Search posts by keywords:

Filter posts by author:

Related NEAT Reports

Other blog posts

posted on Oct 12, 2017 by Rachael Stormonth

I have just looked back at a blog I wrote last May when the news broke of the DXC/HP ES tie-up. Here is an extract: “There is the question of the U.S. federal business that HPE ES will bring in, a market that CSC has only just exited. Will it play a part in the newco? Overall, U.S. public sector would account for around 11% of the newco, way below CSC’s non-compete threshold. When asked about this in the earnings call, (Mike) Lawrie declared ‘post-close, all options and I underscore the word all options would be on the table’. A further divestment may well be on the cards.” See blog here.

I was subsequently assured by HP ES leadership that its federal sector business would be an important part of the newco. I should, of course, be mindful of the fact that a business can switch from being deemed “core” to “non-core” at the moment it is divested.

Anyway, six months after the creation of DXC Technology, we have an answer: DXC Technology is to spin off its U.S. federal business and merge it with two Veritas Capital-owned businesses, Vencore (formerly the SI Organization, spun off from Lockheed Martin in 2010) and KeyPoint Government Solutions (provides background investigation services for federal government agencies formerly Kroll Government Services, acquired by Veritas in 2012), creating an independent, publicly traded U.S. government IT services contractor. As with the CSC/HP ES tie up, this is a tax-free RMT transaction, and Mike Lawrie will be Chairman. Is this a total surprise? Perhaps not.

Some Details of the Transaction

- The newco ownership will be 86% DXC shareholders/14% Veritas Capital

- Newco will pay $400m in cash to Veritas and $1.05bn to DXC. It will also assume $700-800m of Vencore debt

- DXC will use the proceeds to reduce debt, repurchase shares, and “for other general corporate purposes” (possibly M&A?)

- Veritas Capital’s Ramzi Musallam will join the newco board

- Newco CEO will be Mac Curtis of Vencore, COO will be Marilyn Crouther of DXC

- The transaction is expected to close by March 31, 2018.

DXC Rationale for the Transaction

DXC highlights that splitting its USPS and commercial businesses will enable each to focus on their respective market dynamics, optimize capital allocation, and “drive customer value through highly tailored offerings and services”.

The press release also states that combining USPS with Vencore and KeyPoint “will significantly strengthen USPS’ competitive position”. This is perhaps the more pressing factor. If we look at the performance of USPS in its Q1 FY18 (the one quarter that DXC has reported since its creation), it had a very low 0.3x B2B. This, obviously, is partly a reflection of lumpiness in large deal awards in the sector, partly a contraction in federal spend, and partly a timing issue (slippage in signing of a large award in the National Security sector), but it does also indicate a lack of competitiveness.

The Newco: a Top 5 U.S. Federal IT Services Contractor

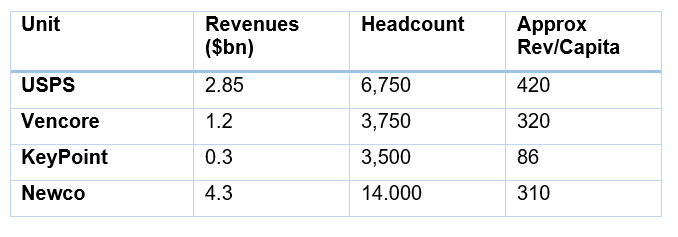

The table below summarizes approximate revenue and headcount for each of the three businesses.

Joining forces with Vencore and KeyPoint will add scale: as a $4.3bn firm the new company will be a top five (by revenue) U.S. federal IT services contractor, similar in size to SAIC and CACI, and not much smaller than (mostly former CSC business) CSRA.

We don’t know the margin profiles of Vencore and Keypoint but suspect that Vencore is at least on a par with USPS (11.4% segment margin in Q1 FY18); its portfolio includes some high margin offerings, also Veritas was looking for a buyer for Ventura in 2015, and is likely to have stripped out costs since. Certainly, in its investor presentation, DXC refers to “industry-leading profit margins”.

While neither USPS nor Vencore has been enjoying topline growth recently, the opportunities for the newco are likely to center more on revenue than on cost synergies, though there will be obvious ones, e.g. around HQ rationalization, also in applying automation to the KeyPoint business.

Vencore, for example, brings to the table capabilities in cyber (enhanced with its 2014 acquisition of Qinetiq North America), and analytics, as well as system engineering.

There is little client overlap: Vencore’s client base includes Intelligence and Defense agencies, whereas, outside its DoN NGEN contract (where the addition of Vencore may be an important factor in the recompete), the USPS federal client base includes the likes of VA, HHS and CMS. The newco will have both a broader portfolio and also access to a broader range of contract vehicles - as Lawrie highlighted, significantly strengthening USPS’ competitive position.

There is shareholder value in this transaction, but what does this mean for DXC?

The transaction will not mean that DXC becomes a commercial sector pureplay: it retains a large public sector business, both internationally and also in the U.S. state and local segments. Looking ahead we suspect further smaller-scale divestment activity may be on the cards.

Meanwhile, DXC continues to invest in expanding certain parts of its portfolio, this week announcing the tuck-in acquisition of Logicalis SMC, further strengthening the already extensive ServiceNow capabilities that CSC then DXC have been ramping up through a series of acquisitions.

We look to see whether there will be also be an increasing emphasis by DXC on certain sector plays, for example Insurance (for example Xchanging brought in insurance software IP and there is the big win a MetLife)): a heavily verticalized (commercial sector) focus has not been a feature of CSC nor HP ES in recent years, but within its GBS business, its Industry IP and BPS businesses could do with a shot in the arm.

Postscript

The initial title of this blog was: "DXC Spins Off U.S. Federal Business: State and Local Next?" However, I overlooked its acqusition of Microsoft Dynamics 365 specialist Tribridge, for which, its Q2 FY18 SEC filings reveal, it has paid $152m. Tribridge, now part of GBS, enhances its offerings and presence in the healthcare, justice, and public safety markets. And of course DXC has a significant presence in the Medicaid sector, with a practice currently included in the health unit of its Commercial segment. Mike Lawrie has sold off a U.S. public sector business twice now; acquiring Tribridge and then doing this for a third time (of units serving various state and local markets) is extremely unlikely. Once USPS is spun off, will we see more clarity about the various non private sector industry practices that currently tucked within Commercial?