Search posts by keywords:

Filter posts by author:

Related NEAT Reports

Other blog posts

posted on Dec 01, 2017 by Dominique Raviart

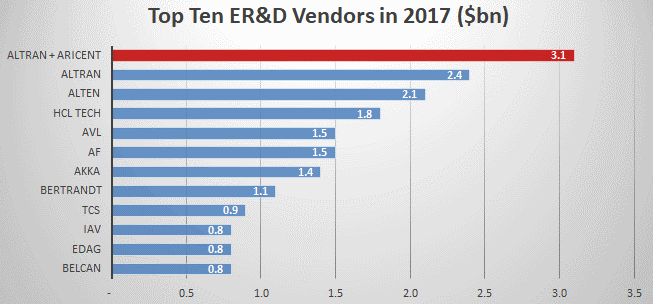

ER&D vendor Altran yesterday announced the acquisition of India-centric Silicon Valley-headquartered Aricent. Altran will be paying $2.0bn for Aricent through a capital increase of €0.75bn, the remaining ~€1bn in debt.

In the year ending June 30, 2017, Aricent had revenues of $687m and an EBITDA margin of 27.9%.

This is a significant acquisition for Altran, strengthening its position as the largest ER&D vendor globally. The combined company will have revenues of ~$3.1bn, and 44k employees, including ~12k in India. Altran, which already was the largest ER&D vendor in Europe, is now also a major player in North America, with revenues not far from those of HCL Technologies.

With this move, Altran will achieve several of its strategic ambitions: by 2020 to reach €3bn in revenues, an adjusted EBIT margin of 13%, and a global delivery network of over 10k.

As well as adding scale in North America, Aricent will also strengthen or fill Altran portfolio gaps in several key areas:

- Strengthening its capabilities in the telecom industry and in semi-conductors

- Bringing in expertise in software product development, internet technology development, and UX design (though the Frog subsidiary).

This is a highly complementary and strategic transaction. So why hasn’t the market’s initial response been warmer? Altran’s share price fell by 6% on the day of the announcement.

High Debt Level and Capital Increase

Much of the negative reaction relates to the capital increase (€0.7bn) vis-à-vis Altran’s market cap (~€2.4bn), and its increased debt (€1.3bn after the capital increase). Altran’s CEO has stressed that the target is to reduce its debt level from a leverage of 3.25 down to 2.5 within two years. The debt level will be high, but this is in the context of lowest interest rates ever.

What about Germany?

One likely impact of acquiring Aricent is that Altran is now unlikely to reach another objective, of deriving €500m in revenues by 2020 from Germany; this was also a key priority, along with the U.S. We estimate that in 2017, Altran will have revenues of €270m in its Germany/Austria business unit, half-way to its objective.

Does this matter? Well, yes; Germany is by far the largest ER&D service market in Europe, with half of its spending done by the automotive sector. While the German automotive ER&D market has been a difficult one in the past two years, resulting from changes in legislations, the reduction by Volkswagen Group (the largest spender in Europe) of its R&D spending, and price pressure, it remains a strategic country to be in for ER&D services vendors.

How Healthy is Aricent?

Altran management has not provided an indication of recent organic growth at Aricent, highlighting instead the rapid change in Aricent’s portfolio, which until the early 2010s had been very telecom-centric and had suffered from anemic spending in the sector.

Aricent has been through a reinvention, closing small geographies, and expanding its client base, from telecom equipment manufacturers to telecom service providers, and then semi-conductors (in chip design, through the $180m SmartPlay acquisition), and to automotive, relying initially on its network/connectivity expertise. In 2015, Aricent also expanded to software product/internet technology development.

Despite this reinvention, Aricent still derives 54% of its revenues from the telecoms sector. Semi-conductor/industrial has become significant (19% of revenues), Frog/UX design (16%), and product/technology development (11%) is a rising segment.

We note that Aricent has an IP partnership with an unnamed ISV: while IBM has not been announced as a partner, the structure of the deal is similar to the HCL Tech and Tech Mahindra IP partnerships, with Aricent acquiring $250m in software assets over four years, and already having a flow of revenues of ~$50m in LTM. We assume this flow represents software development fees from IBM.

Overall, a Bold Move

In short, this is a highly complementary and strategic acquisition. It does leave Altran exposed to financial stress, should market conditions deteriorate. And indeed there is some uncertainty in the automotive sector in the U.S., and in France around the key PSA account. But Aricent is not a major player in the U.S. automotive market.

Well done Altran for this incredibly bold move!