos is working at speed on bringing AI and GenAI both to its offerings and to its own delivery of IT services.

Atos has created a new business line dedicated to data and AI, which it plans will be a key growth driver for the group, growing fivefold from 2k to 10k employees by 2028. The offerings will span advisory, solution development focusing on GenAI and Agentic AI, data services and pre-packaged industry AI solutions.

The planned investments include up to €500m in R&D, and €100m in start-ups.

Key takeaway 1: Atos can now look to the future

Atos has been through a very turbulent period and this has not been helped by a very rapid succession of CEOs (Salle is Atos’ seventh CEO since Thierry Breton left to join the European Commission, and the company’s sixth in the last two years). Salle has extensive experience of successfully managing a business turnaround. New CEOs (ones that are not internal hires) can be open when starting in role about challenges related to historic company weaknesses. And Salle listed some of the key factors contributing to the company having lagged the market since 2022, notably loss of market confidence around the financial restructuring, instability in leadership and strategy, and limited exposure to rapidly growing segments of data & AI and cloud.

The company now has stronger liquidity and has no debts expiring before end 2029. This means it now has the time and flexibility to execute its strategy - if it does not repeat some of the organizational and go-to-market weaknesses of recent decades.

The Genesis transformation plan looks realistic; the extent to which it is working will of course not become apparent before 2027. If executed well, it looks as if Atos can regain its status as a major player, at least in Europe – and Europe was the focus of the Capital Markets Day.

In the short term, 2025 targets include revenues of €8.5bn (down 10.9%, citing voluntary contract reviews and low business traction prior to the completion of its rescue plan) with a slight improvement in operating margin to 4%. With proforma adjustments for the divestment of Advanced Computing (around €0.8bn) and planned exits from non-core countries (around €0.3bn), total 2025 revenues could be closer to €7.5bn.

Looking to 2028, the revenue target of €9bn or €10bn includes inorganic growth. The organic growth target is €8.5bn to €9bn, a 2025-2028 CAGR of 5% to 7% – which could well turn out to be in line with overall market growth across this period (the general expectation currently is no real market recovery before 2026). The success of any M&A activity, which will not be resumed before 2026, is critical to Atos’ future health. Atos needs to be better disciplined in both selecting acquisitions/new capabilities and in subsequently integrating these than it has done historically.

Similarly, decisions on investments in R&D, in partnerships and in start-ups will be critical as Atos will be somewhat late to the GenAI/agentic AI party.

Key takeaway 2: Cross-domain integration is key

Historically, Atos has not been particularly effective in cross- and up-selling to its large enterprise clients. The company does indeed have IT lifecycle capabilities spanning IT strategy & consulting, design, implementation, and ongoing support. And it is expanding its large deals team.

Looking ahead, it will, naturally, endeavor to cross-sell higher growth areas of cyber, and data & AI to its IT infrastructure, workplace and digital division client base.

But there is a big difference between having a focus on ‘cross-selling’ and going to market with integrated services offerings with business-value-based propositions. We look to see some evident progress by Atos in developing integrated services offerings that clearly address clients’ business priorities, not just their technology challenges, in parallel to strengthening its stakeholder engagement with more large enterprise clients.

Similarly, we also look forward to the tailored industry offerings.

P.S. In the week since the Capital Markets Day we have been looking at market and client response: we would broadly term the former as cautious and the latter as warmer. Clients that have stayed with Atos in recent years have welcomed the increased clarity this year.

]]>

At the Cognizant UK & Ireland analyst and adviser meet in London this week we were keen to get a closer understanding of three things:

- How some of the changes introduced since the arrival of Ravi Kumar S as CEO are making a difference to the company

- The factors underpinning this year’s revenue underperformance of Cognizant in the UK and Ireland, also any new go to market priorities for the region

- Cognizant’s plans for leveraging the newly acquired Belcan.

Our takeaways in all three areas were encouraging and we came away with a positive outlook both for Cognizant in UK and Ireland and for its expanded ER&D business.

Cognizant in September 2024: refreshed management, more energized workforce, radically improved CSAT

Firstly, anyone who follows Cognizant will be aware that since his arrival in January 2023, Ravi Kumar S has brought in a wealth of new senior talent (including at the very top CFO Jatin Dalal, ex Wipro, and EVP and Global Head of Operations Rajesh Varrier, ex Infosys).

To give a few more examples:

- In terms of sector heads there are two new SVPs formerly at Infosys, Anurag Vardhan Sinha (Comms, Media & Tech) and Nageswar Cherukupalli, (Financial Services and Insurance). Also fresh from Infosys is Shweta Arora, now SVP, Global Head of Consulting

- Wipro, in addition to Jatin Dalal, has also lost Mohd Haque, now Cognizant’s Chief Commercial Officer, Americas. He also brings in extensive sector domain expertise and networks, this time in healthcare, a key sector for Cognizant.

It is almost customary for a new CEO to bring in execs that they have worked with or alongside before, particularly when joining a company that has faced well publicized challenges – this is not remarkable. But changing faces does not always work its magic. At Cognizant, there is a palpable sense of revived energy and of clarity about corporate strategic priorities.

One of Ravi Kumar’s stated priorities is for Cognizant to be “an employer of choice”: this does not sound particularly ambitious, but it does hint at challenges the company was facing, including around attrition, recruitment, employee morale, and also performance. Attrition has fallen at Cognizant – but so has it for its peers: this reflects the current labor market. One initiative launched last year, the “Blue bolt” internal grassroots “idea incubator” is likely to be having a positive impact on both employee involvement by delivery personnel and also client perceptions of Cognizant, thus a contributory factor to company achieving its highest ever Net Promoter Score, after a less successful period. We gather that NPS has increased in the last 2 years from 46 to 60, a huge improvement.

Increasing focus on Industry Solutions

Cognizant formerly had four “integrated” horizontal practices (Core Technologies and Insights, Enterprise Platform Services, Intuitive Operations & Automation, Software & Platform Engineering). In 2023, Cognizant set up its Industry Solutions Group as part of the company’s strategy to build further differentiation at the industry level. The ISG is essentially a sub-unit (led by EVP of Intuitive Operations & Automation) that houses industry technologists and specialists in vertical micro-segments with the remit to work with external partners in developing industry-specific products and services: an early example is Telco Assurance 360, built on ServiceNow.

Cognizant UK & Ireland: looking to new offerings in key sectors

After three years of decent growth (3-year CAGR of 12.2%, thanks primarily to the strong U.K. public sector), Cognizant UK&I has had a disappointing year so far in 2024, at least in terms of revenue performance. H1 revenues of $900m were down 5.4%, around 6.4% in CC). An 11.4% decline in the financial services sector (last year accounted for a third of UK&I revenues) accounts for most of the region’s underperformance: this can be attributed to falling discretionary spending, Cognizant having lost out on vendor consolidation at a major U.K. bank.

For some vendors, the U.K. continues to be a growth region in 2024 (we note TCS, 6.0% growth in its last quarter, Sopra Steria, 5.3% in H1 2004). Those vendors have invested heavily in the region and have some well-established and very large outsourcing arrangements. Although Cognizant has made a number of tuck-in acquisitions in recent years in the region (and Belcan has also brought in U.K. capabilities), we would argue that it has not done this: UK&I represents just 9% of global revenue (in comparison, the region accounts for around 17% of the global revenues for TCS and Sopra Steria) and most activity remains dependent on discretionary spend; Cognizant is not protected by sizeable outsourcing deals.

So, what are Cognizant’s priorities for UK&I? Nearly two years ago, we noted the following:

- Continued focus on the U.K. public sector (central government, defense, and health)

- Reigniting the BFS sector across banking, targeting large deals and security and market infrastructures, also government regulators, and fintech

- Scaling up consulting sub-vertical expertise.

This broadly remains the case today. The sectorial priorities are still BFSI (specific areas of banking, also of insurance), public sector (back-office operations), also Comms Media & Tech (e.g., field operations, order processing, digital content marketing). We note a stronger focus now on outsourcing opportunities, including areas of BPS. Cognizant does not have a significant presence in the U.K. for BPS and thus will be positioning as a challenger. There are some obvious areas of both public and private sector BPS which present potential opportunities for Cognizant in which to look to compete.

