Search posts by keywords:

Filter posts by author:

Related Reports

Related NEAT Reports

Other blog posts

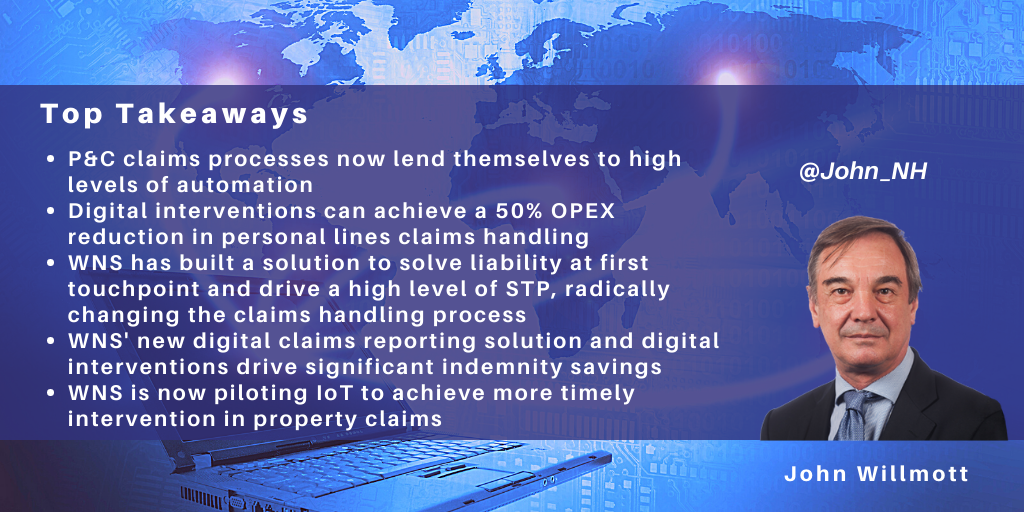

posted on Jan 22, 2021 by John Willmott

WNS has a highly developed property & casualty (P&C) insurance practice handling 30 million claims transactions and ~$12 billion in claims spend annually. The company has extensive capability in property & casualty supporting motor, property, casualty, employer and public liability for insurers, fleet operators, MGAs, global corporates, and municipal authorities. WNS has strong capability in the Lloyd’s & London market supporting specialty lines products. The company has developed a range of proprietary solutions in support of its P&C and Speciality BPM business.

The company has now taken its proposition to the next level by reinventing, automating, and digitizing its claims handling capability to assist insurers in competing with the new generation of digital disrupters.

WNS Seeking to Reengineer P&C Claims Handling to Touchless Process: Proposition – ‘Simplified Claims’

WNS’ strategy is to assist its P&C insurance clients in moving to contactless, touchless claims, with their or clients’ staff only intervening for the decreasing proportion of exceptions that need manual handling, typically for risk appetite, strategy, governance, or customer proposition reasons.

This has the potential to enable insurance companies to dramatically reduce their operating costs while simultaneously speeding up the claims process and increasing customer NPS.

For example, for motor claims, key elements in this strategy include:

- Establishing the liability for approx.70% of claims at the first notice of loss (FNOL) stage, whether received via a portal, email, or voice and then automating all downstream claims management in these cases

- Minimizing dispute timescales and costs by providing a self-serve option for the customer and third-parties to acknowledge an accident’s circumstances and share their versions of events in a timely fashion

- Automating the downstream processes if the policyholder is at fault, with third-party and subrogation interventions handled digitally

- Identifying and progressing fraud throughout its life cycle

- Handling Third Party exposures via complex AI, ML models to assess unstructured data, complete valuations, and make offers.

Similar disruptive solutions to drive high levels of straight-through processing (STP)/one-touch claims are deployed for property (personal and commercial) and casualty products.

WNS is also looking to minimize the insurance supply chain cost. For example, in property insurance, this will involve using images and video calls to cash settle more property claims at one touchpoint, eliminating the necessity for visits by loss adjustors.

