Search posts by keywords:

Filter posts by author:

Related Reports

Related NEAT Reports

Other blog posts

posted on Jan 17, 2017 by Dominique Raviart

M&A activity in IT services is set to take a new direction in 2017. Here, I reflect on M&A activity by the largest IT services vendors in 2016, with its emphasis on mega deals, and look ahead to 2017, which is set to be the year of digital & security tuck-in acquisitions.

Large M&As in 2016: IT Conglomerates and Defense Firms Divest IT Services Arms

Large-scale M&A activity in 2016 was characterized by:

- IT conglomerates disposing their IT services businesses (HPE and Dell)

- Defense firms selling their U.S. federal IT services activities (Lockheed Martin and L3)

- Telecom service providers divesting their datacenter business (Verizon, CenturyLink).

There has been a lot of water under the bridge since the late 2000s, when hardware conglomerates were acquiring IT services firms, looking for higher margins. Several of those conglomerates have now divested their IT services arms (HPE, Dell; and, in BPO, Xerox). Having said that, there is no universal business model in the IT industry: IBM, Fujitsu, (and to a lesser extent Hitachi and NEC, both in Japan) are tier one IT services vendors, currently ranking number one and three, respectively. We believe this trend is long-lasting and expect further service divestments by hardware vendors.

Divestment of IT services arms has spread to other sectors, e.g. the U.S. defense sector, where Lockheed Martin is the largest transaction. Recent transactions also include CACI’s acquisition of L3’s National Security Business (a $550m transaction, with the acquired unit having $1bn in revenues), and Honeywell’s sale of its government services division to private equity KBR (for $300m). Looking ahead, how the Trump administration will impact government services spending is difficult to predict.

NTT DATA Acquires Dell Services. Other Telcos Selling Datacenter Businesses

In a previous blog (here), we discussed how telecom service providers retrenched from significant M&As in IT services in recent years. Today, there remain just a few significant telecom service providers with presence in IT services: NTT Group (through subsidiaries such as NTT DATA, and Dimension Data) and Deutsche Telekom (with T-Systems). BT Global Services has largely refocused its IT services presence to the U.K., although it remains present globally in network services.

Other telcos have been reconsidering their datacenter assets: Verizon is selling 29 datacenters to Equinix, for $3.6bn. This is a major change in Verizon’s strategy: Verizon had acquired Terramark, a hosting and cloud computing vendor in 2011 (for $1.4bn). Also in the U.S., CenturyLink is divesting its datacenter and co-location business for $2.3bn, to private equity. On a smaller scale, Colt in Europe sold its 12 datacenters to PE-backed Getronics.

In 2017, telcos will continue shifting their assets from IT services (and from their capex intensive datacenter business) towards media companies, internet vendors (mirroring Verizon’s likely acquisition of Yahoo), and overall market consolidation (Europe remains fragmented, while the U.S. has now become concentrated, the latest M&A being that of L-3 Communications by CenturyLink for $24bn).

SaaS, Digital Marketing, and Cyber Drive Continuous Flow of Tuck-In Acquisitions

SaaS, digital marketing, and cyber-security continued in 2016 to drive a continuous flow of tuck-in acquisitions. Accenture was the most active acquirer in this space, with $930m spent on acquisitions in FY16. Outside of Accenture, most major IT services vendors made up to three investments in digital and security during the year.