Belcan – third acquisition in ER&D means end-to-end ER&D service capabilities

Cognizant has been investing since 2001 in boosting its ER&D capabilities. That of Belcan, recently completed, follows the company’s earlier acquisitions of:

- Mobica (March 2023), an IoT software engineering services provider headquartered in Manchester. Mobica brought in nearly 900 employees across Europe and the U.S., including around 550 in Poland, a significant expansion of Cognizant’s nearshore delivery capabilities in Eastern Europe (where we felt it had lagged its peers)

- ESG Mobility (June 2021), a Munich-based engineering R&D provider for connected, autonomous and electric vehicles, brought in around 1,000 employees, in Germany, U.S., and China.

In total, we estimate Cognizant has invested $1.75bn in these three acquisitions, including $1.29bn for Belcan (the company’s largest acquisition since that of Trizetto). The rationale for beefing up ER&D capabilities is clear; our interest is how Cognizant intends to leverage Belcan (which is slightly margin dilutive, we note also it counts Boeing as a major client, although its overall revenues are growing).

Belcan has around 6,500 employees globally and gets around 85% of its revenues from the U.S. Its revenue mix is approximately 45% product engineering, 34% systems & software (model-based engineering, embedded software), 21% manufacturing and supply chain. A blend that dovetails nicely with those of Mobica and ESG Mobility: in terms of its portfolio, Cognizant can now claim to having end-to-end capabilities and scale (around 10,000 employees) in ER&D. An immediate priority will be integrating the three companies, presumably under the Belcan brand.

Belcan brings to Cognizant a presence in the aerospace sector: as well as there being continuing high demand for engineering talent in this sector, there are opportunities to bring in IT services capabilities from Cognizant to clients such as Airbus. Belcan also has some activity in the defense sector: we would not be surprised to see Cognizant look to leverage this to set up a federal sector business in the U.S. We see also potential opportunities for Cognizant to introduce Belcan to some of its automotive sector clients in Europe.

Renewed sense of confidence

It is less than 21 months since Ravi Kumar started as CEO. This blog does not aim to be comprehensive: it does not, for example, look at progress in major initiatives such as the corporate push to land large outsourcing deals (where the company has seen success in North America) but we note a renewed sense of confidence at Cognizant and in the UK&I market and we look to see some new developments over the next year or so.

]]>

NelsonHall recently wrote a PoV on the current disconnect between GDP growth and IT services spending[1]. In October 2023, the IMF refreshed its GDP growth predictions; these include better 2023 GDP growth in the U.S. (+2.1%) and Japan (+20%) than the U.K. (+0.5%) and the Eurozone (+0.7%). Unusually, the IMF's predictions are not in line with our observations of IT services spending. In calendar Q1-Q3 2023, IT services spending growth fell sharply in the U.S. (to low single-digit), while the U.K. and Europe remained solid.

Performance Convergence in Q3 2023 Despite Different Footprints

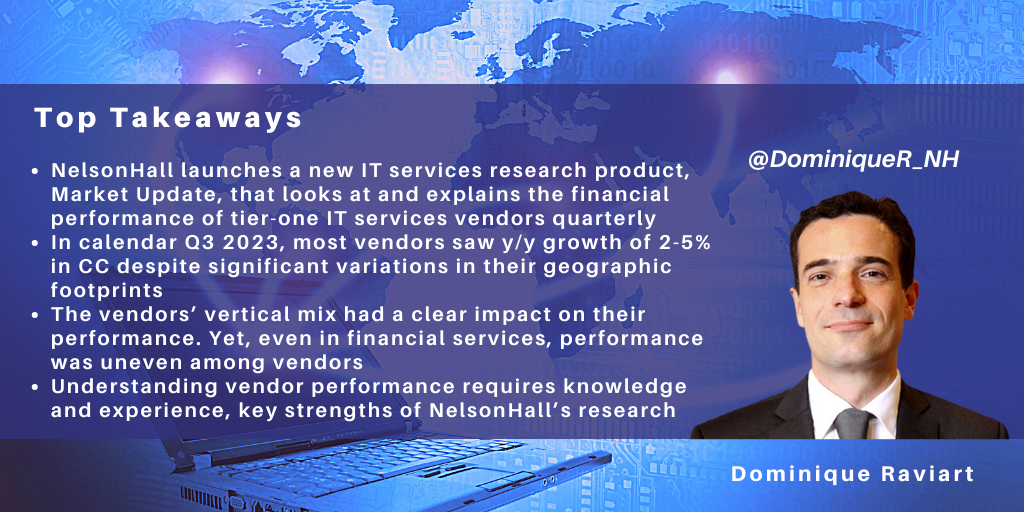

In Q3 2023, NelsonHall launched a new IT services research product, Market Update[2], that looks at and explains the financial performance of tier-one IT service vendors in Q3 and compares their performance. There was a strong pattern of these vendors seeing decelerating constant currency (CC) revenue growth in the quarter.

Most vendors saw y/y growth of 2-5% in CC, and this, despite significant variations in their geographic footprints. For instance, TCS and Capgemini have different geographic mixes (TCS derives ~52% of its revenues from clients in North America; Capgemini: ~61% from clients in the U.K./Europe), yet they saw similar y/y revenue growth (TCS: +2.8% in CC, Capgemini: +2.3% in CC). Notably, although the U.S. continues to be soft, vendors with a dominant North American footprint did not underperform those (e.g., Capgemini and CGI) stronger in the U.K./Europe.

The vendor's vertical mix had a clear impact on their performance in the quarter. Vendors exposed to softness in the high-tech, financial services, retail & CPG, and North American telecom sector suffered more than their peers with a greater presence in the following sectors: government, U.S. healthcare, energy & utilities, and manufacturing. For instance, CGI was resilient in the U.S. in Q3 thanks to its government and healthcare footprint. However, a vendor's vertical mix is not the only factor explaining its topline performance in the quarter. There are other reasons: not all verticals are global.

Banking is an example of an industry impacted by the same factors globally (e.g., stock markets, inflation). In contrast, buying behaviors of IT services in sectors such as healthcare and telecoms tend to be more regional and have different dynamics. While healthcare is largely commercial in the U.S., it tends to be part of the public sector in the U.K./Europe.

Even in a global industry such as financial services, performance has been uneven: HCLTech's BFSI revenues were up 12.5% y/y in CC in Q3, while almost all its competitors experienced negative growth. Overall, vendors are still hit by mortgage slowdowns, and demand has also fallen in asset management, investment banking, cards, and payments. Some vendors will win out in the medium term from large vendor consolidation deals. Unsurprisingly, Insurance has been more resilient.

Big Deals Made the Difference

Several vendors have a track record in large deals, accepting competitive pricing for those in open tenders and the ability to raise their profitability. Other vendors emphasize they are being "selective" in their contract pursuits.

There is no silver bullet for understanding the various factors underlying the performance of different IT services vendors. It requires domain knowledge and experience combined with detailed knowledge of individual IT services providers' capabilities and financial performance: these are strengths of NelsonHall's research. Don't hesitate to contact Guy Saunders or Darrin Grove to connect with NelsonHall.

[1] See our IT Services – Market Update, for NelsonHall subscribers

[2] See the recent Quarterly Update, for NelsonHall subscribers.

NelsonHall recently visited the TCS Pace Port innovation center in Amsterdam, the first Pace Port opened by TCS in Europe in May 2021 following a delay caused by the pandemic.

TCS is not unique in having opened facilities designed to foster collaboration and innovation to address clients' business challenges and new requirements. In itself, the broad concept of the Pace Port can be seen in all the leading IT services majors that have opened innovation centers. But not all these facilities have been well designed. Furthermore, the extent to which some are able to support their company's underpinning capabilities or broader positioning can vary. At their very worst, some of the earlier innovation centers visited by NelsonHall have been reminiscent of lipstick on a pig.

TCS Pace Ports Used to Gain Commitment from Key CXO Stakeholders

For TCS, the Pace Port is a key asset. In an approach that is characteristic of the company, expansion of the network has been considered rather than hasty: a second Pace Port in Europe opened last year in Paris, and before the end of this year, TCS will be opening one in London: this will be the eighth globally.

TCS' latest annual report has the slogan ‘Innovate.Adapt.Thrive’, a clear response to the current volatile economic and political environment.

Where a few years ago, TCS was primarily targeting what it called 'Growth and Transformation' (G&T) initiatives by large enterprises (typically large scale and multi-service line opportunities including advisory services, application migration and modernization and data-driven analytics), today there is also a focus on being well positioned for securing work where the client's discretionary budgets are curtailed or uncertain, engagements where the focus is on shorter-term cost and optimization propositions, typically improving business efficiencies. Accordingly, while supporting its clients' growth and transformation initiatives remains very important to TCS, the company increasingly positions itself as an ‘all-weather’ partner, with Pace Ports supporting both types of opportunity.

