posted on Mar 15, 2022 by Ivan Kotzev

NelsonHall recently published a CX Operations Transformation market analysis, with growth forecasts and highlights of the major client requirements, challenges, and success factors for the adoption of next-gen CX. Here is an abbreviated look at the state of the market in Q1 2022 and several expected short-term scenarios.

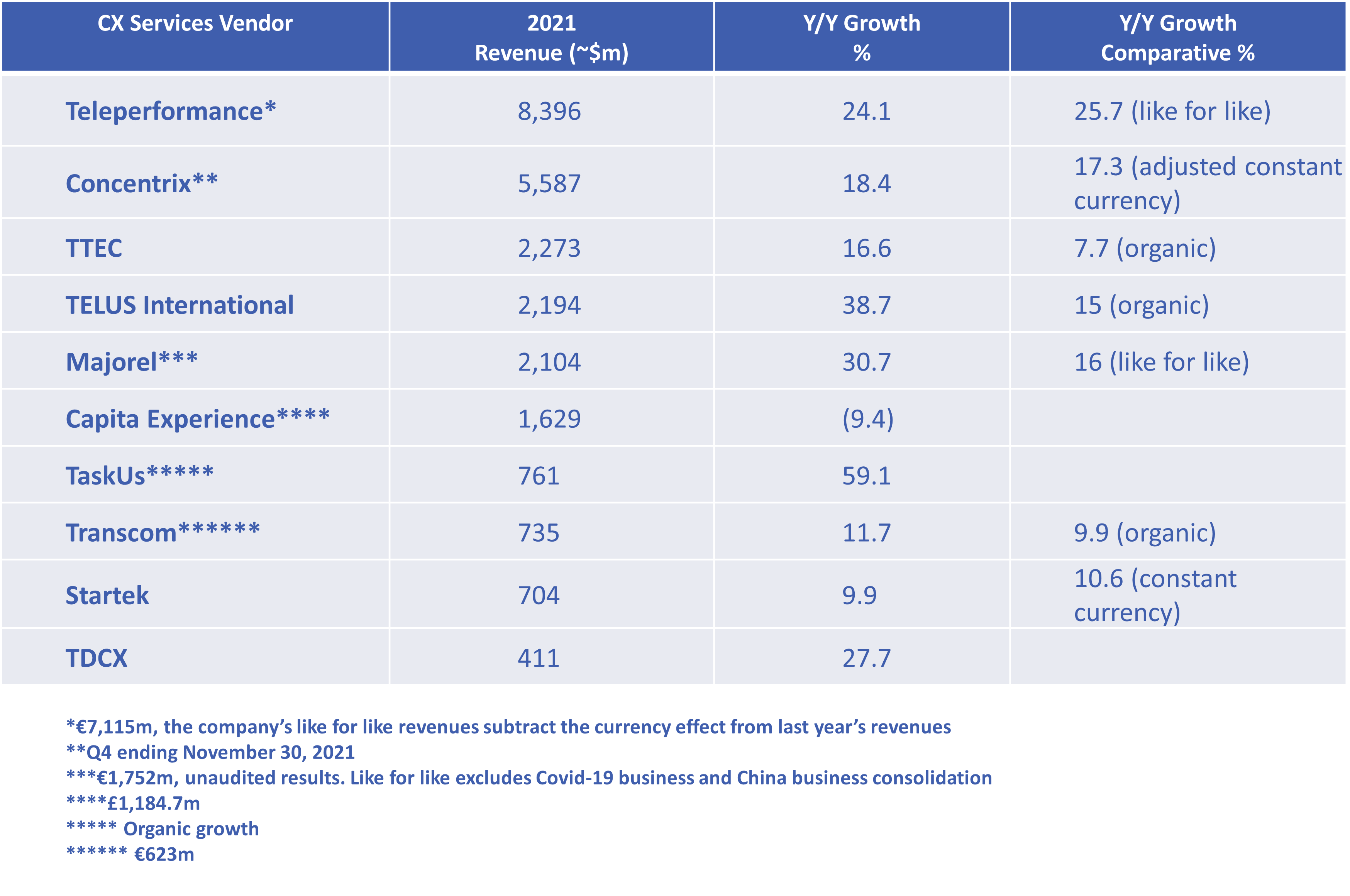

2021 was a good year for CX services

After the disruptive first nine months of 2020, the CX services market began a rapid recovery, which lasted throughout 2021. In fact, the global market rebounded strongly, with many vendors achieving record organic growth beyond their pre-pandemic levels.

