posted on May 01, 2018 by Ivan Kotzev

For many years, the telecoms sector has been the dominant market for customer experience (CX) services providers. However, over the last few years, consolidation, flat performance, decreasing margins caused by market saturation, new digital models and competitors, and unfavorable regulations (e.g. Eurotariff) have eroded the significance of the telecoms sector for CX services providers. Indeed, a common boast among CX outsourcing executives is their success in diversifying away from the sector.

And now, the $26bn acquisition agreement between T-Mobile and Sprint, announced last week, looks set to accentuate that trend. If approved, the deal will leave only three national wireless players in the U.S. and will put further pressure on their CX services providers.

Decreasing share & focus on telecoms

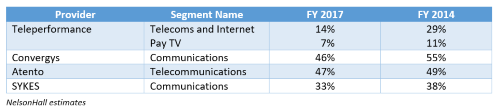

The communications industry remains the largest CX services sector at ~24% of the market in 2017 (NelsonHall estimate), but for most of the leading CX services providers it has been steadily decreasing in the last few years, both as a share of business and in absolute terms, as shown here:

Major telecoms brands such as AT&T, T-Mobile, Tele2, O2, Telefonica, BT, Three, and Telstra remain the largest clients for many CX services providers. However, in times of fluctuating volumes, this telecoms top-heavy client base has adversely impacted several providers in their core markets, though typically the overall growth in other sectors has offset the steady decline in communications. Additional factors such as the high level of self-service, where the sector has been a pioneer, simplification of offerings and product ranges, and demand for cost savings through offshoring, have further impacted the size and profitability of the segment.

Digital opportunities in other, high-growth industries

The telecoms sector has been leading in the adoption of emerging digital channels such as messengers, in the implementation of contact center RPA, and the use of customer-facing automation through bots. However, partially due to the sector’s success in adopting these digital models internally, and partly due to smaller innovation investment funds, many of the most innovative and largest-scale outsourced CX implementations have been in other industries; for example:

- Videochat and messengers support in the e-retail, banking, and travel sectors

- Contact center and back-office automation in financial services, healthcare, and energy & utilities

- Big data analytics for revenue generation in BFSI, e-retail, and consumer electronics

- Remote diagnostics and self-healing for tech support in high-tech and automotive.

Major tech players such as Amazon, Alibaba, Apple, Facebook, Google, JD.com, and Netflix have now reached the scale of outsourced CX operations previously seen only in telecoms. The added benefit for these companies is their global nature, being able to offer multi-market prospects.

But evolving telcos can be very attractive clients

Nevertheless, the constant evolution of telecoms’ business models, exemplified by Vimpelcom’s new strategy to reinvent itself as a global tech company, or the recent M&A surge to create telco-media behemoths such as the proposed AT&T Time Warner merger, unlock new opportunities. A great example of telco evolution has been AT&T’s purchase of DirecTV in 2015, which consolidated the outsourcing network but also provided new markets and service lines for AT&T core vendors.

The shift to 5G and IoT and the evolving telco’s end-user needs require proactive support, heavy use of automation and machine learning in the contact center, and always-on digital engagement. All these are current investment areas for CX services providers and, even if not straight away, telecoms will eventually reap their benefits.

NelsonHall’s pending Global CXS Market Forecast 2018-2022 report and self-service forecasting facility provide industry breakdowns by service line, sector, geography, and vendor. For access, please contact NelsonHall Client Services Director Guy Saunders