Potentially more valuable to service providers for sustaining long-term and expanding relationships are short, discrete engagements where they can deliver a demonstrable value add to the client's business – transforming perhaps, but not a full-blown enterprise-wide G&T initiative. Being close to the client, having a detailed understanding of their business environment, possessing broad industry domain knowledge, and having access to stakeholders outside the CIO office are all critical to this. To be seen by your major clients as a full-service partner capable of supporting them in their digital transformation journeys requires both CIO and CXO access. And the TCS Pace Port is a key element in this. See our blog on the TCS Pace Port in New York: TCS Pace: Integrating Capabilities to Drive Innovation - NelsonHall (nelson-hall.com).

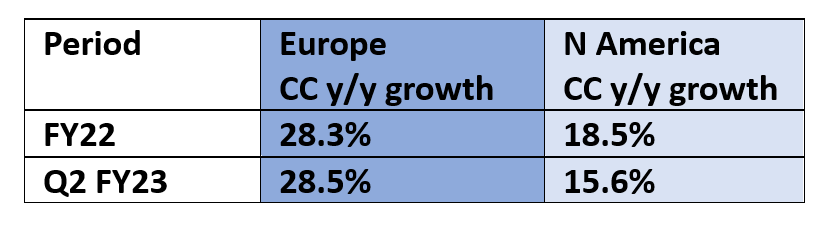

Amsterdam Pace Port Key to Driving Continental European Revenue Growth

TCS is today a significant player in Europe, generating nearly $4.2bn in revenues in the region in FY23, and its business in Europe is now roughly the size of its longer-established U.K. business. Perhaps surprisingly, TCS is only slightly larger than Infosys in Europe, although globally it generated nearly $10bn more in revenue in FY23 than Infosys. And recent CC growth in Europe has been trailing even the U.S., which is currently sluggish for everyone. Expect to see TCS Europe catch up over the next two years, getting closer to the strong growth the company has been enjoying in the U.K. And, in TCS fashion, this will not be achieved by acquisition activity, neither for scale nor for expertise, though captive carve-outs are always a possibility.

Within Europe, key regions for TCS are France, Germany, the Nordics, and more recently the Netherlands, where TCS aspires to be the largest systems integrator by revenue. The Amsterdam Pace Port is an important asset for this, as is TCS's role as the lead sponsor of the Amsterdam Marathon. In addition, its PACE Internship Program in Amsterdam has a batch of students pursuing Masters in Innovation & Digitalization.

TCS has ~300 clients in Europe, having doubled the number of new clients yearly since 2020. It has a nearshore presence in seven European countries, with major hubs in Hungary and Poland.

Key sectors in Europe for TCS include the obvious suspects of banking & financial services, insurance, and pharma/chemicals, also retail and postal services. TCS is also becoming more active in the transportation sector. Recent major deals include ones with Athora Netherlands, Bayer, Tryg, bPost, PostNord, and Versuni (formerly Philips Domestic Appliances). Recent new logo wins include Bane NOR, Outokumpu, Equans, Sandvik, SKF, TaP, and Airbus.

In the U.K., TCS has 23K FTEs and works with 48 FTSE companies. The company is looking to develop greater presence in currently underserved sectors including general insurance, the public sector, education, wealth & asset management, and media.

Contextualization is a Key Pace Port Success Factor

TCS refers, like Accenture, to its Innovation Architecture, which comprises its:

- Foundational research, in areas such as deep learning & AI, robotics & autonomous systems, behavioral and social sciences, and data & decision sciences

- COIN (co-innovation network), includes 100+ academic partners and 2.5k start-ups

- TCS PACE philosophy and the Problem to Value (P2V) innovation value proposition

- The Pace Port facilities, which serve as physical manifestations of the PACE philosophy.

TCS Pace Port Amsterdam is a hub where TCS teams are able to co-innovate with European clients, guiding them through the discovery, definition, refinement, and delivery phases of innovation, leveraging rapid prototyping techniques. TCS describes its Pace Ports as ‘platforms to identify business triggers, drive innovation at speed and scale, and accelerate the problem-to-value journey’.

TCS works with the client to develop a portfolio of MVPs as demonstrable innovation examples that the client can use to harness wider commitment from within their organization, with MVPs delivered in 30/60/90 day cycles.

Models used by TCS in the Pace Ports include:

- The Agile Innovation Cloud (AIC), brings together consulting, design thinking, and TCS' ecosystem and technology capabilities. A team from the client organization and TCS work together in proceeding from business problem definition to ideation, taking a strong outcome/business value orientation and then selected agile development builds, using rapid sprints

- TCS and client teams periodically review AIC innovation outcomes to deliberate on and fund identified MVPs for production deployment. The model helps clients gain visibility and momentum

- The Clay Map, an innovation portfolio model based on thinking from Clayton Christensen (who was a board member of TCS). It serves as a guide for creating a balanced portfolio of innovation ideas.

Workshops at TCS Pace Ports always involve a senior business stakeholder who can influence the company's direction, not just the CIO. The aim is to help clients find consensus on common innovation objectives and harness attention from, and involvement by, senior execs to the innovation agenda. TCS recognizes that it needs to continue to do more to increase its levels of relationship with non-technical CXOs.

A key Pace Port success factor is contextualization, with TCS typically carrying out 6-7 weeks of preparation to prepare the ground with other members of the client organization prior to the session with the key stakeholders. Inclusion of cross-industry knowledge is important.

The TCS Pace Port in Amsterdam currently hosts ~2 clients per week.

Beginning to Use GenAI for Initial Idea Generation

Overall, there is a very clear focus on helping clients exploit emerging technologies like AI/ML, AR/VR, IoT, blockchain, and robotics in building rapid prototypes. At TCS Rapid Labs, niche technologies like AI/ML, AR/VR, IoT, blockchain, and robotics help build rapid prototypes, cutting down on the cost and time to innovate.

TCS provided sessions demonstrating its thinking and related IP in four areas: the future of retail, intelligent banking, railsense, and smart city. The future of retail demonstrated a vision for the creation of a retail store digital twin, done in aggregate across stores. At the same time, the rail demonstration provided a vision for an intelligent railway station, combining indoor and outdoor navigation, and an enhanced onboard traveler experience, including directing passengers to vacant seats.

TCS also demonstrated using GenAI for idea generation to stimulate discussions with executives. Senior executives can be reluctant to brainstorm in public. So GenAI is starting to be used to overcome any initial social difficulties, act as an alternative to the use of focus groups, and facilitate brainstorming conversations with stakeholders. TCS demonstrated the use of GenAI for idea generation for innovative approaches to chronic pain management. This used multiple personas to generate ideas for three scenarios: logical/low risk, creative, and disruptive/challenging the status quo.

Driving Client Innovation and Pace Usage with Innovation Funds

Innovation funds are a key mechanism for driving client innovation and Pace adoption, and TCS is now including these as addenda to MSAs, typically with a value of 1% of the overall contract. TCS typically contributes 2-5 personnel who create a backlog of ideas and create swim lines of projects.

TCS is also embedding TCS Pace into proposals to new clients.

However, TCS prefers to charge for every Pace project to ensure clients take these sessions seriously.

]]>

IBM Consulting recently held a two-day analyst event for its European business (a significant region for IBM Consulting). Against an ongoing backdrop of uncertainty for client organizations in many sectors, the tone overall is quietly confident, buoyed by recent client wins and progress in a number of internal initiatives.

At a similar event seven months ago, there were clear emphases on IBM Consulting’s partnership ecosystem and on underlying capabilities in consulting-led, garage-style engagements and industry knowledge in support of verticalized offerings. We noted at the time the obvious advantages in being part of the IBM group, including having access to a client base of large enterprises who are incumbents in their markets (and thus pushing for digital transformation), and of course the ease of collaborating with IBM Technology for its cloud and AI assets (see IBM Consulting Strengthening Partnerships to Drive Cognitive & Cloud Consulting Growth - NelsonHall (nelson-hall.com).

Unsurprisingly, the overarching message today is exactly the same. IBM Consulting continues to be a growth vector for IBM Group, delivering topline growth, both at the global level and in Europe, and margin improvement in 2022. Full-year IBM Consulting revenues of $19.1bn were up 14.9% in CC (up 7.1% as reported), with all three business areas (Business Transformation, Application Operations, Technology Consulting,) delivering double digit CC growth.

