posted on May 24, 2021 by Ivan Kotzev

While the CX services industry is anxiously following the situation in India and its surge of COVID-19 cases, the start of 2021 mainly brought positive news. In this blog, I look at the strong performance across the industry and the extent to which the current growth is sustainable.

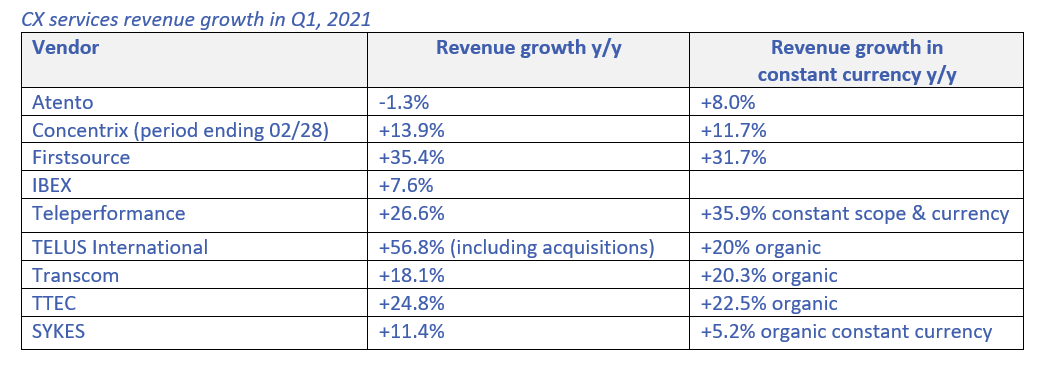

2021’s record start

The three months ending 31st March 2021 was a record quarter for many CX services players. Multiple vendors had double-digit revenue growth, double-digit organic revenue growth, and improved margins.

Much of the growth came from pandemic-related business in the public sector, where vendors provided unemployment support, COVID-19 loan processing, test and trace services, health information helplines, vaccination appointment scheduling and booking. But rapid growth came across sectors, from digitally native and ecommerce companies to healthcare, technology, entertainment, and gaming. Of particular note is the BFSI segment which expanded for all providers.

Across service lines, customer care, new customer onboarding, and content moderation services all saw significant growth. To take one industry-specific example, volume increases in the banking sector have reflected pent-up demand for mortgage processing.

Better margins in Q1 2021, following the big hit last year, came as a result of lower attrition and improved productivity in WAH and during lockdowns.

Tailwind factors

Part of the story is the economic recovery in the U.S., Western Europe, AN&Z, and China, but some drivers are exclusively industry-specific. In a January blog, I discussed the positive trends for 2021 in CX services. Tailwind factors include greater client demand to transform their CX operations, growth of digital-native companies, and the changing relationship between customers and brands...

Vendor goals for the year are to capture a greater number of first-time outsourcers and expand share with existing clients who realized the benefits of risk diversification and the challenges of running a hybrid on-site and at-home customer service delivery structure.

... Five months later, the experience economy is top of mind for companies, and digital-first CX creates interaction volumes across many and new channels simultaneously. It also drives a need to redesign CX across all services and products. This switch brings challenges around technology, internal processes, and the overall customer journey. The convenience of everything being done from home forced clients to transform their business model, leaving little bandwidth to deliver high-quality support and digital sales, creating opportunities for CX services outsourcing and driving enterprises to partner with vendors with disruptive capabilities.

Keeping the momentum

An immediate question for the rest of the year is how successful CX vendors will convert this temporary business surge into permanent deals. The signs are promising because of the above-mentioned digital shift and external factors impacting talent sourcing and management.

First, the labor markets are becoming more challenging, either because of temporary changes such as the unemployment benefits in the U.S. or permanent ones such as the minimum wage increase in Brazil. As attrition returns to normal levels, clients struggle to acquire talent, relying more on their vendors.

Second, employee expectations for more flexible and convenient work models such as WAH benefit large organizations such as CX services providers with experience in recruiting, onboarding, training, and engaging talent virtually.

Multidimensional rebalancing act

The CX services industry is undergoing several rebalancing trends at the same time. On one side is vendor diversification of the client base, leaving fewer accounts, especially telecom, with more than 10% business share. The second focuses on promising sectors with hypergrowth paths such as online entertainment, fintech, and healthcare. From another angle is the aim to offer a broader spectrum of BPS to tackle organization-wide transformation challenges. A prime example is an aggressive push for cloud migration of contact center operations and the partnership of all large players with Amazon Connect.

Vendors are reacting with active M&A strategies such as:

- Teleperformance’s acquisition of Health Advocate to expand U.S. healthcare offerings and capabilities

- TELUS International’s purchase of Lionbridge AI for data annotation

- Tech Mahindra’s deal for Eventus Solutions to strengthen CX consulting capabilities

- TTEC’s acquisition of Genesys and Microsoft integrator and contact center technology developer Avtex.

In parallel, companies from Europe and LATAM such as Atento, Webhelp, Transcom, and Majorel are targeting the U.S. market more actively, looking to benefit from the internationalization of businesses.

Finally, the rationalizing of onshore facility portfolios is beginning to pick up as vendors want to rebalance on-site with WAH delivery.

Sustaining top-line growth

I will conclude the same way as in January: external factors continue to be the most significant unknown in the CX services industry and can reverse the strong market impetus. These factors can be negative, such as the uneven pace of recovery and vaccine access around the world such as India and continued headwinds in travel and hospitality; or they can be positive, such as the potential tax reduction in the Philippines and faster than expected economy bounce-back in core markets.

The market indications are for a strong second quarter and upwardly revised annual results. In the medium term, CX modernization will continue to drive market demand while good execution will differentiate between temporary and sustainable success.