Using New Digital channels for More Timely and Effective Claim Notification

One of the pain points with commercial customers and fleet companies is the amount of time taken by end customers/drivers to report accidents. In these large corporate and municipal accounts, WNS has found the average notification time to average 33 days, which leads to a loss of opportunity to intervene and reduce the loss incurred.

Accordingly, WNS is piloting the use of new digital channels so that the driver of a vehicle can effortlessly report a claim in one touch and upload images, enabling WNS to receive details such as the third party’s registration number details within minutes of the incident. This has the potential to be particularly effective in the case of drivers whose lack of fluency in English may be inhibiting accident reporting.

Similarly, for property surge events, whenever there is a warning of a weather event, such as an Australian bushfire, WNS will identify the post/ZIP codes for the areas likely to be impacted and use this new digital approach to share a prepopulated claim form with customers a day or two in advance of the weather event.

This avoids the need for customers to phone potentially heavily loaded contact centers. Instead, they upload details of their losses, and WNS will respond within 30 minutes, providing details of coverage and dispatching services accordingly.

The new digital reporting channel pilots for motor and property claims are at the completion stage and have been successful from customer experience and indemnity spend standpoints.

Enhancing the Competitiveness of a Major P&C Insurer

WNS has applied its claims strategy components to assist a major global insurer in substantially improving its competitiveness through a fundamental reinvention of its claims processes.

The insurer had carried out a competitive benchmark with a major consultancy, which estimated its OPEX to be very high on a like-for-like basis, with contributory factors being the excessive fragmentation of the insurer’s onshore delivery across more than ten onshore sites and its comparatively low usage of automation and digitalization.

WNS initially addressed these issues by consolidating the insurer’s onshore sites to two centers. WNS also made operating model changes at one of these sites, introducing a collaborative team structure with client staff working alongside WNS staff on a co-branded production floor. A WNS site head runs the site, and in addition to agents, the WNS site personnel include process leads, continuous improvement consultants, and RPA and analytics specialists. The overall client operations delivered by WNS leverage a combination of onshore and offshore delivery.

Secondly, considerable automation and digital interventions have been introduced into the insurer’s motor, property, and casualty claims process. These digital interventions are funded through an innovation funding mechanism that ensures “continuous improvement is a way of life by design”. WNS initially provided resources to deliver productivity improvements, taking a share of the resulting savings, part of which is then used to self-fund further productivity initiatives to establish a continuous reengineering cycle.

Within the new digital model, each new claim reported via the digital channel is run through an automated liability solution, followed by an early settlements, total loss, recovery, and fraud identification model, all integrated via a simple process flow running seamlessly in the background. These interventions are followed by automation of the appropriate downstream activity, such as booking the vehicle for repairs, courtesy car allotment, etc. For suspected total losses, the claim details are run through a total loss predictive tool. These processes for both repairable and total loss motor claims are supported throughout by a self-serve E-FNOL app and fraud screening.

The liability predictive model used by WNS within this contract is based on partner insurtech technology. The system automates digital liability handling within motor claims, including:

- Prompting using image-based questions to establish the accident scenario, including testimonials from witnesses, using links to Google Maps and historical meteorological data to help pinpoint the accident's exact location and weather conditions at the time

- Sending allegations to the third party for self-serve input and responses

- Integration with case law to assist in decision-making

- Built-in AI to identify fraud and subrogation opportunities.

Overall, WNS uses various commercial models ranging from FTE, transaction-based pricing, management consulting fees, and gain share within the contract. Although personal lines claims within the contract are largely paid on transaction-based pricing, WNS is additionally committed to guaranteed percentage efficiency and indemnity improvements together with customer journey improvement.

The overall benefits achieved for this insurance company included:

- Improvement of 15-20 NPS base points

- Improvement of +30 employee NPS (ENPS) base points

- ~50% OPEX reduction

- ~2% motor indemnity reduction.