Recurring themes throughout the analyst event included:

- Macro offerings that look at organizations’ key priorities

- Ongoing development of strategic partnerships

- Key findings from the latest CEO study (under embargo at the time, now published).

Macro offerings around four themes that span the portfolio

At the recent IBM Think customer event, IBM Group launched its ‘Seven Bets’: recommended actions to take in response to seven trends (GenAI, sustainability, profit, digital products, CX, metaverse, the new social contract). Expect to see marketing across the group focus on these.

Meanwhile, IBM Consulting in EMEA has launched four macro campaigns, with various offerings bundled into broad themes that are high among clients’ current priorities:

- Cost and productivity

- Future proofing

- Customer and product transformation

- Sustainability.

Both business-led offerings (e.g., BPS, Talent & Transformation) and technology-led are covered within these four themes. There appears to be an increasing coherence in the value propositions across the company’s broad portfolio; a coherence that historically was not always the case.

Our note on the November 2022 event commented on a bigger push for large deals; a recent win which illustrates IBM Consulting competing against best-in-class opposition is a S/4HANA migration deal at Diageo, won against a well-established incumbent. Among other winning attributes, IBM Consulting highlighted its experience in SAP S/4HANA implementations in the CPG industry.

Strategic partnerships

IBM Consulting’s partnerships have become much richer in the last five years (when there was essentially just one strategic partnership: with SAP). In particular, the Kyndril spin-off has helped IBM Consulting to open up to hyperscalers, in particular with Microsoft Azure and AWS (each of which accounts for ~$1bn in revenues). In aggregate, IBM Consulting’s strategic partnership bookings were up over 50% in 2022, with Azure and AWS more than doubling. This emphasis on developing the partnership ecosystem is evident across all of IBM Group (for instance, in Q4 2022, a series of new IBM Software offerings were made available as-a-Service in the AWS marketplace, and Red Hat continued the expansion of its offerings in hyperscaler marketplaces). But the loosening of the strings to other IBM divisions introduced by Arvind Krishna has greatly benefited IBM Consulting.

We expect to see more types of partnership announcement in 2023/4, including those focused on industry solutions and those expanding its capabilities in generative AI. Indeed, the week after the analyst event, IBM Consulting announced an expansion of its partnership with Adobe, launching a portfolio of Adobe consulting services to help clients navigate the generative AI landscape, leveraging Adobe’s AI-accelerated Content Supply Chain solution. IBM Consulting recently announced its Center of Excellence for generative AI, part of IBM Consulting's much larger global AI and Automation practice, stating that the CoE has around 1,000 consultants with generative AI expertise. IBM Consulting emphasizes assets such as the IBM Garage for Generative AI, IBM’s agile approach to co-creating with clients, to help them fast-track innovation in foundation models for generative AI.

IBM 2023 CEO Study: Cost Take-Out Top Priority; GenAI Top of Mind

Several discussions over the two days of the event referred to key findings from IBM’s 2023 CEO study, under embargo until now, about their top priorities and challenges over the next two to three years.

This latest study finds that the highest priority of the CEOs surveyed is improved productivity or profitability. Product and service innovation has also jumped up in importance, to second place. Customer experience has been pushed down to third place. No great surprises there given current macroeconomic conditions. We noted that, reflecting the current demand by many organizations for their IT service providers to be able to deliver in-year cost savings, a number of presentations featured case studies illustrating IBM Consulting achieving this in different areas of their offerings portfolio, not just in obvious areas of cost take-out.

Another key finding of the study looks at the current pressures on organizations, across nearly all sectors, to adopt generative AI models. It highlights that where the majority of the CEOs surveyed express a high degree of confidence in their organizations’ capabilities to incorporate generative AI into processes and products, this confidence is not shared by other senior execs. This level of disconnect is arguably not surprising: it certainly plays to the need to work with external consultants.

One session at the analyst event briefly referred to potential GenAI use cases that IBM is exploring with clients. The most advanced work to date appears to be in the U.S. health sciences and health payer sectors. For one CPG major, IBM is helping set up a GenAI CoE which will develop use cases for internal processes. In the short term, this is likely to become a common type of engagement for the IT services majors, at least until clients’ organizational functions become more familiar with how they might leverage the GenAI core capabilities of semantic search, summarization and content creation in their operations.

The quality of the client presentations talking of their experience of working with IBM was uniformly high, something that we feel is increasingly rare in these events.

There has been one organizational change since November, one that comes as no surprise: cybersecurity consulting now sits in IBM Consulting (see also our note from last week: IBM Converging Risk Scores to Optimize Cybersecurity Offering - NelsonHall (nelson-hall.com)

So what next for IBM Consulting in EMEA? The company’s recent M&A activity has centered on the U.S. – Europe and the U.K., both more buoyant markets, have not really featured. We expect this to change in the next 12 months.

]]>

We recently attended Infosys’ EMEA CONFLUENCE flagship client event and found the company quietly bullish about recent and projected performance in the region.

Europe remains a growth market for Infosys

Salil Parekh made it clear some years ago that he wanted to grow Infosys’ business in Europe, and the results are there to see.

Europe now accounts for 25% of Infosys’ global revenues and continues to be a growth market for the company, delivering substantially higher CC growth than North America:

N.B. Softness of European currencies against the U.S. dollar has meant that this has not translated into higher reported growth than N. America.

Sectorially, the business mix is significantly different from North America. Over two-thirds of revenues in Europe come from three vertical groups:

- Manufacturing: by far the largest, accounting for 28% of the region’s revenues (compared with under 13% globally). To take one sector, automotive, clients include Daimler (a top 3 account globally), Volvo Cars, and Mercedes Benz

- Financial services: at 21%, significantly less than the U.S. Clients include BNP Paribas and Deutsche Bank

- E&U, Resources and Services: 19% (compared with 12% globally). Clients include E.ON and Uniper.

Recent expansion of localization

The region is served by 19.4k personnel, of whom 71% (nearly 13.8k) are based locally (including those on visas). While it was mentioned as a priority when Salil Parekh arrived as CEO nearly four years ago, momentum to increase localization in key European geographies has been more recent.

In France, for example, the proportion of personnel who are local hires has increased from just 25% in FY20 to 47% in FY22 and should hit 50% this year. In support of this, Infosys has introduced new internship programs in France and grad recruitment programs in selected universities.

Infosys is now looking for new growth opportunities in Europe in 2023 to come from:

- Expansion in the Nordics

- Expansion in the region of its creative, branding, and experience design business, leveraging the recent acquisition of oddity

- Large deals, account expansion, and new account openings.

The Nordics

Infosys already has some marquee clients headquartered in the Nordics, for example, KONE, Telenet, and Posti, and is looking for faster growth in the region.

In Sweden, it has just opened a new proximity center in Gothenburg, its sixth in Europe.

Its recent acquisition of BASE life science, a LS sector technology consultancy headquartered in Denmark, brings expertise in medical, digital marketing, clinical, regulatory, and quality and data science (focused on data and AI in clinical trials and drug development). Infosys intends for BASE to expand its expertise into the consumer health, animal health, MedTech, and genomics segments. BASE has partnerships with Veeva, IQVIA, and Salesforce and enjoyed strong growth in recent years. The acquisition, for around €110m including earnouts, augments Infosys’ life sciences expertise, a sector where it has arguably been under represented and which continues to enjoy strong growth.

Its acquisition four years ago of Fluido brought in substantial local Salesforce capabilities: as well as a Platinum consulting partner, Fluido is a Salesforce training delivery partner in the Nordics. Fluido brought in ~240 employees and offices across Finland (Espoo); Sweden (Stockholm & Gothenburg); Norway (Oslo); Denmark (Copenhagen); and Slovakia (Banská Bystrica).

Expect to see more bolt-on acquisition activity by Infosys of specialists in the region, and some larger-scale personnel transfer outsourcing deals.

Internationalizing oddity

Infosys’ recent acquisition (for up to €50m including earnouts, etc.) of oddity, a Germany-based digital marketing, experience, and commerce agency, strengthens its creative, branding, and experience design capabilities in central Europe. As part of Infosys’ digital experience and design offering, oddity will become part of WONGDOODY. This is a sizeable acquisition by Infosys to expand WONGDOODY into Central Europe. oddity, which will rebrand as WONGDOODY, comprises four specialist units in Germany (plus a 40-person operation in Taipei and Shanghai and a software development team). As well as bringing an onshore presence in Germany to WONGDOODY, it beefs up WONGDOODY’s capabilities in branding, and the oddity waves unit adds some 3D/CGI production capabilities.