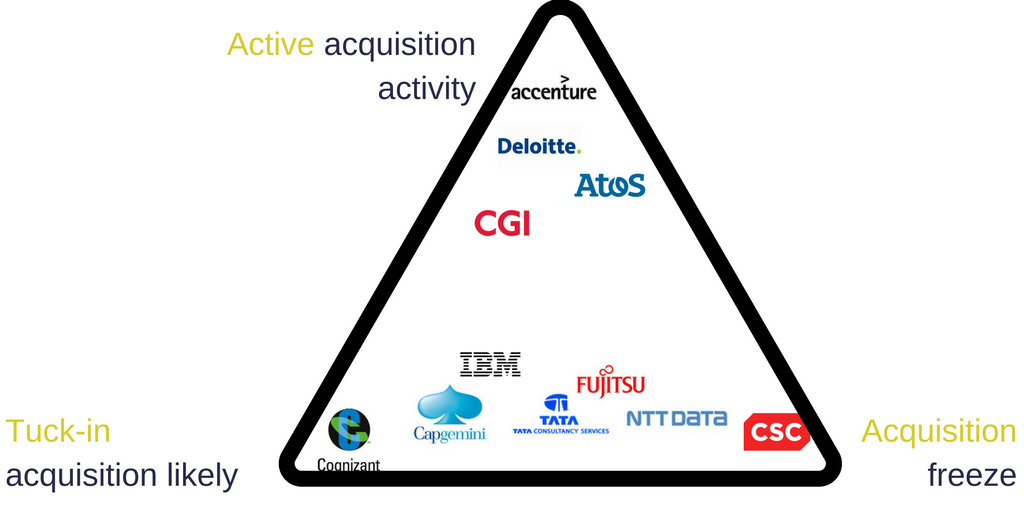

M&A Predictions for 2017 of Top Ten IT Services Vendors: Accenture Continues Digital Buying Spree. CSC and NTT DATA Focus on Integration

Looking at the top ten IT service vendors, apart from Atos and Accenture, we are not expecting any large transactions to occur.

In more detail, our expectations for the M&A focus of each of the leading IT services vendors are:

- IBM’s focus will continue to include infrastructure cloud computing (sitting at the intersection of IT services and hardware), and smaller SaaS service specialists

- Accenture has been the most acquisitive vendor in recent years, as it has pivoted its offerings to what it terms “The New”. We expect Accenture to remain very active in 2017

- CSC and HPE ES new co: one would expect there to be a pause while the integration takes place (also a $5.5bn net debt); however, there could be small to mid-sized acquisitions bringing in industry IP

- Fujitsu has been on acquisition freeze since 2009 (KAZ). We expect this will continue, as Fujitsu continues to face headwinds across its technology units

- NTT DATA: in North America, the focus will be on integrating Dell Services. There may be small scale acquisitions in Europe and APAC. NTT DATA has a significant geographical gap, the U.K., and is also absent in the French market. While the depreciation of the GBP makes the U.K. an attractive hunting ground for consolidators, attractive firms are likely to be smaller specialists, not of the mid-to-large scale that NTT DATA has tended to pursue

- TCS has succeeded in outstripping market growth without being dependent on acquisitions. The need to reduce dependency on H-IB visas could be a driver for investments of some kind to increase its onshore presence in the U.S.

- The Deloitte/DTT network has an acquisition strategy similar to that of Accenture, with a strong focus on digital firms. DTT is transitioning from country operations to larger geographical entities (e.g. DTT in U.K. and Switzerland is absorbing affiliates in Belgium, Netherlands, Denmark, Finland, Iceland, Norway, and Sweden, into Deloitte North West Europe). This increased scale could help in acquiring larger targets

- Capgemini has completed its integration of IGATE and made clear it wants to acquire digital firms in North America in retail/CG/wholesale industries. It is constrained by its €2.3bn net debt and a recent €500m increase in its share buy-back program

- Cognizant, under some pressure from PE, will accelerate its digital tuck-in acquisitions, which have been relatively modest

- Atos had a quiet M&A year in 2016, WL finalizing the acquisition of equens, and Atos North America acquiring Anthelio. The company has financial freedom with a net cash position expected to reach €0.5bn by 2016-end and an additional €3.5bn in potential financing in the 2016-2019 period. We expect the focus will continue on gaining scale in target U.S. America commercial sectors

- CGI is also likely to be more active in 2017, having been somewhat quieter in the last two years than it had indicated in closing a transaction with the “right firm at the right location”. U.S. commercial remains a priority, as is IP/software products. CGI’s preferred mode historically has been a large acquisition every few years. The recent acquisition of Collaborative Consulting indicates a different approach, and that smaller specialists in target regions, such as New England, or sectors, such as BFSI or utilities, are now more likely.