Search posts by keywords:

Filter posts by author:

Related Reports

Related NEAT Reports

Other blog posts

posted on Jun 12, 2020 by Andy Efstathiou

The past decade since the global financial crisis (GFC) has been good for the lending industry. Loan delinquencies in the U.S. reached their highest level after the GFC in the first quarter of 2010 at 7.4% of commercial bank loan portfolios. Since then, loan delinquencies have fallen to 1.44% of loan portfolios as of the fourth quarter of 2019. At the same time, loan portfolios have grown 26.8% larger than they were in the second quarter of 2013. During this period, banks and lenders have reduced collections staff as delinquencies have declined. Banks can support delinquency collections if portfolios maintain low default rates.

However, COVID-19 has had a major adverse impact on the economy. During this time unemployment rates have surged and GDP forecasts have plummeted.

This type of economic contraction will aggressively drive up collection activities at banks. But scaling collections activities will be challenging when all lenders will be trying to scale-up their activities at the same time, and as new regulations constraining collection methodologies are being issued.

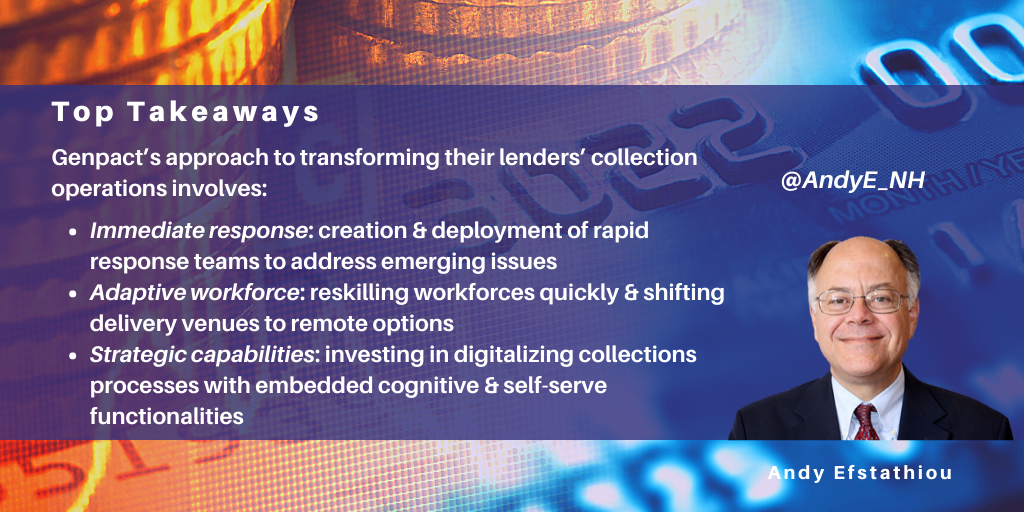

The automation and operating framework will be critical to successfully navigating the collection environment. I recently participated in a Consumer Bankers Association hosted webinar with Genpact where they outlined their approach to improving collections services. Genpact has developed a three-part methodology for transforming their clients’ collection operations:

- Immediate response: creation and deployment of rapid response teams with simplified decision-making structures to address emerging issues and deteriorating portfolios

- Adaptive workforce: reskilling workforces quickly and shifting delivery venues to work-from-home (WFH) or other remote options

- Strategic capabilities: investing in digitalizing collections processes and embedding cognitive and self-serve functionalities

The challenge is large, so success requires a set of prioritized actions to make early gains possible. Examples from Genpact include:

- Immediate response measures taken to date include efforts to proactively identify and remediate high-risk customers before they hit delinquency. Clients can reduce exposure related to high-risk customers by leveraging machine learning to develop and deploy a combination of credit limit decrease and blocking, or proactively offering customers hardship plans. Using text-mining of agent notes from customer service interactions has allowed early identification and treatment of high-risk customers

- Adaptive workforce measures have had the highest activity to date, and include:

- Rapid, remotely delivered workforce training. For example, Genpact is helping a top 5 global bank is ramping up their operations from 600 to 1600 skilled collections resources

- Workforce multiplier support such as a group of rapid response teams (cross-functional teams that can address the rapidly evolving customer dynamics through agile pods). These teams deliver services such as surge-capacity hiring, training, and deployment all with WFH solutions

- New models of data usage, both new data forms, and alternative data streams. COVID-19 has changed customer behavior, and ML needs to be used to identify new customer segmentation patterns and the appropriate response. This is not a one-time activity; it requires weekly refreshes as the data/behavior changes

- Regulatory changes such as the Consumer Financial Protection Bureau’s recently published new contact policies. Straddling compliance and good practice is the need to define and test what empathetic response should be. There are no clear metrics, particularly when it comes to a customer situation where they may be impacted economically, socially, and health-wise

- Strategic measures taken to date include investments in:

- Channels of customer contact and payment beyond the voice channel, including chatbots and self-service

- Automation of manual back-office processes in collections using RPA or workflow solutions, so that agents can focus on customer management. This has been especially useful for implementing the CARES Act program

- Use of AI, ML to develop and offer unique hyper-personalized treatment strategies suited to specific situations and requirements of individual customers. These customized solutions can reduce customer hardship as it considers the individual realities to make the debt more manageable for customers

- Building empathy into conversational tools: for example, real-time speech analytics and conversational AI to prompt effective payment plan matching to customer needs using the appropriate verbiage usage based on customer talk

In short, scaling the same processes, under conditions of reduced resources, increased costs, and growing transaction numbers will not work. Already vendors are addressing these challenges by employing combinations of proactive outreach, workforce training, and technology. Lenders will then be able to increase their effectiveness and scale in collections to meet the rapidly increasing scale of operational delivery required.

To find out more on this topic, view the Consumer Bankers Association hosted webinar with Genpact and NelsonHall here.