While WONGDOODY in Europe has worked for Infosys IT services clients such as Telenet and BPost, there remain significant opportunities for Infosys to leverage WONGDOODY to expand its relationships with clients outside the CIO function in supporting their digital transformation initiatives.

Sales: large deals/account expansion/new account openings

Large deal wins have played a major part in fuelling Infosys’ topline growth since 2018, with Europe having some significant recent deal wins with the likes of Telenor, Deutsche Bank, Volvo Cars, and Curry’s. Infosys claims its current pipeline for large deals in Europe is particularly strong.

Infosys’ TITAN account expansion program has yielded results in the increased number of $50-100m accounts globally, from 26 at end FY22 to 38 at end H1 FY23 (the number of $100m+ accounts staying stable at 39). With enterprises being more cautious in awarding huge multi-year transformational contracts, the focus is now on expansion within high-potential accounts in the $10-50m revenue range and getting them closer to that $50m area.

With sales hunting initiatives, there has been considerable success in winning new marquee accounts in Europe: of the 52 new clients landed over the last 18 months that each have revenues of $10bn+, Europe accounts for 21 (over 40%). Many of these are $10m+ TCV deals. Infosys claims its pipeline of $10m+ deals from new accounts remains strong. Some of these are potential vendor consolidation initiatives: initiatives that we expect to see more of as attrition levels continue to fall.

Unsurprisingly, current demand is dominated by cost take-out themes such as infrastructure modernization and Tech & Ops deals. Looking ahead, Infosys is interested in captive acquisitions and is also likely to benefit when vendor consolidation initiatives increase.

Planned technology investments in Europe reflect the focus on manufacturing sectors; areas of interest include private 5G for IIoT use cases and smart factories. At the moment, Infosys has two innovation centers in Europe (in Dusseldorf and Bucharest, which is also a cyber defense center) and two design studios (Dusseldorf again and London). Expect to see a few more opening over the next 24 months, with perhaps more of an industry emphasis in some of these.

]]>

IBM Consulting recently held its first analyst and advisor event in Europe since IBM’s spin-off of its Global Technology Services infrastructure business (now Kyndryl) and the renaming of the former IBM Global Business Services division to IBM Consulting just over a year ago.

When IBM had announced its intended spin-off of the GTS division in October 2020, new CEO Arvind Krishna declared this would free up the rest of IBM to focus on the higher margin, higher growth hybrid cloud market (notably the RedHat OpenShift business) and its cognitive computing businesses. IBM Consulting has also benefited from other recent developments, and the business now looks more relevant as a major IT services business, and less of an add-on to IBM Technology businesses.

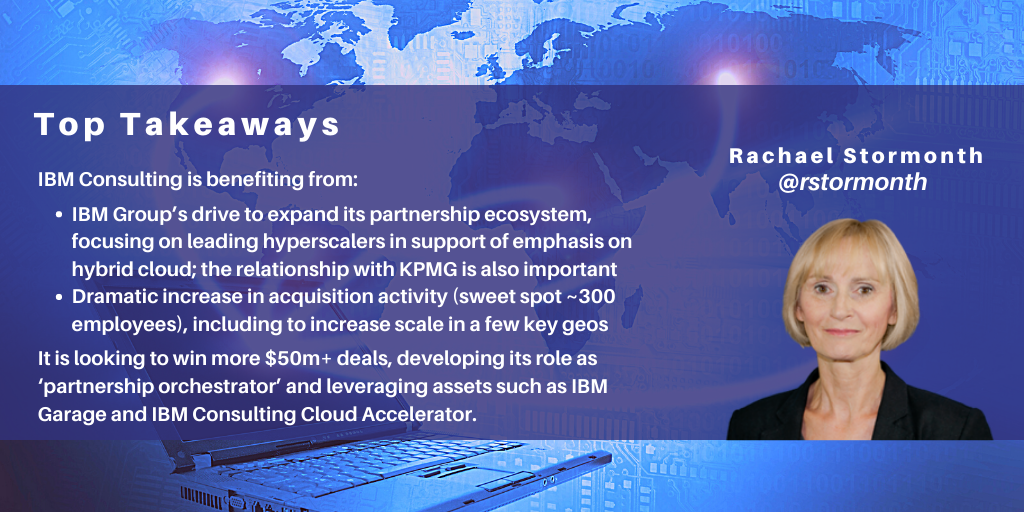

Partnership Ecosystem

A key priority across the group has been expanding IBM’s partnership ecosystem. An example of this is Infosys BPM’s recent opening of a Center of AI and Automation in Poland, in collaboration with IBM, following several years of joint work in identifying new use cases and building solutions to enable clients to innovate in hybrid cloud environments.

For IBM Consulting, this increased emphasis on developing the partnership ecosystem includes a particular focus on AWS and Microsoft Azure and increasing the number of certifications (reaching 17k certifications in AWS, 33k in Azure by end FY22); and of course, IBM Cloud (7k certifications). The Kyndryl split and the ecosystem play have broadened opportunities for IBM Consulting to work with the likes of AWS: that is now a $1bn business, and IBM Consulting’s alliance program is aiming to make each of its strategic partnerships $1bn businesses like AWS. IBM Consulting emphasizes that it no longer promotes IBM Technology as a priority. Nevertheless, Red Hat remains an important revenue driver, with IBM Consulting claiming the #1 Red Hat service partner position.

As well as partnerships with hyperscalers and the major ISVs, IBM Consulting’s relationship with KPMG is notable: this has been important in providing access to line of business heads such as CFOs for business transformation discussions; expect to hear more about this relationship.

IBM Consulting claims its partnership relationships have evolved from 1:1 deal-specific relationships that was the norm just 18 months ago and that today, 60% of its engagements involve technology solutions from several partners. In a somewhat ambitious claim, IBM Consulting says that moving into 2023 it is aiming to develop its role as a partnership ‘orchestrator’ in deals involving multi-vendor solutions, responsible for managing T&C complexities.

Managing Recent Growth, including Increased Acquisition Activity

IBM Consulting has been a growth vector for IBM, delivering topline growth of around 16% in the last four quarters, of which around 14% is organic. Hybrid cloud is clearly the growth vector, delivering 28% topline growth, led by activity in Technology Consulting around application modernization on the hybrid cloud with Red Hat OpenShift.

IBM Consulting is benefiting from a dramatic expansion in acquisition activity since the arrival of Arvind Krishna as CEO. Notably:

- Some transactions have brought in specific skills such as Microsoft Azure specialist NeuDesic (1500+ personnel) and Nordcloud (cloud advisory and cloud management with 430+ certifications across AWS and Azure)

- Others have increased IBM Consulting’s scale in geographies where it is light, including France and Spain in Europe; for example, Bluetab Solutions Group, which has brought in ~700 employees, many of them based in Spain.

Expect to see more acquisition activity of both types. While the recent downturn in company valuations is likely to spur inorganic growth, IBM Consulting is unlikely to pursue any very large transactions but continue to focus on companies with a few hundred rather than thousands of employees.

In terms of the underlying organic growth, the change of name from GBS to IBM Consulting has been helpful with recruitment, making the company a more attractive prospect for personnel attracted by the notion of ‘consulting’ and working with clients.

IBM Consulting has grown from 120k to 160k employees over the last 18 months. Across the workforce, there is a strong focus on skills development with an emphasis on badging/certifications. We heard of 40k cloud certifications recently, 23k Microsoft Azure badges, 15k AWS and 30k SAP. In support of this drive, compensation is now linked to skills rather than to performance – which of course demands accurate workforce planning. We are seeing a growing trend by IT services providers to increase the level of bonus attached to skills competencies: IBM Consulting appears to be pushing this hard.

Looking for More $50m+ Deals

IBM Consulting is taking a vertical, rather than geography-based GTM approach, and is looking for larger deals ($50m+). In support of this, there is a strong emphasis on assets such as:

- IBM Garage: IBM Consulting claims it is now being used in two-thirds of engagements. While there are broad similarities to approaches that have been developed by other leading large systems integrators in recent years, IBM Consulting is finding its Garage methodology a differentiator in its pursuit of larger deals

- IBM Consulting Cloud Accelerator, which it describes as a ‘cloud acceleration platform designed to orchestrate a collection of expert rules, tools, technical assets and industry solution starter kits to drive rapid planning and low-touch execution for hybrid cloud journeys’. The platform houses a repository of assets and tools across home-grown catalogs and IBM products, open-source and third-party vendors. Expect to hear more about how IBM Consulting has used this with clients.

