posted on Apr 06, 2020 by Sven Lohse

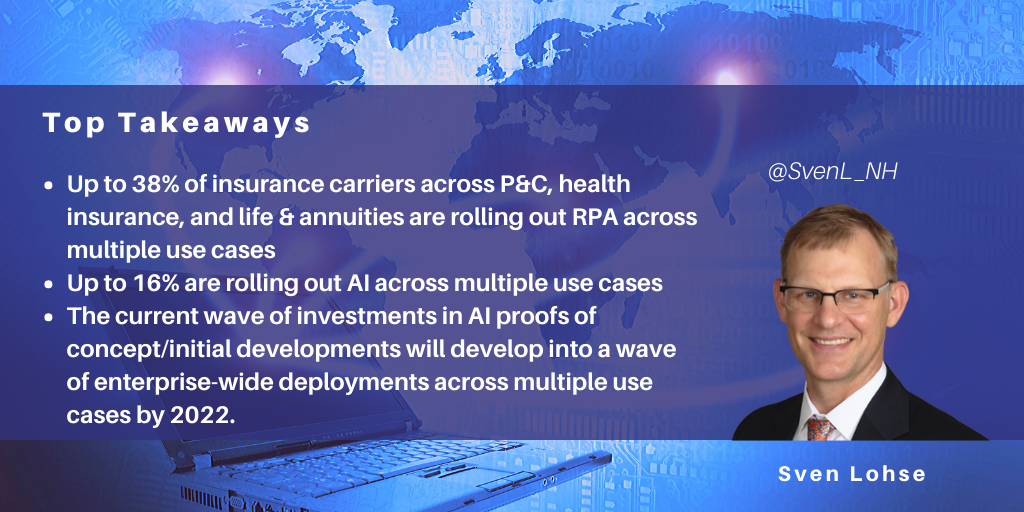

NelsonHall predicts that by 2022, 35% of insurance industry carriers will be in the process of adopting AI technology across multiple use cases within the enterprise. This is based on NelsonHall survey data from the insurance industry that tracks adoption of both RPA and AI (NLP/ML/DL) technology across the property & casualty, health insurance, and life & annuities insurance sectors.

Survey findings

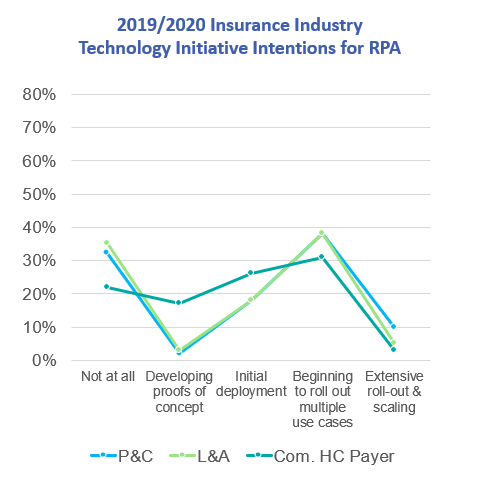

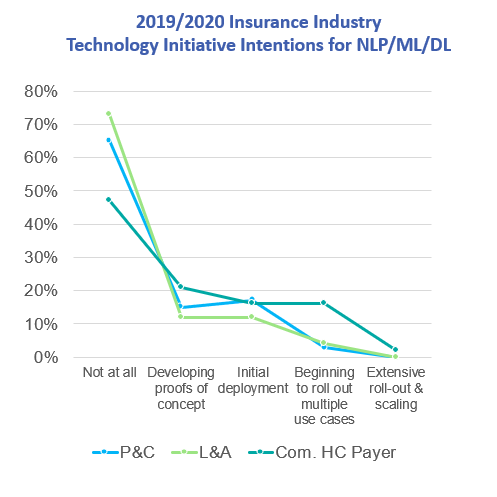

Between 31% and 38% of surveyed carriers are beginning to roll out RPA across multiple use cases, while between 3% and 16% are beginning to roll out AI across multiple use cases – this range includes P&C (3%), L&A (4%) and healthcare payers (16%).

We expect a similar rate of maturity development for AI as for RPA. For RPA, we have seen a wave of investments in proofs of concepts/initial deployments in 2016/2017 develop into enterprise-wide initiatives in 2019/2020. We expect to see the current wave of investments in AI proofs of concepts/initial developments to develop into a wave of enterprise-wide deployments across multiple use cases by 2022. As was the case with RPA, we see a wide variety in the rates of adoption for different types of AI (in particular for natural language processing, machine learning, and deep learning).

The business functions that lead in adoption of AI include:

- P&C insurance: policy origination, underwriting automation, and capacity to manage changes in volume of customer interaction in real-time

- Life & Annuities: policy pricing optimization, contact center real-time customer support, investment support

- Health insurance: product pricing optimization, marketing decision-making.

AI adoption will likely reflect the following broad trends:

- U.S., U.K., and Asia/Pacific carriers will in general lead their counterparts in Continental Europe in the implementation of AI

- Some business functions will provide more fertile ground for adoption of AI, e.g. personal lines insurance policy origination, and customer service will continue to adopt AI more quickly

- Continental carriers will emphasize the importance of customer service and increased speed/ease of new business acquisition in comparison to straight through processing, which is more frequently the top priority for U.K., U.S., and Asian carriers.

General guidance for carriers in adoption of AI

Enterprise governance

Effective enterprise-wide rollouts and scaling of new AI technologies will require strong enterprise governance structures. Efforts completed on behalf of similar enterprise deployments of RPA will pave the way for AI adoption. See the following NelsonHall blog for an example from the health insurance industry: How NTT DATA Established Enterprise Automation Governance for BCBS Health Insurance Carrier

Adapt roles and skills within personnel pyramids

Adoption rates and effectiveness of implementation of AI technologies will ultimately depend on the organizational structures and quality of the people used to transform carrier operations. Carriers will therefore be required to redefine organizational structures, roles and skills. (This will be true whether AI adoption is conducted with or without the extensive use of external consulting and/or outsourcing partners.) Expect significant lag time between the articulation of new organizational structures, roles, and skills, and the period in which enterprises can acquire talent. As with most new technologies, AI experts will be hard to identify, attract and retain, whether compensated directly by a carrier or not.

Align with existing procurement strategies

Procurement strategies that manage external AI partner vendors need to be clear, manageable, and adapted to enterprise procurement structures in place. It’s noteworthy that while outcomes-based, or gain-sharing, contracts get a lot of attention, about 90% of P&C transformational outsourcing contracts in the U.S. are still managed on an FTE, fixed-price, or transaction basis. In Asia Pacific, that proportion is even higher. So, especially for early-stage AI projects, insurance carriers should likely consider keeping outsourcing contracts as straightforward as possible.

Get early buy-in

Winning the race to effective, enterprise-wide adoption of a new technology frequently depends on how innovators introduce that technology within the context of the enterprise. Far-sighted planning may include pilot projects that start small, and then earn organizational buy-in based on clearly demonstrable, early wins. Employee upskilling programs can help allay the fears of those concerned with being displaced by new technologies.