The table below shows the annual revenues for publicly listed companies, their respective year-over-year expansion, and comparative growth percentage with caveats.

CX services revenues for FY 2021, ending 31st December 2021

The trend is industry-wide, with both private vendors reporting strong growth (e.g., Alorica, Sitel) and public vendors not included in this table expanding revenues in the quarter ending in December 2021:

- Tech Mahinda with 34% y/y

- HGS with 20% y/y

- Ibex with 12.8% y/y

- Firstsource with 7.2% y/y.

Much of this growth stemmed from the improved economic environment with greater activity across verticals, including the heavily impacted travel and hospitality sector. An example contract in the space is Majorel taking over ~2.7k employees and centers from Booking.com across several markets.

Some of the headwinds behind the growth were temporary. For example, the end of 2021 saw a gradual ramp down of some projects such as COVID hotlines and track and trace activities. However, the growth direction is clear.

An example is the public sector, where part of the healthcare-related work converted into permanent business, such as HGS being awarded a two-year critical care contract by the U.K. Health Security Agency with a maximum value of £211m. Another indication of faster than expected CX growth in the historically sluggish public sector has been vendors' active merger and acquisition activity. Major deals include:

- Teleperformance acquisition of U.S. government BPS provider Senture for $400m

- TTEC's upcoming acquisition of part of Faneuil U.S. public sector business

- Tech Mahindra paying $62m for Activus Connect which has a strong presence in U.S. federal and state services support.

Across industries, the most significant growth engine continues to be the increased adoption of outsourced CX by clients to lower costs, address talent shortages, and meet the business and customer needs for digital transformation.

New economy players demand new CX outsourcing

Ecommerce, fintech, including crypto, media, entertainment, and gaming sectors, posted sizable growth in 2021. An example is Teleperformance, where the media, entertainment, and gaming sectors reached 9% of the business, up from 6% in 2020.

Vendors' responses have evolved from sector diversification (from their legacy telecom accounts) to their current aim of capturing the new client types with targeted sales efforts, custom offerings, and flexible commercial terms. Providers also increasingly complement their portfolio with specialized front-office services (e.g., CSS Corp's services for the mobility sector), analytics (e.g., WNS' Triange), and data training services (e.g., TELUS International).

The major investment focus is in CX consulting resources and capabilities, with the most notable dealbeing Concentrix’s acquisition of PK to form its Catalyst consulting and technology arm.

Another strategic investment is geographic expansion, such as Webhelp's sizable deals in LATAM or Majorel's in Turkey, which allows labor-arbitrage, but more importantly gives additional capacity in the narrowing onshore labor market. This globalization of delivery also supports the borderless nature of new economy clients, who, even at the early stage of development, look to internationalize their business.

These activities will continue with announced plans for acquisitions, additional consulting bench strength, new strategic partnerships, new multilingual sites, and the opening of CoEs and innovation studios.

Impact of the war in Ukraine

In the first days of the human tragedy in Ukraine, the impact on CX services was limited to the few CX operations in the country. The unprecedented sanctions on Russia will likely make in-country delivery untenable, at least in the short term, with one multinational vendor having a meaningful local presence and mostly Russian national CXS providers affected. Some speculative effects through 2022 include:

- Ramp-up of programs in support of travel disruptions, with a slowdown or reverse of the travel and hospitality CX services recovery

- Ramp-up of KYC and regulatory compliance services in BFSI, including in front-office activities

- Increased security and fraud protection work

- Significant ramp-up of social media crisis management and online reputation management services

- Further inflation and labor cost increases

- Expansion of support for ecommerce and online shopping as consumers offset rising gas prices.

Positive signs during instability

Multiple vendors revised up their 2022 expectations to correspond with their improved performance, such as TaskUs looking to reach $1bn. This bullish vision relies on sustainable organic revenue increase and targeted acquisition deals. For example, TTEC aims to double its business in five years, and Teleperformance is planning to become a €10bn company by 2025. Within the constraints of the highly unpredictable global macro-economic situation, the CX services market will likely accelerate above the initial forecast of 5% CAAGR by 2025 (NelsonHall estimate).