IBM Consulting’s emphases on consulting-led, garage-style engagements, its partnership ecosystem, and industry knowledge in support of verticalized offerings are not massively dissimilar from other large leading services providers. There are obvious advantages in being part of the IBM group, including having access to a client base of large enterprises who are incumbents in their markets (and thus pushing for digital transformation), and of course the ease of collaborating with IBM Technology for its cloud and AI assets.

But overall, IBM Consulting was at pains to emphasize how much it has changed its technology ecosystem priorities in the past two years. We welcome this: the past few decades show that IBM’s conglomerate approach to IT has not particularly led the growth of its services activities, whereas now IBM Consulting is able to benefit from the momentum in AWS and Microsoft Azure. Kyndryl of course remains an important partner, not least because of the shared client base and its status as a tier-one managed mainframe service vendor. However, the Kyndryl partnership will possibly become more transactional as IBM Consulting relies more heavily on its own investments in AIOps.

We believe that IBM Consulting is beginning to distinguish itself more clearly from IBM Software and Infrastructure. Its expanded partnership ecosystem, assets such as IBM Consulting Cloud Accelerator, the development of more industry-specific playbooks, and a more organized approach to winning large deals will all help fuel future growth. That is not to say there are pockets of the portfolio that are in the shadows. With the exception of Talent and Transformation, there is perhaps more work to be done in messaging around some of the ‘Business Transformation’ offerings.

]]>

In its Q3 FY22, TCS delivered its sixth consecutive quarter of organic growth around the 15% mark. Despite the uncertain macroeconomic background, TCS has a strong pipeline for at least the next two quarters and has yet to see any softening in the market. For example, it was expecting some softening in Europe in the September quarter but instead achieved both increased revenue growth and a strong order book.

Nonetheless, enterprises are typically starting to focus more on execution rather than envisioning and on programs with a clear, well-defined set of outcomes. TCS perceives that some enterprises might be becoming more realistic about some of their more fanciful projects with long-term RoI. This perception ties in well with recent NelsonHall research, which shows a continuing high emphasis and level of intention for short-term transformations with high RoI, but with some longer-term projects with less certain RoI being put on hold.

TCS is not experiencing widespread vendor consolidation within accounts but is seeing some increase in share within some of its major clients as they push incremental business towards the stronger vendors in their vendor portfolios.

Renewed Travel also Boosting Client Relationships

The normalization of travel is also now working in TCS’ favor. During lockdown and travel restrictions, TCS had to extensively use contractors for minor roles needing personnel onsite at client locations for periods of, say, 3-4 months. Now TCS is reverting to sending visa holders from India, which has the triple benefit of improving both customer and employee satisfaction and delivering cost reduction.

Nevertheless, like its peers, TCS still faces the widespread issue of managing the return to the office. Employees in IT services companies typically became very comfortable working from home during the pandemic, but companies are finding that this has had an impact on company culture and strength of allegiance, among other things. However, managing the return to the office has to be done carefully in order to avoid alienating staff. TCS’ approach is to request middle and senior-level personnel to typically work in the office most days, encouraging attendance by more junior personnel, some of whom now go into the office 2-3 days per week, and others continuing to work primarily from home.

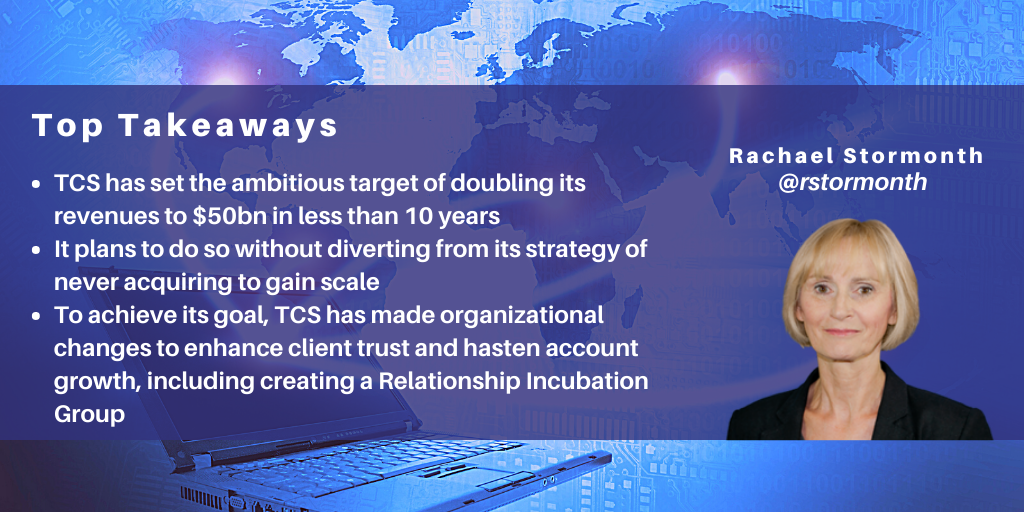

Pursuing Bold Ambitions

In a departure from its traditional reticence, the TCS management is now openly referring to ambitions for the company to reach $50bn in annual revenue – and to do so without diverting from its strategy of never acquiring to gain scale.

TCS is looking to get to $50bn in less time than it took to move from $10bn to $25bn, a period of 10 years. This is an aggressive target, particularly given TCS’ emphasis on organic growth. However, with technology valuations softening, TCS may become more active in acquiring for new capabilities: any such transactions would be bolt-ons. After reaching $5bn in FY08, TCS has typically taken around three years to add each subsequent $5bn to its revenues, reaching $10bn in FY12, $15bn in FY15, $20bn in FY19, and now $25bn in FY22.

Changing the Organizational Structure to Enhance Client Trust and Hasten Account Growth

To achieve its goal of getting to $50bn in less than ten years and facilitate account revenue growth, TCS has made some changes to its organizational structure and adopted a novel, confident and distinctive approach to handling different tiers of accounts.

Firstly, it has taken steps to reduce the delivery uncertainty that enterprises can have when they have modest spend with a new vendor. Previously, TCS’ account management was verticalized, with the potential danger of business unit heads focusing on the higher revenue accounts to the detriment of the lower revenue accounts. All TCS mainstream accounts are typically Global 2000 enterprises, so even the lower revenue accounts have massive potential.

To address this issue and make smaller accounts feel they are important to TCS, it has created a new business group, Relationship Incubation Group. This group works with the ~500 newly acquired clients using a high-touch engagement model to overcome delivery anxiety and build a foundation of trust. The new unit is horizontal rather than vertical and is organized geographically into “small regions” with regional managers. It strongly focuses on delivery and client handholding and avoids cross-selling and up-selling.

Once trust is established, and account revenues are, say, $5m to $10m, the governance of the account transfers to Enterprise Group, which is geared to upselling and cross-selling to facilitate clients consuming a much wider range of TCS services and accelerate revenue growth in each account. This group adopts TCS’ traditional account management approach and is entirely verticalized.

Finally, the largest clients, those with over $100m spend with TCS and who view TCS as a trusted transformation partner, are governed by TCS’ Business Transformation Group. TCS currently has 59 clients that generate at least $100m in annual revenue, an impressive number that will clearly continue to increase.

TCS is not a company that regularly states bold ambitions, but when it does those ambitions are invariably achieved: the only question is when TCS will reach its $50bn target. Will it be as early as FY27?

]]>

Dominique Raviart gives his reaction to today's announcement by Atos, who issued its second profit warning in seven months.

]]>

With a new Chairman appointed 15 months ago and a new CEO in place for the last four, Wipro has seen a significant changing of the guard – much has been made of the fact that Thierry Delaporte is Wipro’s first non-Indian CEO appointment. The announcements made in a recent event for financial analysts (its first such event in five years) reveal some major shifts happening within the company. Some of these are course corrections, others are more radical changes: all are initiatives that we believe will help improve Wipro’s competitiveness over the next few years.

Each of the initiatives discussed below is designed to support what Chairman Rishad Premji highlights as a new ‘obsession for growth’ at Wipro:

- Nurturing new culture

- Change in operating model to improve client proximity: structure, the GAE

- Prioritizing (and de-prioritizing) target markets

- Formalizing approach to large deals

- Increasing M&A.

Culture Change

Admitting publicly that you are looking to drive a major shift in culture, while of course retaining core values (the ‘spirit of Wipro’) is brave, as it acknowledges that changes need to be made. It is not appropriate to comment here on perceptions of the legacy culture at Wipro, but the success of this new drive to nurture a culture that has more of a growth mindset is arguably critical to Wipro’s future success. In its attempts to drive cultural transformation across the company, Wipro has elected to adopt a top-down approach, appointing a Chief Culture Officer at SVP level, and encouraging its leaders to be advocates by exhibiting five ‘habits’ in action.

The five habits to be espoused by all Wipro employees are:

1) Being respectful

2) Being responsive

3) Always communicating

4) Demonstrating stewardship of the company (rather than focusing on individual priorities)

5) Building trust.

In sum, the application of these attributes should have clear benefits. For example, internally, it should lead to less of a hierarchical feel within teams and units, more consistency in work practices across the organization, stronger communications and teamwork, and also help with global diversity. And in relationships with clients, it should support Wipro’s ambition to be regarded more as a champion challenger by them, rather than being judged just on its abilities in execution.

Like all the major IT services players, Wipro has been assiduously rolling out talent re-skilling programs for some years now. These efforts will continue and be intensified. In addition, and reinforcing the ambitious culture change, we should also expect to see much more diversity at Wipro, including (and presumably not limited to) nationality and gender. Having a more diverse workforce, which will require changes in hiring practices and HR policies, will be a critical element in Wipro’s efforts to improve client proximity and reinforce portfolio development, and, importantly, become an employer of choice.

Change in Operating Model: ‘Simplicity over Perfection’

In short, Wipro is introducing a much simpler operating model, with effect from January 1.

The primary P&L will be four strategic market units (SMUs):

- Americas 1, organized by sector and covering all of Wipro’s major target verticals. Headed by Srini Pallia (was President, Consumer business vertical)

- Americas 2, also organized by sector, including BFSI, manufacturing, hi-tech, E&U. Headed by Angan Guha (was head BFSI vertical)

- Europe, organized by region: UK & Ireland, Switzerland, Germany, Benelux, Nordics, Southern Europe. Head to be announced

- Asia Pacific, Middle East & Africa (APMEA), also organized by region: Australia/ New Zealand, India, West Asia, South East Asia, Japan, South Africa. Headed by NS Bala (was President E&U vertical).

So, what is Wipro looking to achieve by moving away from a vertical-led operating model to a geography-led one, just as Accenture has done recently (also following the arrival of a new CEO)?

Firstly, the move to this model is intended to improve client proximity, particularly outside the U.S. Delaporte acknowledges that one challenge Wipro is facing (one that we have noted for years in our Key Vendor Assessments on the company) is that its revenue growth has remained largely dependent on the U.S. market: apart from the U.K., which accounted for around 10% of global revenues last FY, Wipro has lagged most of its peers in scaling in other key growth markets. In FY20, for example, just 8% of its global revenues (~$660m) came from Eurozone countries, led by Germany and France. Even excluding the impact of COVID-19, Wipro has underperformed in Europe in recent years: looking ahead, Delaporte is looking for Europe and APMEA to contribute around 50% of Wipro’s incremental revenues globally over the next few years.

Secondly, the new model is much simpler than the one it is replacing. A less centralized model with fewer P&Ls should mean more accountability at the local level, faster decision making, for example in deal pursuits, and more agility generally.

Thirdly, Wipro intends to be more selective in prioritizing specific sectors within its identified target markets. Delaporte cites as an example Switzerland, where Wipro’s focus will be Life Sciences, BFSI, Heavy Industries and Consumer. The SMU leads having oversight of industry sector coverage within their regions should enable a more focused approach in prioritizing specific markets at a regional and even country level. This is a move from an approach that has typically looked at sectors through U.S.-centric lenses; Europe and APMEA in particular are expected to benefit from a more regional approach to target sectors and a more intimate grasp of local markets.

The four SMUs are supported by just two global business lines (GBLs):

- Integrated Digital, Engineering & Application Services (iDEAS), includes domain and consulting, applications & data, engineering and R&D and Wipro Digital. Headed by Rajan Kohli (was president, Wipro Digital)

- iCORE, includes Cloud & Infrastructure Services (CIS), Wipro Digital Operations & Platforms (DOP) and Cybersecurity & Risk Services (CRS). Headed by Nagendra Bandaru (was President cloud, IT infrastructure services, and DOP).

The GBLs house Wipro’s industry domain capabilities in addition to the service line practices and delivery.

As with the go-to-market, Delaporte is introducing simplicity into portfolio management and the delivery model. (Wipro has been reporting along six industry groups and five practices).

One obvious benefit is improved economies of scale.

Moving to just two GBLs should also help in prioritizing portfolio investments, with a focus on developing integrated offerings that span different practices and are designed to address clients’ business challenges or help them in creating new digital business models: ones that are what he calls ‘at the intersection of strategy, design and technology’. This will be an important move for Wipro: our perception is that Wipro Digital was not well integrated with the rest of the company, limiting the company’s ability to position strongly to clients looking for innovation or transformation partners. Similarly, the new model should also assist efforts to target business stakeholders beyond the CIO.

Unsurprisingly, some Wipro execs are leaving, including Milan Rao and Bill Stith at the end of the year, and Bhanumurthy BM and Anand Padmanabhan over the next few months – but so far, the number is relatively low for a change of CEO and a strategic refresh. As well as new roles such as the Chief Growth Officer, we do expect to see much greater diversity in the regional leadership soon.

Formalizing Approach to Strategic Clients & Large Deal Pursuits

A move to strengthen large account management was to be expected, as Wipro has for many years been lagging its Indian-oriented peers in the number of very large accounts. While FY18 saw a big jump in the number of $100m+ accounts (up from 10 to 15, since slipped back to 13), there has essentially been no movement in the number of $75m+ p.a. or $50m+ accounts since FY18. At end Q1 FY21 (the last quarter before the pandemic began to hit), Wipro had 39 $50m+ accounts (exactly the same number as in FY18), compared with 100 for TCS` and 61 for Infosys.

Wipro’s MEGA and GAMMA accounts currently contribute around 70% of its revenue. Delaporte is looking to accelerate growth in these accounts by more formally centering the organization around the client through a new role. The Global Account Executive (GAE) not just represents Wipro in the account but, importantly, manages that account, supported by industry and technology specialists and delivery managers. Delaporte claims this to be the ‘most important pillar’ for accelerating growth at Wipro, and the GAE the most important role in the new organization. A reflection of its influence and accountability, it is just two layers below the exec committee. His target is for GAEs to constitute 25% of Wipro’s top 200 leaders within a few years.

In addition to strengthening key account management, Delaporte is looking to improve Wipro’s ability to target and land new transformational opportunities. He has acknowledged Wipro has had ‘mixed results’ in winning large deals in recent years; he hopes to improve this by setting up a large deals team that has expertise in deal structuring, including financial and commercial modelling, as well as solution development. We think this is likely to involve external hires of people with relevant experience.

Overseeing the roll out of the GAEs and the build out of the large deals team is the Chief Growth Officer, a new role, and one that is also likely to be an external hire. She or he will also have oversight of strategic alliances; unsurprisingly, there will be a push to deepen and scale existing partnerships with the likes of AWS, Microsoft, Google, Salesforce, SAP and ServiceNow. Expect to see an increase in the number of partner-centric CoEs in support of this.

M&A

Until the last few quarters, Wipro had been relatively quiet on the M&A front for a few years, since Appirio in 2016 and DesignIt in 2015. Expect to see an acceleration in M&A as Wipro looks to expand local capabilities in its target regions in platforms such as Salesforce and ServiceNow and, like Eximius Design, in engineering services in the areas of IoT, Industry 4.0, edge computing, and 5G.

Some of Wipro’s historic acquisitions had not exactly been success stories and here again there appears to be an awareness that a more structured approach is called for: it is setting up a new post-merger integration team which should help in driving synergies and in presenting a joined up face to clients and in its go-to-market.

Of the initiatives that Delaporte is introducing, some might seem on first consideration a little bold, but there is a clear design that seeks to address a range of company-specific challenges that have impeded Wipro’s growth in recent years and boost its abilities to position for the newer types of opportunities that it, and its peers, are targeting.

2021 could mark the commencement of a much stronger performance at Wipro.

]]>

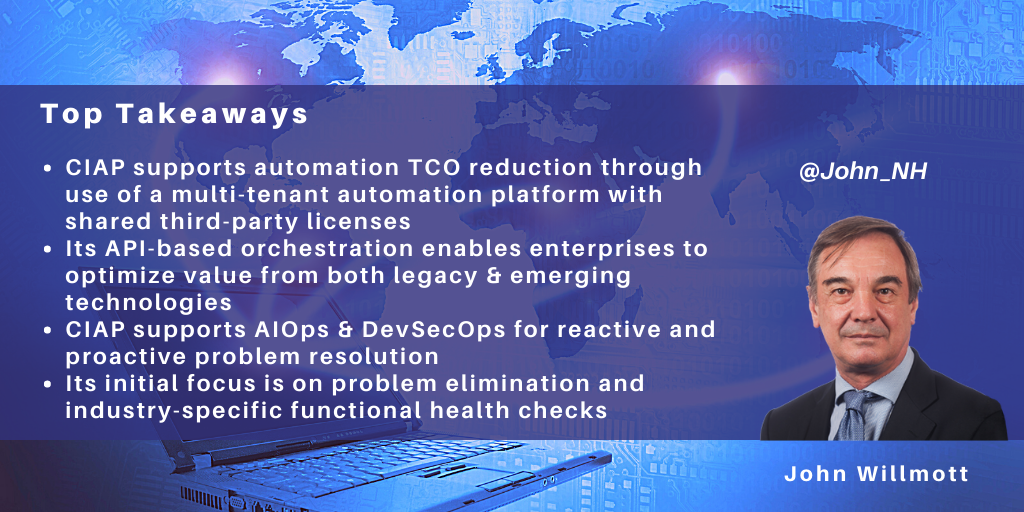

Capgemini has just launched version 2 of the Capgemini Intelligent Automation Platform (CIAP) to assist organizations in offering an enterprise-wide and AI-enabled approach to their automation initiatives across IT and business operations. In particular, CIAP offers:

- Reduced TCO and increased resilience through use of shared third-party components

- Support for AIOps and DevSecOps

- A strong focus on problem elimination and functional health checks.

Reduced TCO & increased ability to scale through use of a common automation platform

A common problem with automation initiatives is their distributed nature across the enterprise, with multiple purchasing points and a diverse set of tools and governance, reducing overall RoI and the enterprise's ability to scale automation at speed.

Capgemini aims to address these issues through CIAP, a multi-tenanted cloud-based automation solution that can be used to deliver "automation on tap." It consists of an orchestration and governance platform and the UiPath intelligent automation platform. Each enterprise has a multi-tenanted orchestrator providing a framework for invoking APIs and client scripts together with dedicated bot libraries and a segregated instance of UiPath Studio. A central source of dashboards and analytics is built into the front-end command tower.

While UiPath is provided as an integral part of CIAP, CIAP also provides APIs to integrate other Intelligent Automation platforms with the CIAP orchestration platform, enabling enterprises to continue to optimize the value of their existing use cases.

The central orchestration feature within CIAP removes the need for a series of point solutions, allowing automations to be more end-to-end in scope and removing the need for integration by the client organization. For example, within CIAP, event monitoring can trigger ticket creation, which in turn can automatically trigger a remediation solution.

Another benefit of this shared component approach is reducing TCO by improved sharing of licenses. The client no longer has to duplicate tool purchasing and dedicate components to individual automations; the platform and its toolset can be shared across each of infrastructure, applications, and business services departments within the enterprise.

CIAP is offered on a fixed-price subscription-based model based on "typical" usage levels, with additional charges only applicable where client volumes necessitate additional third-party execution licenses or storage beyond those already incorporated in the package.

Support for AIOps & DevSecOps

CIAP began life focused on application services, and the platform provides support for AIOps and DevSecOps, not just business services.

In particular, CIAP incorporates AIOps using the client's application infrastructure logs for reactive and predictive resolutions. In terms of reactive resolutions, the AIOps can identify the dependent infrastructure components and applications, identify the root cause, and apply any automation available.

CIAP also ingests logs and alerts and uses algorithms to correlate them, so that the resolver group only needs to address a smaller number of independent scenarios rather than each alert individually. The platform can also incorporate the enterprise's known error databases so that if an automated resolution does not exist, the platform can still recommend the most appropriate knowledge objects for use in resolution.

Future enhancements include increased emphasis on proactive capacity planning, including proactive simulation of the impact of change in an estate and enhancing the platform's ability to predict a greater range of possible incidents in advance. Capgemini is also enhancing the range of development enablers within the platform to establish CIAP as a DevSecOps platform, supporting the life cycle from design capture through unit and regression testing, all the way to release within the platform, initially starting with the Java and .NET stacks.

A strong focus on problem elimination & functional health checks

Capgemini perceives that repetitive task automation is now well understood by organizations, and the emphasis is increasingly on using AI-based solutions to analyze data patterns and then trigger appropriate actions.

Accordingly, to extend the scope of automation beyond RPA, CIAP provides built-in problem management capability, with the platform using machine learning to analyze historical tickets to identify the causes and recurring problems and, in many cases, initiate remediation automatically. CIAP then aims to reduce the level of manual remediation automation on an ongoing basis by recommending emerging automation opportunities.

In addition to bots addressing incident and problem management, the platform also has a major emphasis within its bot store on sector-specific bots providing functional health checks for sectors including energy & utilities, manufacturing, financial services, telecoms, life sciences, and retail & CPG. One example in retail is where prices are copied from a central system to store PoS systems daily. However, unreported errors during this process, such as network downtime, can result in some items remaining incorrectly priced in a store PoS system. In response to this issue, Capgemini has developed a bot that compares the pricing between upstream and downstream systems at the end of each batch pricing update, alerting business users, and triggering remediation where discrepancies are identified. Finally, the bot checks that remediation was successful and updates the incident management tool to close the ticket.

Similarly, Capgemini has developed a validation script for the utilities sector, which identifies possible discrepancies in meter readings leading to revenue leakage and customer dissatisfaction. For the manufacturing sector, Capgemini has developed a bot that identifies orders that have gone on credit hold, and bots to assist manufacturers in shop floor capacity planning by analyzing equipment maintenance logs and manufacturing cycle times.

CIAP has ~200 bots currently built into the platform library.

A final advantage of using platforms such as CIAP beyond their libraries and cost advantages is that they provide operational resilience by providing orchestrated mechanisms for plugging in the latest technologies in a controlled and cost-effective manner while unplugging or phasing out previous generations of technology, all of which further enhances time to value. This is increasingly important to enterprises as their automation estates grow to take on widespread and strategic operational roles.

]]>

Infosys BPM has reached its 18th birthday, in many cultures the age of maturity, achieving a major milestone of $1bn in annual revenues. Infosys BPM today is a very different company from its birth in 2002 when it was set up as a JV in India with Citibank, and there have been some significant developments in the last couple of years.

We recently caught up with Infosys BPM CEO Anantha Radhakrishnan, and while he is intensely conscious that it not a time for celebrations when a pandemic is raging, there is a clear confidence about Infosys BPM’s future trajectory. While not quite celebrating, there is a quiet pride about what the company has been doing to help fight the spread of the infection in the state of Karnataka.

Delivering effective COVID-19 programs

What has been achieved in Karnataka (population 64m+) in a contact, inform and track program in a very short time is quietly remarkable (it certainly appears so to me; my own government, a nation with a similar sized population, has yet to introduce any such program). Karnataka is vulnerable to the virus coming into the state via international travellers flying into Bangalore and Mangalore airports. Its state government turned to Infosys BPM to help launch and manage a program to respond to this specific threat, also a second broader program focusing on citizens across the state.

In the first program, Infosys BPM designed and managed a program to reach out digitally to all travellers coming into Karnataka from March 1 onwards, capture their relevant health data via an app, monitor their health for 14 days, provide a help number should they develop any COVID-19 type symptoms, and also advise on quarantine procedures.

In the second larger program, citizens have been encouraged via an extensive multimedia outreach program to log relevant health and non-health information on an app or helpline number. On the basis of the data they provide, they are given advice on appropriate action to take, with help being arranged in exceptional circumstances. The system integrates with the state’s own hospital and ambulance systems. And in the event of any infection hotspots, it can be used to send localized messages to citizens living in a particular cell phone tower or village. Infosys BPM helped define the outreach strategy, designed the ‘Apthamitra’ app (‘close friend’ in the local language), and assembled a consortium of nine BPS companies that have operations in the state to operate the inbound and outreach program. This activity illustrates the maturity of Infosys BPM in its ability to design and launch a major program from scratch.